Automotive Robotics Market Summary

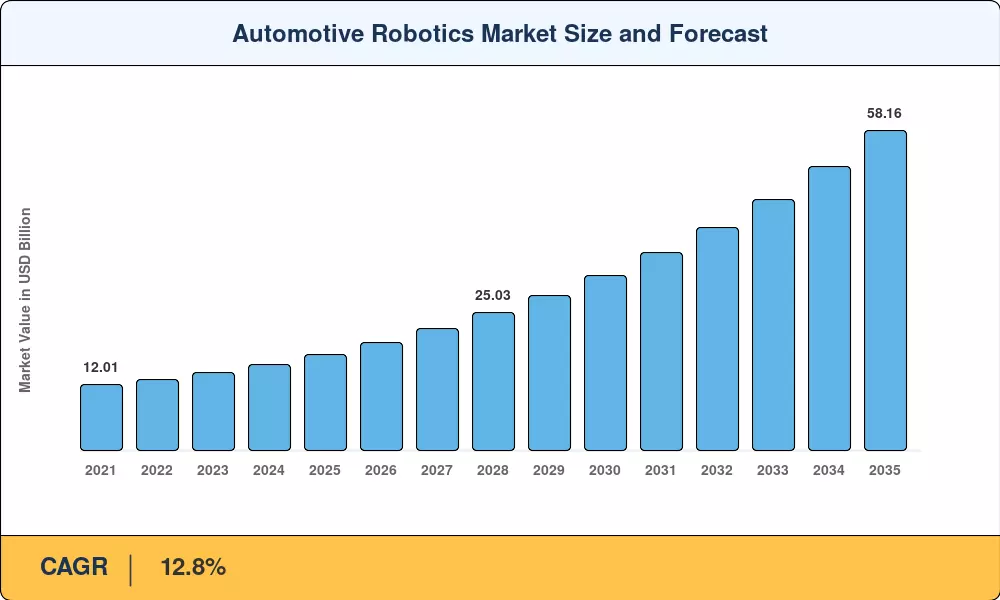

The Automotive Robotics Market reached a valuation of USD 17.42 billion in 2025 and is projected to climb from USD 19.67 billion in 2026 to USD 58.16 billion by 2035, expanding at a CAGR of 12.8% across the forecast window. The Automotive Robotics Market growth trajectory is anchored by two converging forces: the global push toward vehicle electrification — with over 40 countries committing to zero-emission vehicle mandates by 2035 [1] — and a structural shortage of skilled manufacturing labor that has made automation an operational necessity rather than a strategic luxury.

A generational technology shift is reshaping production floors worldwide. Legacy fixed-sequence robotic cells designed for internal-combustion drivetrain assembly are giving way to reprogrammable articulated and collaborative platforms capable of handling EV battery module stacking, e-powertrain mating, and full-body dimensional verification. The International Federation of Robotics recorded 136,000 new industrial robot installations in the automotive sector in 2023 alone, a 9% year-over-year jump that signals broadening adoption beyond premium OEMs into mass-market assembly [2].

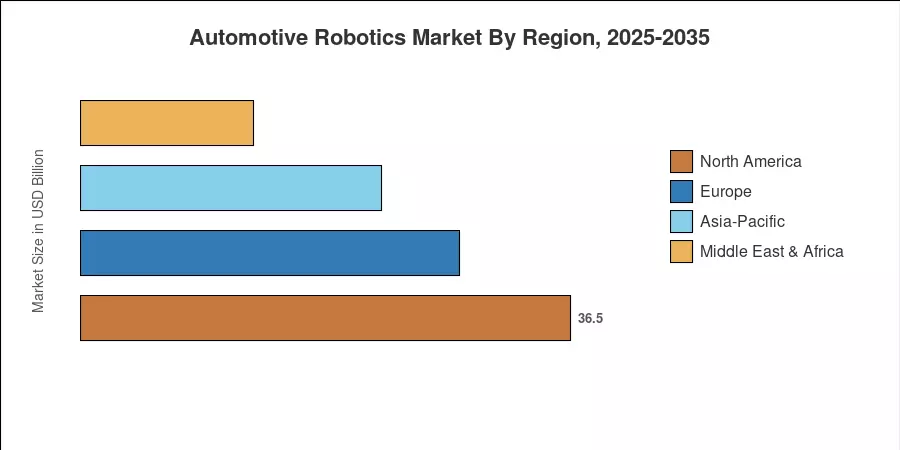

Asia-Pacific dominates the Automotive Robotics Market with an estimated 42.9% revenue share in 2025, driven by China's aggressive factory modernization programs and Japan's robotics export ecosystem. North America holds the second-largest position at roughly 24% share, buoyed by reshoring incentives under the U.S. Inflation Reduction Act. South America emerges as the fastest-growing region at a 15.6% CAGR through 2035, fueled by greenfield EV assembly plants in Brazil and Argentina. The next decade will see robotics density in automotive plants double from current levels, fundamentally redefining what a competitive production line looks like.

Key Report Takeaways

• By Product Type

- Articulated robots captured a 52.9% revenue share within the Automotive Robotics Market in 2025, reflecting their versatility across body welding, painting, and heavy-payload handling tasks.

- Collaborative robots are projected to register a 15.1% CAGR through 2035, as OEMs embed them in flexible final-assembly and quality-inspection stations alongside human operators.

• By Function Type

- Welding robots accounted for the largest functional segment in 2025, underpinned by rising body-in-white complexity in multi-material EV architectures.

- Inspection and quality-testing systems post the fastest functional growth, reflecting OEM mandates for 100% inline dimensional verification.

• By Region

- Asia-Pacific commanded the dominant position in the Automotive Robotics Market in 2025, with China alone representing over half of regional robot deployments.

- South America is the fastest-growing geography through 2035, propelled by new EV assembly capacity in Brazil.

Automotive Robotics Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates bottom-up shipment data from robot OEMs, top-down macroeconomic indicators (automotive capex, EV production ramp curves), and qualitative input from 45+ industry interviews conducted in 2024–2025. Historical figures (2021–2024) rely on audited company filings and customs-trade databases; forecast values (2026–2035) apply a calibrated compound growth framework validated against regional manufacturing census data.