Hospitality Robot Market Summary

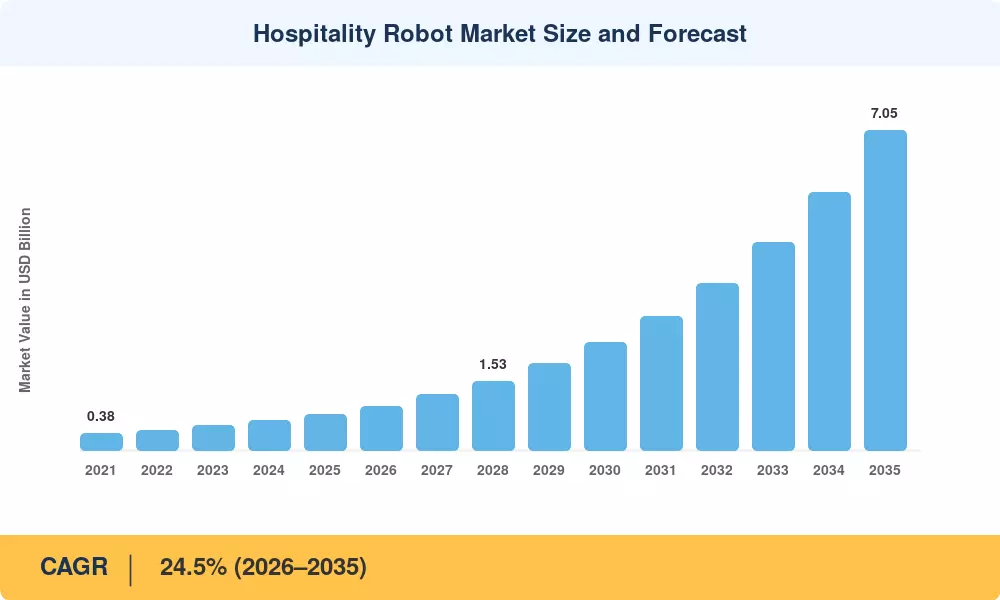

The Hospitality Robot Market reached an estimated USD 0.79 billion in 2025 and is projected to expand from USD 0.98 billion in 2026 to USD 7.05 billion by 2035, registering a compound annual growth rate of 24.5% over the 2026–2035 forecast window. Two catalysts are pushing deployment forward at scale: chronic labor shortages in accommodation and food-service industries, the U.S. Bureau of Labor Statistics reported 1.5 million unfilled hospitality positions through mid-2024 [1], and aggressive government digitization programs across East Asia that subsidize robotic automation in tourism infrastructure [2].

There is a structural technical change happening. Properties that once used manual housekeeping rosters, front-desk staffing models and traditional room-service logistics are now deploying integrated robotic platforms that use simultaneous localization and mapping (SLAM) navigation, large-language-model concierge engines and autonomous UV-C disinfection. The total investment in global venture finance for hotel automation has surpassed USD 2.1 billion from 2021 to 2024, with SoftBank Vision Fund and Sequoia Capital leading many Series B+ rounds [3].

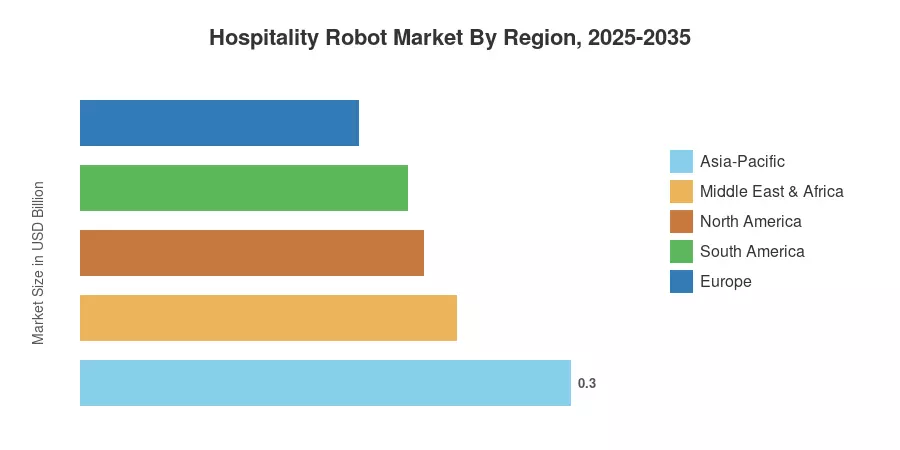

Asia-Pacific leads the Hospitality Robot Market, with over 38% of worldwide sales, led by manufacturing scale in China and early-adopter hotel chains in Japan and South Korea. North America is the fastest expanding region with 26.2% CAGR, driven by leading hotel groups in the U.S. and Canada launching fleet-wide robotic room service. Europe comes second with a share of 22%, with the support of funding from the EU Digital Europe Programme for smart-tourism projects [4]. The next decade will see deployment density shift from flagship luxury hotels to mid-tier and select-service firms looking for unit economics advantages.

Key Report Takeaways

• By Robot Type

- Delivery robots command the largest share of the Hospitality Robot Market at approximately 35% of 2025 revenue, reflecting high-frequency use in room-service and F&B operations.

- Cleaning and disinfection robots are expanding at a 27.1% CAGR through 2035, propelled by post-pandemic hygiene mandates and guest-satisfaction benchmarks.

- Reception and concierge robots account for roughly USD 0.16 billion in 2025, gaining traction in airport hotels and large resort complexes.

• By End User

- Hotels and resorts represent the dominant end-user vertical in the Hospitality Robot Market, contributing 45% of total demand.

- Restaurants and food-service establishments are growing at the fastest pace, with a 26.8% CAGR forecast through 2035.

• By Region

- Asia-Pacific holds a 38% revenue share of the Hospitality Robot Market, anchored by deployments across China, Japan, and South Korea.

- North America is projected to reach USD 2.12 billion by 2035, as U.S. hotel operators accelerate fleet procurement.

- The Middle East & Africa region is recording a 28.5% CAGR, led by Saudi Arabia's Vision 2030 tourism investment program.

Hospitality Robot Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated approach combining bottom-up revenue estimates from 45+ robot OEMs, top-down demand modeling from hotel and restaurant operator capex surveys, and cross-validation against import/export customs data for autonomous service platforms [5].