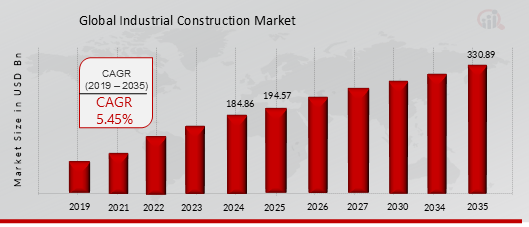

Global Industrial Construction Market Overview

Industrial Construction Market Size Was Valued at USD 184.86 Billion In 2024. The Global Industrial Construction Industry Is Projected to Grow from USD 194.57 Billion In 2025 To USD 330.89 Billion By 2035, Exhibiting A Compound Annual Growth Rate (CAGR) Of 5.45% During the Forecast Period (2025 - 2035).

Rapid Urbanization and Industrialization, Green Building Standards and Decarbonization Goals and Drivers Impact Analysis Is Driving the Industrial Construction Market.

As per Analyst at MRFR,” The industrial construction industry always changes depending upon the economic, technical, and legislative forces. With the fast industrialization and infrastructure development, along with global trends towards clean energy, demand for industrial facilities across the manufacturing, chemicals, energy, and pharmaceutical industries is on the rise. Technology has been making the industry more and more efficient—this includes the things like Building Information Modeling (BIM), automation, and modular construction”

Source: Secondary Research, Primary Research, Market Research Future Database, and Analyst Review

Industrial Construction Market Trends

GROWTH IN RENEWABLE ENERGY INFRASTRUCTURE

The high-stakes Industrial Construction Market has a once-in-a-lifetime opportunity in the exponential growth of renewable energy infrastructure. Countries are committing to reducing emissions and have begun transitioning from fossil fuels, this will mean both sizeable investments into solar, wind, hydrogen, and battery storage facilities. Governments throughout the world and private sector investments have rolled out, often the largest-scale clean energy investment projects ever in recent times, and are all designed with multiple and significant purpose: to maximize climate goals, to enhance energy security, and to build back economies that are sustainable and representative of real growth.

The European Union’s Green Deal and the U.S. Inflation Reduction Act (IRA) alone have potentially added billions of new dollars of funding to renewable energy development, and the utility scale solar and wind facilities being deployed in China and India alone at an aggressive pace are some of the most sizeable electricity present demand solutions on the planet.

With these renewable energy projects and a global scope, there is a significant growth opportunity for industrial construction services associated with many elements of the build-out including Engineering, Procurement and Construction (EPC) of greenfield renewable energy sites, retrofitting of existing facilities, substation build-outs, transmission lines (new and upgrades), energy storage infrastructure, and other supporting renewable infrastructural services.

Also, the emergence of green industrial parks, and net-zero manufacturing hubs, expands the market opportunity for contract and consulting construction firms who are developing some degree of knowledge and proficiency in sustainable design and low or zero-carbon technologies. Construction firms that are willing to lean into this transition into renewable energy solutions, invest in trained labour, invest/embrace new digital and hybrid tools, products, and materials, will reap the economic, environmental, and personal rewards in the coming months and years ahead.

Industrial Construction Market Segment Insights

Global Industrial Construction By Construction Type Insights

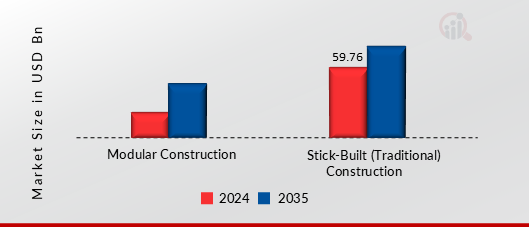

Based on construction type, Industrial Construction Market is segmented into Modular Construction,(Permanent Modular Construction (PMC) ,Relocatable Modular Buildings) , Stick-Built (Traditional) Construction ( Concrete Frame Construction, Steel Frame Construction, Wood Frame Construction). The Stick-Built (Traditional) Construction segment dominated the global market in 2024, while the Modular Construction is projected to be the fastest–growing segment during the forecast period.

