Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Product Type | Articulated Robots, SCARA Robots, Collaborative Robots, Cartesian Robots | Articulated Robots (52.9% share, 2025) | Collaborative Robots (15.1% CAGR) |

| By Function Type | Welding Robots, Painting Robots, Assembly Robots, Material-Handling Robots, Inspection & Quality-Testing | Welding Robots (43.1% share, 2025) | Inspection & Quality-Testing (13.1% CAGR) |

| By Component Type | Robotic Arms, Controllers, End-Effectors, Automotive Robotics Market & Services | Robotic Arms (38.5% share, 2025) | Automotive Robotics Market & Services (13.4% CAGR) |

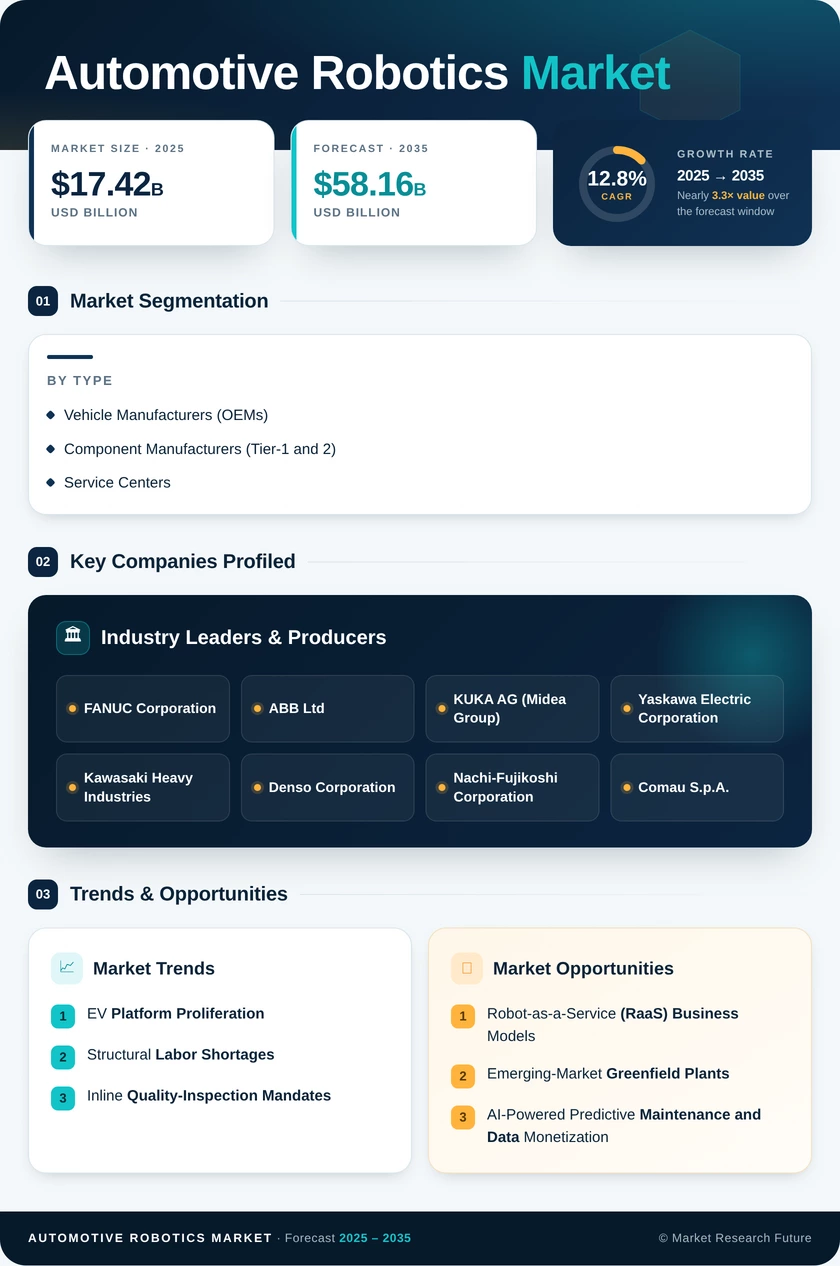

| By End-User Type | Vehicle Manufacturers (OEMs), Component Manufacturers (Tier-1 and 2), Service Centers | Vehicle Manufacturers (56.5% share, 2025) | Service Centers (13.0% CAGR) |

