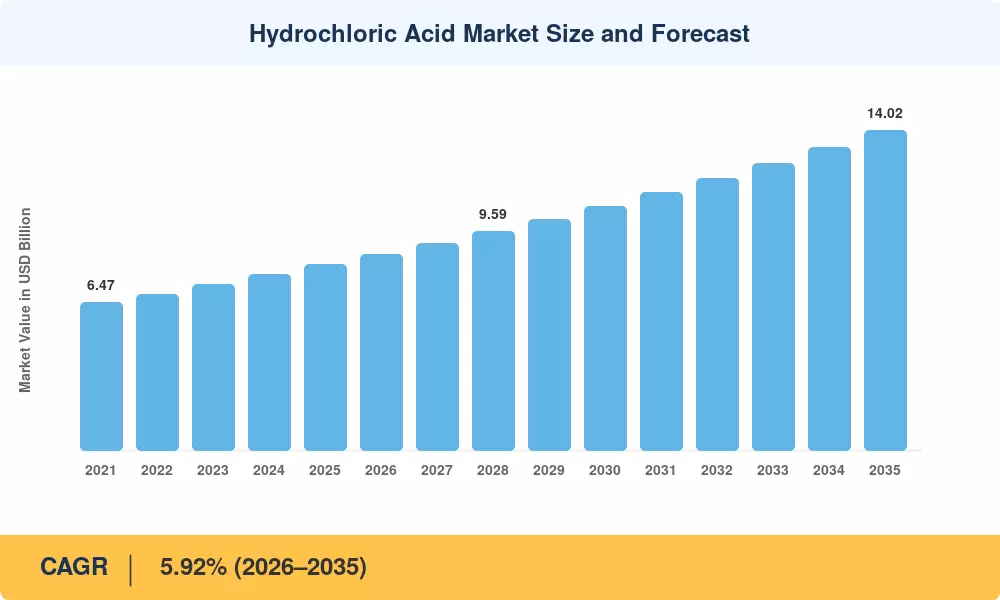

Hydrochloric Acid Market Summary

The Hydrochloric Acid Market reached an estimated 8.15 million tons in 2025, with the forecast period beginning at 8.59 million tons in 2026 and climbing to 14.02 million tons by 2035 at a CAGR of 5.92%. This expansion is rooted in a convergence of semiconductor fabrication build-outs, accelerated oil well acidizing activity tied to unconventional gas plays, and tightening water treatment standards that require reliable pH control chemicals across municipal and industrial facilities [1]. Governments in the United States, China, and India have committed over USD 180 billion collectively to semiconductor self-sufficiency programs through 2030, each of which drives demand for ultra-high-purity inorganic acid compounds used in wafer cleaning and etching steps [2].

A structural shift is underway in how chemical processing acids are produced and consumed. Legacy mercury-cell chlor-alkali plants — once responsible for roughly 15% of European muriatic acid output — are being decommissioned under the EU Mercury Regulation, replaced by membrane-cell technology that produces higher-purity hydrochloric acid at lower energy intensity [3]. This transition has spurred over EUR 4.2 billion in membrane retrofits since 2021, simultaneously improving product quality for steel pickling chemicals and electronic-grade applications while raising the capital bar for smaller merchant producers [4].

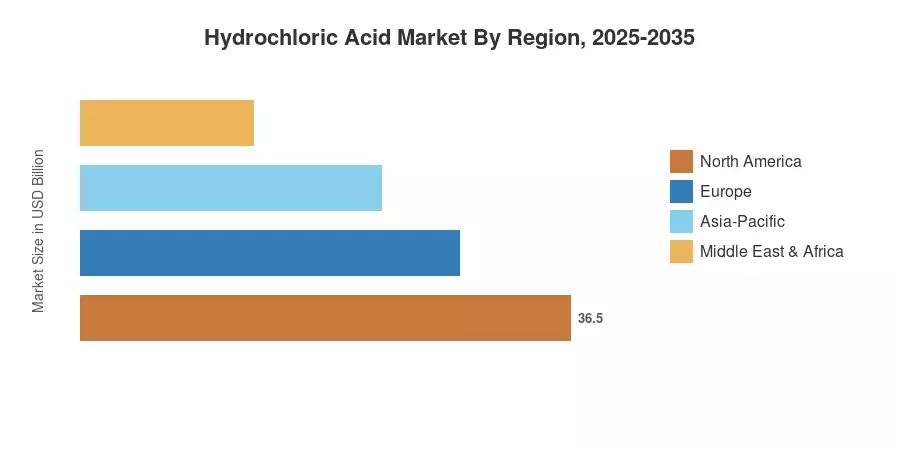

Asia-Pacific commands roughly 56% of global volume, driven by China's chlor-alkali overcapacity and India's expanding pharmaceutical intermediate sector. The region also posts the fastest CAGR at 6.28% through 2035. North America holds the second-largest share at approximately 21%, anchored by Gulf Coast petrochemical clusters and shale-gas stimulation demand. Europe contributes around 16% of volume, with growth tied to industrial cleaning chemicals for automotive steel processing. As battery-recycling hydrometallurgy scales globally, the Hydrochloric Acid Market is poised for sustained demand diversification well into the next decade

Key Report Takeaways

• By Grade

- Industrial-grade hydrochloric acid held 57% revenue share in 2025, underpinned by steel pickling chemicals and water treatment acids demand across heavy industries

- Ultra-high-purity grades are projected to grow at a 6.35% CAGR through 2035, driven by sub-5 nm semiconductor fabs requiring parts-per-trillion metal specifications

• By End-User Industry

- The chemicals segment captured 34.5% of the Hydrochloric Acid Market share in 2025, reflecting its role in organic and inorganic acid compounds synthesis

- Oil and gas end users are expanding at a 6.58% CAGR as oil well acidizing operations intensify in North American shale basins

• By Region

- Asia-Pacific accounted for 56% of volume in 2025, led by Chinese chlor-alkali co-production and Indian pharmaceutical manufacturing

- North America's Hydrochloric Acid Market is valued at approximately 1.71 million tons in 2025, supported by chemical processing acids demand along the Texas–Louisiana corridor

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up production data from chlor-alkali plant databases, trade-flow analysis from UN Comtrade, and top-down validation against published industry association statistics. Historical figures (2021–2024) reflect actual shipment records, while the 2025 base year blends preliminary production reports with demand-side consumption audits. Forecast values (2026–2035) apply the calibrated CAGR with adjustments for announced capacity additions and regulatory phase-outs.