Stick-built or traditional construction is a method of building on-site by assembling the parts (component by component). This method is still the most common, and prevalent method of industrial construction because of the flexibility in design and decor materials. Stick-built construction is used for large custom-built facilities like manufacturing plants, warehouses, or power stations.

The stick-built form of construction will always follow the complexity of a design that is site-specific. It allows integrated infrastructure in relation with the surrounding infrastructure, although it can take a long time to construct and can be subjected to adverse weather that could cause delays. The traditional construction method will withstand the weather and provide structural integrity and longer lifespan even if changes are experienced in both construction and engineering.

Figure 1: Industrial Construction Market, By Construction Type, 2024 & 2035 (USD Billion)

Global Industrial Construction By Building Type Insights

Based on building type, Industrial Construction Market is segmented into Manufacturing Plants ( Automotive, Electronics, Food Beverage) ) , Warehouses Distribution Centers, Data Centers, Clean Rooms / Laboratories, Power Energy Facilities, Waste Water Treatment Plants. The Structural Systems segment dominated the global market in 2024, while the Pre-Engineered Components is projected to be the fastest–growing segment during the forecast period.

Context is king in all aspects of design. Manufacturing facilities are essential to the industrial construction space, built purposely for the production of things at scale. The design of a manufacturing facility has its own set of challenges, because at times they provide for either extremely complicated machinery or these bulky flows of creating goods. In addition to the machinery it also must incorporate workflows to store materials and assurances for the safety of employees as well.

Projects of this type give heavy use to higher structure requirements (high volume and high load), differentiated flooring systems, and lots of electrical and mechanical systems.

Manufacturing facilities are also typically subject to rigorous environmental, health, and safety criteria. In the new era of manufacturing, the design and construction of auto plants now typically emphasize automation, energy efficiency, and lean manufacturing plans. In view of all of this, these new facilities must really begin with regional demand, access to raw material, and especially now with supply chain logistics for how and where these facilities will be build. The world is shifting to Industry 4.0 and we are even developing the plans as constructs become smarter.

Global Industrial Construction By Component Type Insights

Based on By Component Type, the Industrial Construction Market has been segmented into Structural Systems, Interior Build-Out, Mechanical, Electrical, and Plumbing (MEP), Pre-Engineered Components, On-Site Built Components. The Structural Systems segment dominated the global market in 2024, while the Mechanical, Electrical, and Plumbing (MEP) is projected to be the fastest–growing segment during the forecast period.

Structural systems typically make up the physical framework of an industrial facility. Structural systems are the combination of the foundations, beams, columns, slabs and load bearing walls that are engineered to support the weight the building, prevent lateral forces like wind and seismic and accommodate the loads of heavy machinery operations. Structural systems will use materials successfully used as a part of other similar types of work. Common materials used are steel, reinforced concrete and precast materials. The combination and configuration, for each job, will depend on the size and operational use of the facility.

The design of the structural systems is critical to the building's safety, lifespan and capacity to be adaptable for future use. Structural systems for industrial structures need to accommodate long open spans, tall ceilings, heavy-duty operations all while allowing the future sustainability for plant expansions, modifications or simplifications. Advanced design tools are increasingly being used, for example, BIM (Building Information Modeling), which provide high levels of precision and the ability to easily coordinate with the other associated systems in the construction phase.

Increasingly modular and sustainable building materials have focused designer and builder attention to minimize costs while reducing the environmental impact to our surroundings.

Global Industrial Construction By End-Use Insights

Based on By End-Use, the Industrial Construction Market has been segmented into Oil & Gas, Pharmaceutical, Food Processing, Automotive, Aerospace, Logistics, Chemicals, Utilities Infrastructure. The Logistics segment dominated the global market in 2024, while the Utilities Infrastructure is projected to be the fastest–growing segment during the forecast period.

