Robotics Market Summary

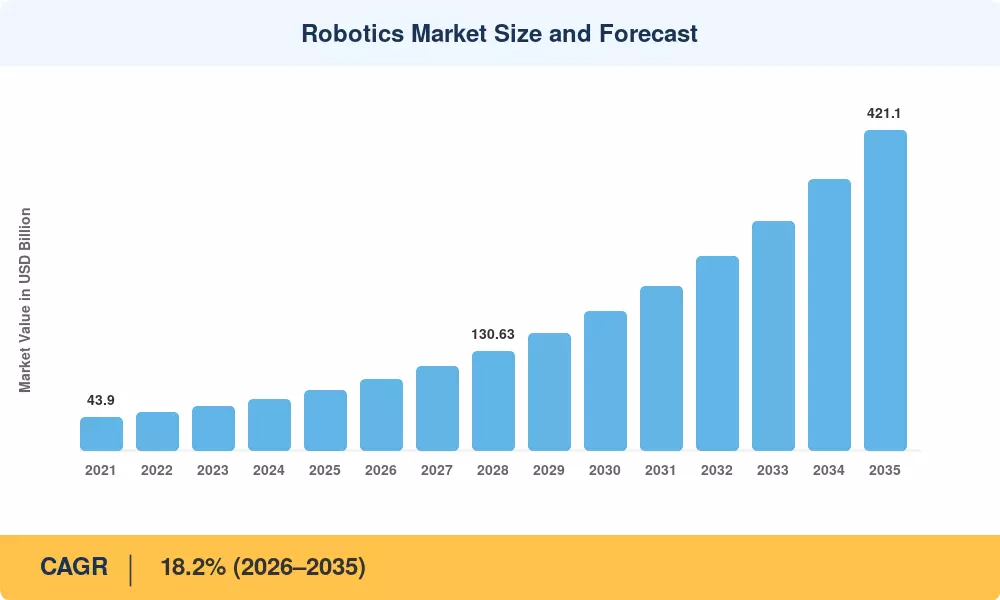

The global Robotics Market reached USD 79.10 Billion in 2025 and is projected to climb from USD 93.50 Billion in 2026 to USD 421.10 Billion by 2035, registering an 18.2% CAGR across the forecast window. Structural labor shortages across OECD economies, combined with government-backed reshoring mandates such as the U.S. CHIPS and Science Act and the EU Horizon Europe robotics allocations exceeding EUR 2.3 Billion, are converting automation from a discretionary upgrade into a strategic imperative [1][2]. This Robotics Market expansion is not cyclical — it reflects a permanent recalibration of how goods are manufactured, moved, and maintained.

A generational technology shift underpins the growth. Legacy fixed-sequence industrial arms are giving way to sensor-rich, AI-enabled platforms capable of real-time decision-making. Robot-as-a-Service (RaaS) contracts have lowered entry barriers for small and mid-sized enterprises, while component cost deflation — servo motor prices dropped roughly 14% between 2022 and 2024 — continues to improve unit economics [3]. Software intelligence now commands a rising share of total system value, unlocking recurring revenue for vendors that pair hardware with cloud-based analytics.

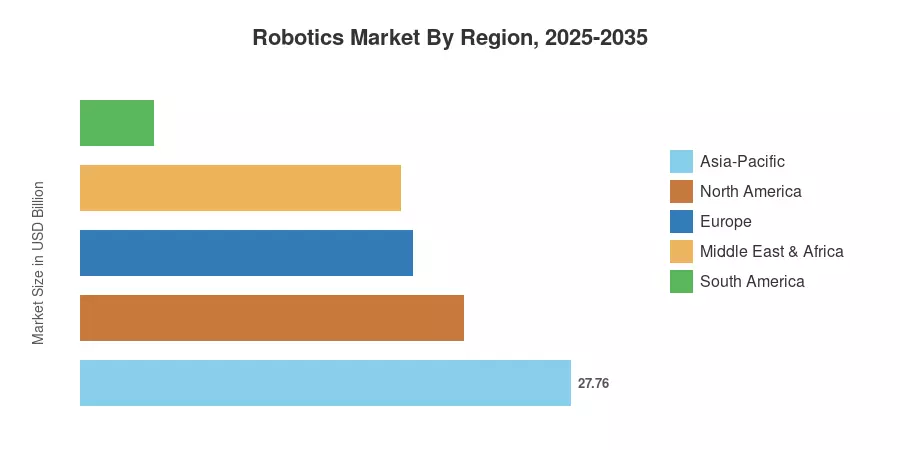

Asia-Pacific dominates the Robotics Market with an estimated 35.1% revenue share, anchored by China's installed base of over 1.5 million operational units and Japan's leadership in precision assembly robots [4]. The Middle East & Africa region is expanding fastest at a 22.9% CAGR, fueled by sovereign-wealth diversification programs in Saudi Arabia and the UAE. Europe holds the second-largest share at approximately 23.8%, supported by Germany's Industrie 4.0 framework and accelerating adoption in food-processing automation. The decade ahead will test whether supply chains can deliver enough skilled integrators to match surging demand.

Key Report Takeaways

• By Robot Type

- Industrial robots captured 66.2% of the Robotics Market revenue share in 2025, driven by automotive and electronics assembly demand.

- Collaborative robots are on track to register a 23.8% CAGR through 2035 as safety-rated designs open new floor-plan configurations for SMEs.

• By Component

- Hardware accounted for 58.7% of total Robotics Market value in 2025, though software is emerging as the fastest-growing component at a 21.3% CAGR.

- Services — spanning integration, maintenance, and training — represent the stickiest revenue layer for OEMs.

• By Application

- Logistics and warehousing held a 36.4% share of the Robotics Market in 2025, reflecting the e-commerce fulfilment build-out.

- Medical and surgical robotics are advancing at a 23.1% CAGR, propelled by minimally invasive procedure adoption.

• By End-User Industry

- Automotive led end-user segments with a 26.8% share in 2025.

- Healthcare providers are forecast to expand at a 23.2% CAGR, the fastest among all end-user verticals.

• By Region

- Asia-Pacific commanded 35.1% of the global Robotics Market share in 2025.

- The Middle East & Africa registers the quickest regional expansion at a 22.9% CAGR between 2026 and 2035.

Robotics Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining bottom-up revenue analysis of leading OEMs and integrators, top-down validation through national industrial automation statistics, and cross-referencing with trade association shipment data from the International Federation of Robotics (IFR). All forecast figures assume no major global recessionary shock and incorporate current policy trajectories for automation incentives.