Industrial Lubricants Market Summary

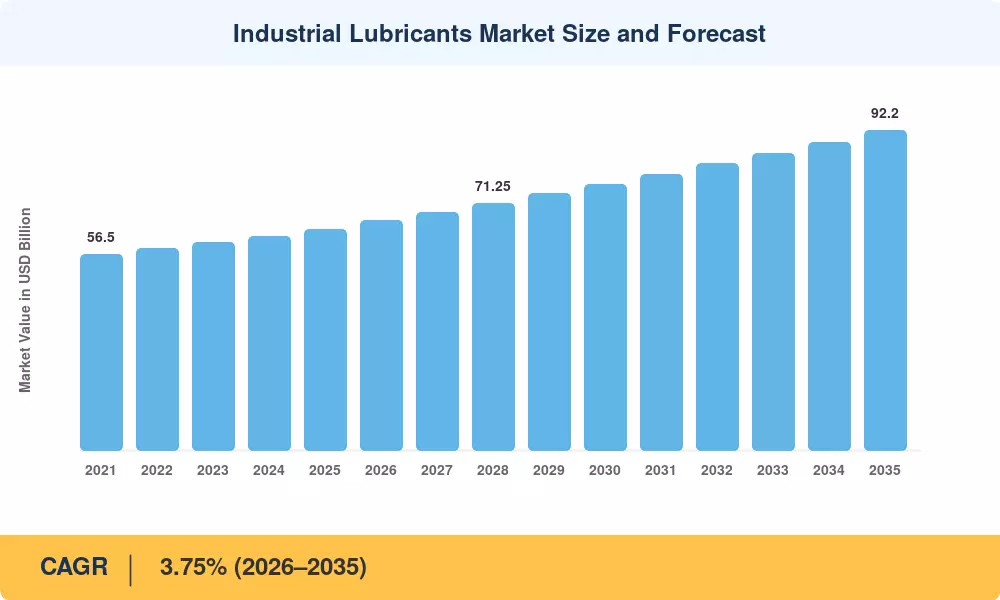

The Industrial Lubricants Market reached an estimated USD 63.80 billion in 2025 and is projected to grow from USD 66.19 billion in 2026 to USD 92.20 billion by 2035, registering a CAGR of 3.75% during the forecast period. Two forces are converging to drive this trajectory: governments worldwide are tightening equipment emissions standards under frameworks like the EU's Industrial Emissions Directive recast, and manufacturers are simultaneously accelerating capital expenditure on automated production lines that demand precision-grade fluids [1]. The result is a market that is rapidly moving beyond bulk commodity sales toward engineered, application-specific formulations.

Legacy mineral-oil-based products still account for the majority of volume, but the technology mix is shifting. Synthetic and semi-synthetic formulations—once reserved for aerospace and high-speed machining—are penetrating mainstream industrial applications as total-cost-of-ownership calculations favor longer drain intervals and reduced downtime. The U.S. Department of Energy estimates that optimized lubrication practices alone can reduce industrial energy consumption by 3–5% across heavy manufacturing facilities, a saving worth roughly USD 7.4 billion annually in the United States [2]. That economic incentive, paired with OEM specifications increasingly mandating synthetic basestocks, is reshaping purchasing behavior across the Industrial Lubricants Market.

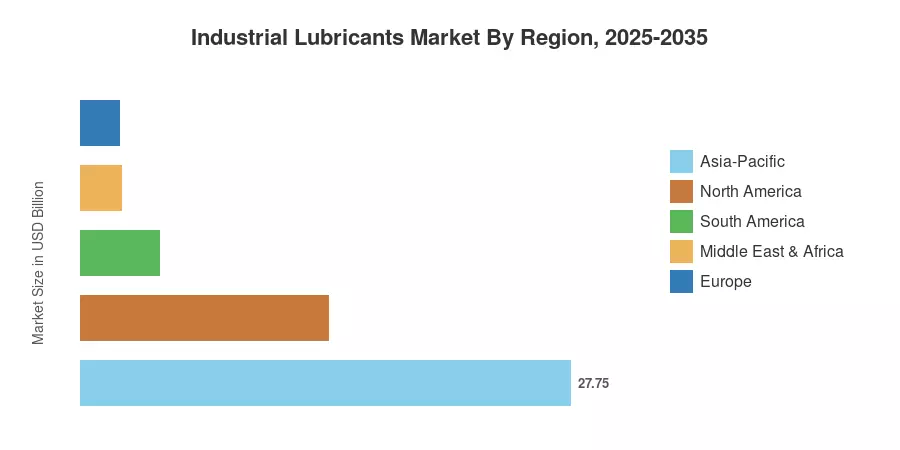

Asia-Pacific dominates global consumption with approximately 43.5% of the Industrial Lubricants Market in 2025, driven by China's integrated refinery-petrochemical expansions and India's accelerating infrastructure build-out. North America holds the second-largest share at around 22.0%, supported by shale-gas-era reindustrialization and strict EPA compliance requirements. Europe captures roughly 20.5%, with demand anchored in Germany's machinery sector and the Nordic region's push toward bio-based chemistries. As Industry 4.0 upgrades proliferate and renewable energy installations scale, the Industrial Lubricants Market stands at the intersection of sustainability mandates and performance engineering.

Key Report Takeaways

• By Product Type

- Engine oil commanded a 25.1% share of the Industrial Lubricants Market in 2025, reflecting its broad application across mobile and stationary power equipment.

- Hydraulic and transmission fluid is forecast to register the fastest segment CAGR of 4.25% through 2035, propelled by growing demand from automated material-handling systems.

- Metalworking fluid accounted for USD 11.80 billion in 2025 as precision machining volumes expanded across automotive and aerospace supply chains.

• By End-User Industry

- Heavy equipment represented 31.2% of the Industrial Lubricants Market in 2025, underpinned by global mining and construction activity.

- Power generation is projected to grow at a 4.62% CAGR through 2035 as wind-turbine installations and gas-fired peaking plants multiply.

- Food and beverage processing contributed USD 6.57 billion in 2025, with food-grade lubricant adoption rising under FSMA and EU Regulation 1935/2004.

• By Region

- Asia-Pacific led the Industrial Lubricants Market with a 43.5% share in 2025 and is also the fastest-growing region at a 3.90% CAGR through 2035.

- North America accounted for USD 14.04 billion in 2025, supported by reindustrialization trends and defense-sector procurement.

- Europe is forecast to expand at a 3.48% CAGR through 2035, driven by decarbonization-linked reformulation mandates.

Industrial Lubricants Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down revenue modeling from base-oil production data, trade-flow analysis, and bottom-up demand estimates derived from installed equipment populations across 42 countries. Historical figures (2021–2024) are validated against customs data and published financial reports from major producers. Forecast figures (2026–2035) apply a calibrated compound growth model adjusted for macro-industrial indicators, regulatory pipeline analysis, and technology substitution curves.