Logistics construction supports the warehousing, transportation, and delivery of products. Key project types are distribution centers, cross-dock terminals, and freight hubs. Modern logistics buildings emphasize clear heights, large open floor areas, strong floor slabs, and sophisticated automated systems, such as AS/RS and conveyor networks. Locations with access to highways, ports, and urban centers offer the best last-mile delivery potential. The global e-commerce boom has further increased spending on logistics infrastructure. These investments want fast build time and scalable and flexible facilities.

Sustainable buildings with integration of sustainable resources and smart energy paradigms are becoming a standard expectation in logistics real estate development.

Global Industrial Construction Regional Insights

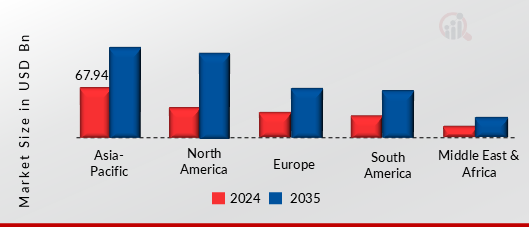

Based on Region, the Global Industrial Construction is segmented into North America, Europe, Asia-Pacific, South America, Middle East & Africa. The Asia Pacific dominated the global market in 2024, while the Asia-Pacific is projected to be the fastest–growing Region during the forecast period.

Asia Pacific is the fastest growing region in the Industrial Construction Market, led by China, India, Japan and Southeast Asia. China still remains the elephant in the room by an overwhelming distance with its massive investment in manufacturing, energy and logistics infrastructure across the country, underpinned by new regulations intended to legitimate a new, sustainable economy. The 'economic rebalancing' is manifesting itself through sharp upticks in neighbouring countries.

India is nurturing its industrial base and making a significant piece of it through its involuntary commitment to Build in India, driven by increased foreign direct investment (FDI) and heightened demand for electronics, electric vehicles and pharmaceuticals.

Southeast Asia is being favoured by companies who are diversifying away from China offering an emerging industrial construction opportunity. All industrial construction in the Asia Pacific region will continue to experience growth driven by urbanisation, population, and digitalisation. The industrial warehousing for food, beverages and essentials (e.g. pharmaceuticals), data centres and renewable energy plants are key growth areas. Further, there is a relatively cheap and skilled workforce within the region, as well as government support to attract private sector investment.

There are real opportunities within the region but there are potential challenges to project timelines and schedules of other tasks from disruption to supply chains or lack of policy clarity or constraints from humanitarian or mechanical issues in general.

Figure 2: Industrial Construction Market, By Region, 2024 & 2035 (USD Billion)

Further, the major countries studied in the market report are the U.S., Canada, Mexico, Germany, , Germany, U.K., France, Italy, Spain, Russia, Rest of Europe, China, Japan, India, Australia, Indonesia, South Korea, Rest of Asia Pacific , GCC , South Africa, Rest of Middle East & Africa , Brazil , Chile, Rest of South America .

Global Industrial Construction Key Market Players & Competitive Insight

Many global, regional, and local vendors characterize the Industrial Construction Market. The market is highly competitive, with all the players competing to gain market share. Intense competition, rapid advances in technology, frequent changes in government policies, and environmental regulations are key factors that confront market growth. The vendors compete based on cost, product quality, reliability, and government regulations. Vendors must provide cost-efficient, high-quality products to survive and succeed in an intensely competitive market.

The major players in the market include Laing O’ROURKE, Red Sea International, Atco Ltd, Bouygues Construction, Skanska, KLEUSBERG GMBH & Co. Kg, Fluor Corporation, AECOM, Vinci Group, Turner Construction Company, And Among Others. The Industrial Construction Market is a consolidated market due to increasing competition, acquisitions, mergers and other strategic market developments and decisions to improve operational effectiveness.

Key Companies in the Industrial Construction Market include.

- Laing O’ROURKE

- Red Sea International

- Atco Ltd

- Bouygues Construction

- Skanska

- KLEUSBERG GMBH & Co. Kg

- Fluor Corporation

- AECOM

- Vinci Group

- Turner Construction Company

Industrial Construction Market Industry Developments

-

Q3 2025: Toyota completed Phase 1 of construction on "Woven City" in late 2024, and is scheduling a fall 2025 launch. Toyota has finished the first phase of its Woven City project, a smart city initiative, and plans to launch the facility in fall 2025 to test mobility innovations with actual citizens.

