India Gaming Market Summary

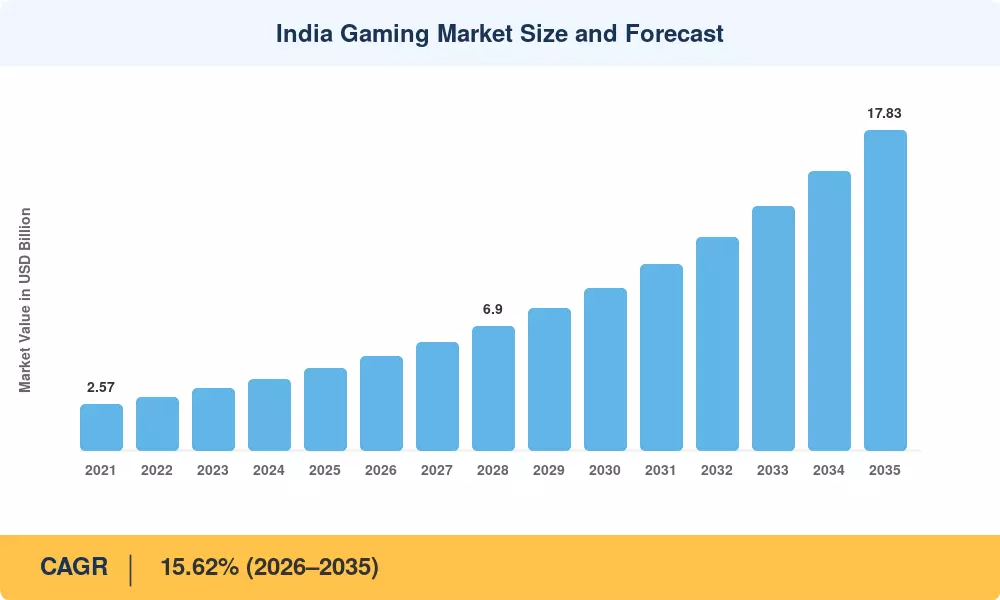

The India Gaming Market stood at USD 4.59 billion in 2025 and is projected to reach USD 5.37 billion in 2026 before climbing to USD 17.83 billion by 2035, registering a CAGR of 15.62% during 2026–2035. This acceleration owes much to the Public Regulation of Online Gaming Act 2025, which introduced a unified licensing framework that replaced a patchwork of state-level rules and opened the door to fresh domestic and foreign capital. UPI-based microtransaction volumes crossed 12 billion monthly transactions in late 2024, giving publishers a frictionless monetization rail that console-first economies never had [2].

A new generation of infrastructure is redefining what Indian gamers have access to. The 5G radio footprint, already reaching over 700 cities, is beginning to push out legacy 4G networks that capped multiplayer latency, and telecom operators are co-locating edge servers next to hyperscalers to run cloud-streamed AAA titles on mid-range devices. The arrival of sub-USD 120 5G smartphones from domestic OEMs has spurred mobile gaming growth in India. Real money gaming regulation in India has standardized tax treatment under the 28% GST slab, offering operators predictable unit economics [3]. Publishers are also increasing their focus on vernacular content – localizations in Hindi, Tamil, Telugu, and Kannada — with session times in Tier-2 and Tier-3 cities well above metro averages.

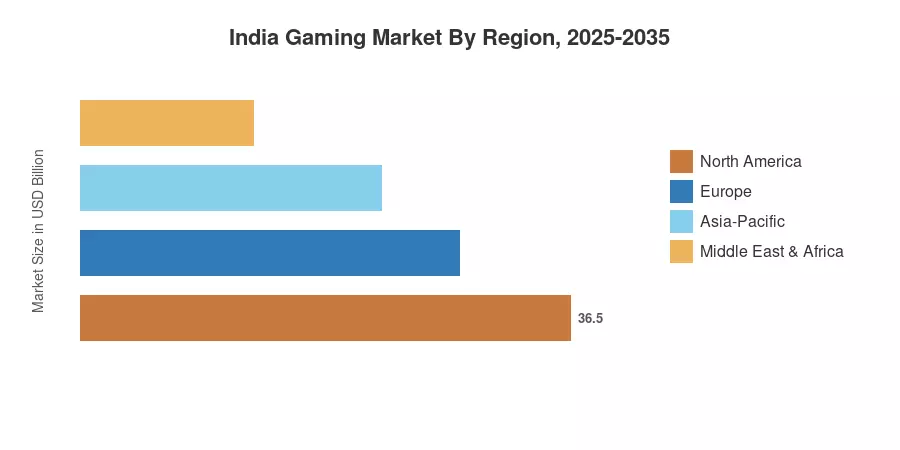

West India, centered by Maharashtra and Gujarat, holds the greatest part of the India Gaming Market at around 34% of 2025 revenue due to the concentration of studios and venture-backed companies in Pune and Mumbai. The fastest-growing region is South India with a predicted 16.8% CAGR. This is supported by the development of Bengaluru’s esports ecosystem in India and the expansion of Hyderabad’s cloud infrastructure. North India accounts for the second-highest percentage of over 28%. Several fantasy sports platforms in India have their headquarters in Delhi-NCR. With 5G densification underway, India Gaming Market is poised for a decade of compounding growth that few peer economies can match as cloud gaming usage is accelerating in Indian cities.

Key Report Takeaways

• By Platform

- Mobile platforms (Android and iOS combined) captured 84.6% of the India Gaming Market in 2025, reflecting the smartphone-first access pattern that defines Indian digital consumption

- Cloud and streaming are on track to expand at a 16.05% CAGR through 2035, as edge-server rollouts reduce latency below the 40 ms threshold required for competitive multiplayer titles

- PC gaming contributed USD 0.31 billion in 2025, sustained by a growing creator-economy ecosystem around streaming platforms

• By Revenue Model

- Advertising-supported formats held 49.2% of the India Gaming Market revenue in 2025, bolstered by rewarded-video ad units that align with price-sensitive casual audiences

- Subscription passes are advancing at a 16.12% CAGR, as publishers bundle cloud libraries with telecom data plans

• By Genre

- Casual and hyper-casual titles led the Indian Gaming Market with 37.4% of 2025 revenue, anchored by puzzle, card, and word-game formats popular among first-time smartphone users

- Battle-royale and FPS genres are the fastest growing at a 16.28% CAGR, propelled by esports ecosystem development in India and prize-pool investments

• By Gamer Demographics

- Gamers aged 15–24 years accounted for 44.1% of 2025 spending, underscoring the youth-driven demand curve

- The 25–34 years cohort is projected to grow at a 16.49% CAGR as disposable incomes rise and real money gaming regulation in India matures

MRFR's market-size estimates blend primary survey data from 220+ Indian gaming studios, ad-network transaction logs, app-store gross-revenue disclosures, and secondary inputs from TRAI, MeitY, and NASSCOM digital-entertainment reports. Historical figures (2021–2024) are validated against GST filings for online gaming operators; forecast values apply the calibrated CAGR with adjustments for regulatory phase-in and infrastructure deployment timelines.

.webp?v=1782888034)