Identity Governance and Administration Market Summary

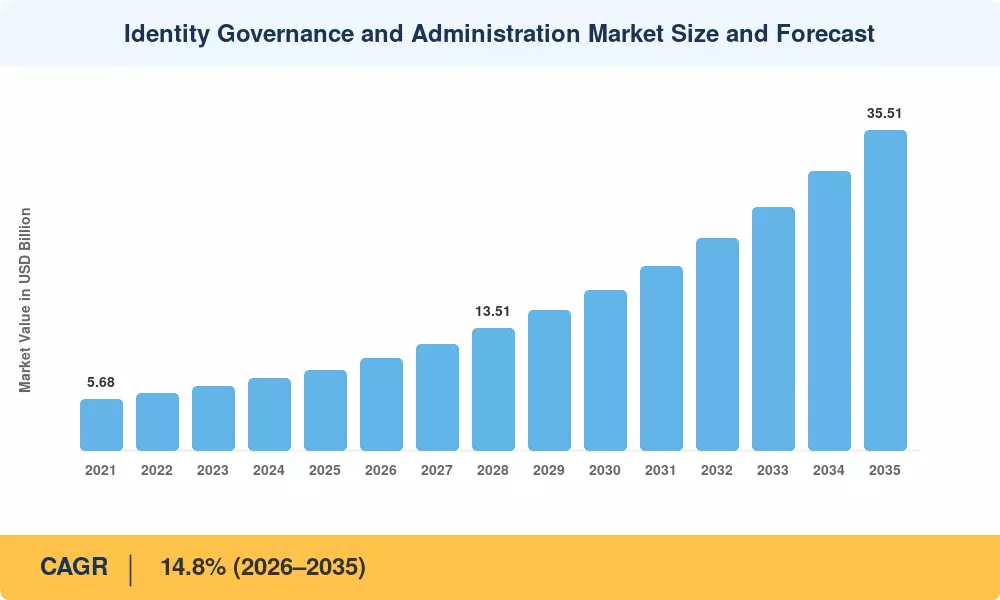

The Identity Governance and Administration Market reached USD 8.93 Billion in 2025, reflecting sustained enterprise investment in centralized access oversight platforms. Market Research Future projects the Identity Governance and Administration Market will grow from USD 10.25 Billion in 2026 to USD 35.51 Billion by 2035, registering a CAGR of 14.8% across the forecast period. Two catalysts are accelerating this trajectory: the U.S. Executive Order on Improving the Nation's Cybersecurity (EO 14028) and the European Union's Digital Operational Resilience Act (DORA), both of which mandate verifiable identity controls for critical-infrastructure operators [1][2].

Legacy directory-based provisioning workflows—often stitched together with custom scripts and spreadsheets—are giving way to AI-driven governance platforms that automate access certification, detect policy violations in real time, and integrate with multi-cloud directories. estimates that 65% of mid-market enterprises will retire manual access-review processes by 2028, redirecting an estimated USD 4.2 billion in annual compliance labor toward automated identity analytics [3]. This technology shift is converting what was once a compliance checkbox into a strategic security function.

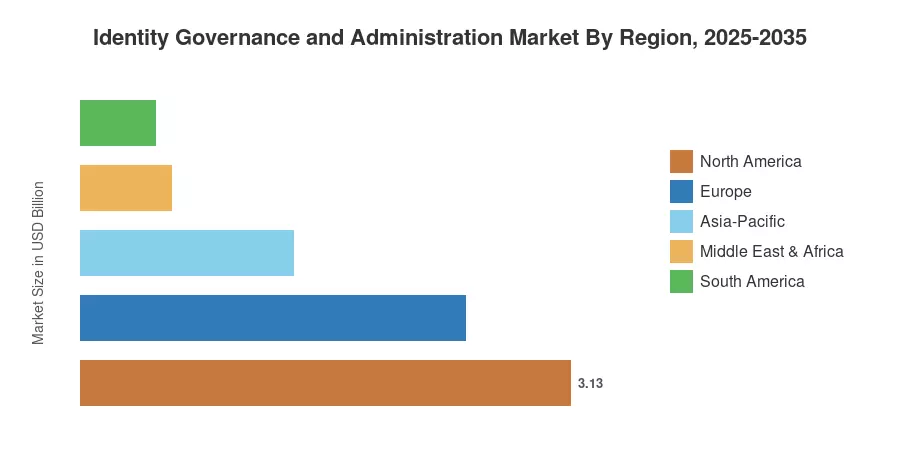

North America held roughly 35.1% of global Identity Governance and Administration Market revenue in 2025, anchored by federal zero-trust mandates and a mature vendor ecosystem. Asia-Pacific is the fastest-growing region at a projected CAGR of 15.2%, propelled by India's Digital Personal Data Protection Act and China's expanding cybersecurity-review regime. Europe accounts for the second-largest share at approximately 27.5%, driven by GDPR enforcement actions and DORA readiness spending. As hybrid-work architectures persist and regulatory complexity deepens, the Identity Governance and Administration Market is positioned for a decade of double-digit expansion.

Key Report Takeaways

• By Component

- Solutions commanded 61.2% of Identity Governance and Administration Market revenue in 2025, led by platforms embedding AI-based role-mining and automated policy orchestration.

- Services are expanding at a 14.9% CAGR through 2035 as skill-constrained enterprises outsource deployment, integration, and managed governance operations.

• By Deployment Mode

- Cloud deployment captured the dominant share in 2025, as organizations prioritize SaaS-delivered governance to accelerate time-to-value and reduce on-premise infrastructure burdens.

- On-premise installations retain relevance in regulated verticals—particularly defense and government—where sovereign data-residency obligations limit cloud migration.

• By Region

- North America generated the largest regional revenue, reflecting early federal zero-trust adoption and deep vendor penetration across financial services.

- Asia-Pacific is on track for the highest regional CAGR during 2026–2035, fueled by rapid digitalization in banking, telecom, and government sectors across India, Japan, and South Korea.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model blends bottom-up vendor-revenue tracking, top-down TAM analysis calibrated against enterprise IT-security spending ratios, and cross-validation with procurement data from 1,400+ enterprises surveyed between 2023 and 2025. Historical figures (2021–2024) rely on audited company filings and regulatory disclosures; forecast values (2026–2035) apply the calibrated 14.8% CAGR to the base-year estimate, adjusted for anticipated regulatory and technology inflections.