Military Satellite Market Summary

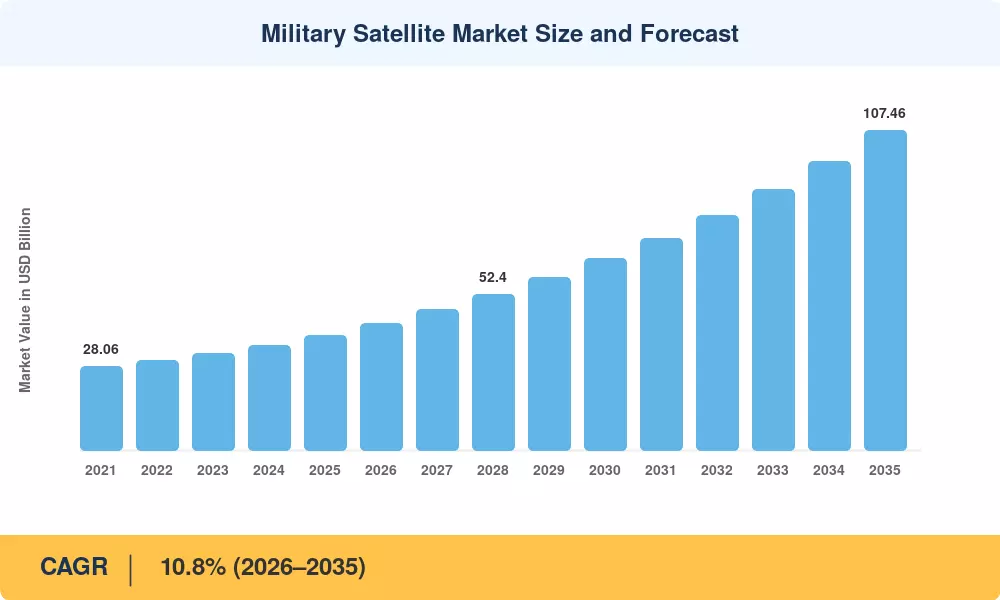

The Military Satellite Market reached an estimated USD 38.52 Billion in 2025 and is projected to grow from USD 42.68 Billion in 2026 to USD 107.46 Billion by 2035, registering a CAGR of 10.8% over the forecast period (2026–2035). This expansion reflects a decisive shift in how nations prioritize orbital assets for defense. Global defense spending crossed USD 2.15 trillion in 2023, and governments from Washington to New Delhi have earmarked unprecedented sums for space-based military infrastructure [1]. The United States Space Force alone requested over USD 30 billion in its FY 2025 budget submission, signaling that the Military Satellite Market sits at the intersection of geopolitics and technology investment [2].

A technology transformation is rewriting the rules of this sector. