Medical Device Adhesive Market Summary

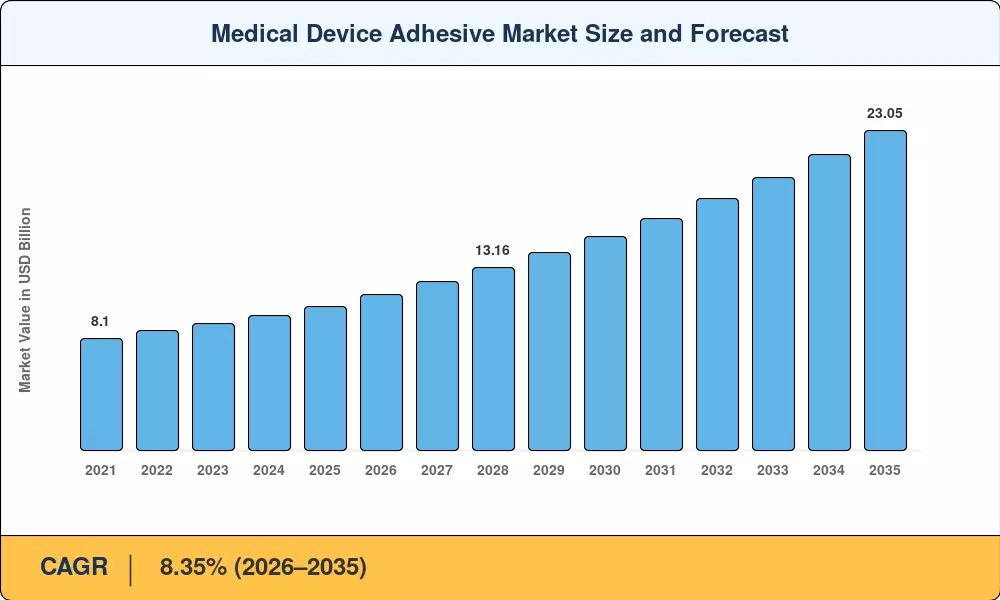

The Global Medical Device Adhesive Market size was valued at USD 10.34 Billion in 2025, and the market is projected to grow from USD 11.21 Billion in 2026 to USD 23.05 Billion by 2035, registering a CAGR of 8.35% during the forecast period 2026–2035. Two catalysts are accelerating this trajectory: mandatory ISO 10993 biocompatibility testing — now enforced across 47 national regulatory bodies — and the rapid shift toward home-based care, which the WHO estimates will account for 35% of chronic-disease management episodes by 2030 [1]. These regulatory and demographic forces are pulling adhesive innovation in directions the medical device adhesive market has not seen in decades.

From a technical perspective, silicone-based chemistries capable of preserving peel strength following 25-kGy radiation sterilization are gradually replacing traditional acrylic systems, although a 15–20% raw material premium [2]. AI-guided optical-curing platforms have reduced bonding cycle times by approximately 25%, reducing production overhead for Class III device assemblers [3]. Meanwhile, water-based formulations continue to gain popularity as European VOC limitations tighten to 50 mg/m3, forcing manufacturers to move towards solvent-free product lines [4].

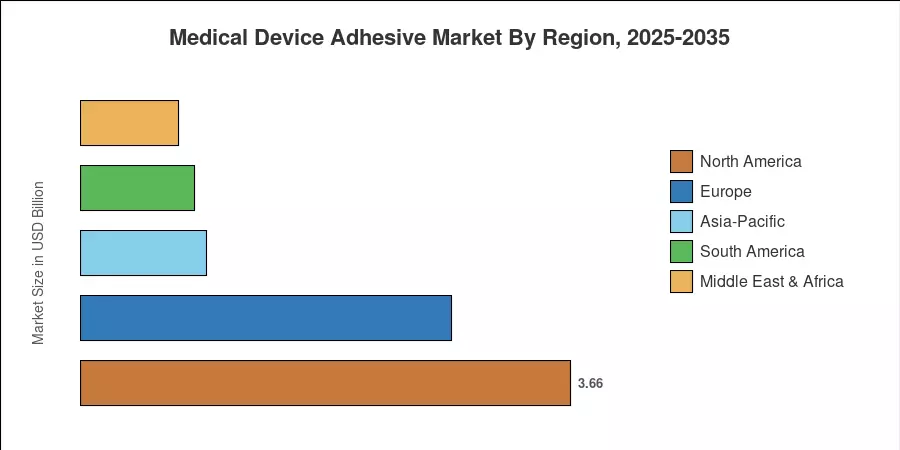

Approximately 35.4% of the medical device adhesive market is attributed to North America due to the presence of major Class III device manufacturing clusters and the fast-tracked 510(k) pathway by the FDA [5]. Asia-Pacific is the fastest expanding market with a projected CAGR of 9.10%, driven by accelerated harmonization with ISO 10993 standards in China and Japan [6]. Europe has the second greatest share at 26.8%, supported by the EU MDR’s strict material traceability requirements. The medical device adhesive industry is entering its most dynamic growth phase in over a decade driven by the proliferation of wearable diagnostics and implantable electronics.

Key Report Takeaways

• By Resin

- Acrylic resins captured 31.0% of the medical device adhesive market in 2025, supported by cost-efficient bonding across disposable diagnostic devices.

- Silicone adhesives are forecast to expand at an 8.75% CAGR through 2035, reflecting sterilization-resilient formulation demand.

• By Technology

- Water-based systems held 37.1% of the medical device adhesive market in 2025, benefiting from tightening VOC regulations across the EU and North America.

- UV/radiation-curable technologies are projected to record the highest segment CAGR at 9.00% during 2026–2035.

• By Adhesive Form

- Pressure-sensitive films and tapes accounted for 39.5% of the market in 2025.

- Gels and hydrocolloid patches are expected to grow at an 8.90% CAGR as chronic-wound home care expands.

• By Application

- Medical devices and equipment represented 46.9% of the medical device adhesive market in 2025.

- Internal medical applications are projected to advance at a 9.20% CAGR through 2035.

• By Geography

- North America contributed 35.4% of global revenue in 2025.

- Asia-Pacific is anticipated to post the fastest regional CAGR of 9.10% during 2026–2035.

Medical Device Adhesive Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from a triangulation of manufacturer revenue disclosures, trade-association shipment data, and validated third-party benchmarks. Forecast projections apply an 8.35% CAGR anchored to confirmed regulatory calendars and device-pipeline visibility through 2035 [1][2].