| By Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | Asia-Pacific (42.9% share, 2025) | South America (15.6% CAGR) |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Articulated Robots | Six-axis platforms are gaining AI-enabled adaptive path planning for multi-material BEV body assembly |

| SCARA Robots | High-speed pick-and-place expanding into EV power-electronics module insertion |

| Collaborative Robots | Price erosion below USD 40,000 per unit, opening Tier-1 and aftermarket service adoption |

| Cartesian Robots | Linear-motion dispensing and sealing systems integrating vision-guided bead inspection |

Articulated robots remain the backbone of automotive body shops globally, prized for their reach, payload capacity, and kinematic flexibility. Collaborative robots represent the most dynamic growth vector, steadily moving from pilot programs into series-production roles across final assembly and quality verification.

By Function Type

| Sub-Segment | Key Trend |

| Welding Robots | Laser and friction-stir welding cells replacing resistance spot welding for mixed-material BEV bodies |

| Painting Robots | Electrostatic bell-cup atomizers improve transfer efficiency above 90% |

| Assembly Robots | Battery-pack and e-axle mating tasks requiring sub-millimeter repeatability |

| Material-Handling Robots | Heavy-payload transfer systems integrating with autonomous mobile robot fleets |

| Inspection & Quality-Testing | 3D laser scanning and AI defect classification enabling 100% inline verification |

Welding remains the highest-revenue function owing to the structural volume of body-in-white operations across the global vehicle fleet. Inspection and quality-testing cells are closing the gap as OEM mandates for zero-defect output push adoption across all production tiers.

By Component Type

| Sub-Segment | Key Trend |

| Robotic Arms | Lightweight carbon-fiber-reinforced arm designs reduce energy consumption |

| Controllers | Edge-AI chipsets enabling real-time adaptive motion control at the cell level |

| End-Effectors | Quick-change tooling systems supporting mixed-model production flexibility |

| Automotive Robotics Market & Services | Cloud-based simulation, OTA updates, and Robot-as-a-Service subscriptions |

Robotic arms account for the largest hardware share, but software and services are capturing an increasing proportion of total spend as OEMs prioritize digital-twin simulation, predictive analytics, and subscription-based deployment models.

By End-User Type

| Sub-Segment | Key Trend |

| Vehicle Manufacturers (OEMs) | Full-line automation from stamping through final assembly for BEV-dedicated plants |

| Component Manufacturers (Tier-1 and 2) | OEM-mandated automation thresholds flowing down to supplier operations |

| Service Centers | High-voltage EV battery diagnostic and repair cells are entering early adoption |

Vehicle manufacturers remain the dominant end-user, deploying robots across the full manufacturing value chain. Service centers represent a nascent but rapidly emerging segment as the growing EV parc creates demand for automated high-voltage battery servicing and recalibration.

By Geography

| Sub-Segment | Key Trend |

| Asia-Pacific | China's NEV mandate and Japan's robot-export ecosystem sustain regional dominance |

| North America | IRA credits and OEM reshoring investment drive double-digit growth |

| Europe | Net-Zero Industry Act and OEM BEV platform transitions accelerate adoption |

| South America | Brazilian greenfield EV plants position the region as the fastest-growing geography |

| Middle East & Africa | Saudi Vision 2030 and UAE free-zone strategies establish early automation footholds |

Asia-Pacific's leadership reflects both the world's largest vehicle production base and a mature domestic robotics supply chain anchored by FANUC, Yaskawa, and an expanding cohort of Chinese manufacturers. South America's greenfield advantage — building automation-native plants without legacy infrastructure constraints — underpins its status as the fastest-growing regional market through 2035.