-

Q3 2025: Total construction starts were up 16 percent in June 2025 to a seasonally adjusted annual rate of $1.33 trillion, driven by strength in manufacturing and data center construction. Manufacturing and data center construction led a surge in new construction starts in June 2025, with nonresidential building starts improving 39 percent compared to the previous year.

Industrial Construction Market Segmentation

Industrial Construction Market By Construction Type Outlook (USD BILLION, 2019-2035)

-

Modular Construction

- Permanent Modular Construction (PMC)

- Relocatable Modular Buildings

-

Stick-Built (Traditional) Construction

- Concrete Frame Construction

- Steel Frame Construction

- Wood Frame Construction

Industrial Construction Market By Building Type Outlook (USD BILLION, 2019-2035)

-

Manufacturing Plants

- Automotive

- Electronics

- Food Beverage

- Warehouses Distribution Centers

- Data Centers

- Clean Rooms / Laboratories

- Power Energy Facilities

- Waste Water Treatment Plants

Industrial Construction Market By Component Type Outlook (USD BILLION, 2019-2035)

- Structural Systems

- Interior Build-Out

- Mechanical, Electrical, and Plumbing (MEP)

- Pre-Engineered Components

- On-Site Built Components

Industrial Construction Market By End-use Outlook (USD BILLION, 2019-2035)

- Oil & Gas

- Pharmaceutical

- Food Processing

- Automotive

- Aerospace

- Logistics

- Chemicals

- Utilities Infrastructure

Global Industrial Construction Regional Outlook

-

North America

-

Europe

- Germany

- Italy

- France

- UK

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Thailand

- Rest of APAC

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East

- GCC Countries

- South Africa

- Rest of MEA

|

Report Attribute/Metric

|

Details

|

|

Market Size 2024

|

USD 184.86 BILLION

|

|

Market Size 2025

|

USD 194.57 BILLION

|

|

Market Size 2035

|

USD 330.89 BILLION

|

|

Compound Annual Growth Rate (CAGR)

|

5.45% (2025-2035)

|

|

Base Year

|

2024

|

|

Market Forecast Period

|

2025-2035

|

|

Historical Data

|

2019- 2023

|

|

Market Forecast Units

|

Value (USD Billion)

|

|

Report Coverage

|

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends

|

|

Segments Covered

|

By Construction Type, By Building Type, By Component Type, By End-use

|

|

Geographies Covered

|

North America, Europe, Asia-Pacific, South America, Middle East & Africa.

|

|

Countries Covered

|

the U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Russia, Rest of Europe, China, Japan, India, Australia, Indonesia, South Korea, Rest of Asia Pacific, GCC, South Africa, Rest of Middle East & Africa, Brazil, Chile, Rest of South America.

|

|

Key Companies Profiled

|

Laing O’ROURKE, Red Sea International, Atco Ltd, Bouygues Construction, Skanska, KLEUSBERG GMBH & Co. Kg, Fluor Corporation, AECOM, Vinci Group, Turner Construction Company

|

|

Key Market Opportunities

|

· Growth In Renewable Energy Infrastructure

|

|

Key Market Dynamics

|

· Rapid Urbanization and Industrialization

· Green Building Standards and Decarbonization Goals

|

Frequently Asked Questions (FAQ):

The Industrial Construction Market size is expected to be valued at USD 330.89 Billion in 2035.

The global market is projected to grow at a CAGR of 5.45% during the forecast period, 2025-2035.

Asia Pacific had the largest share of the global market.

The key players in the market are Astec Industries Laing O’ROURKE, Red Sea International, Atco Ltd, Bouygues Construction, Skanska, KLEUSBERG GMBH & Co. Kg, Fluor Corporation, AECOM, Vinci Group, Turner Construction Company, And Among Others.

Stick-Built (Traditional) Construction Systems Industrial Construction dominated the market in 2024.

Logistics Segment had the largest revenue share of the global market.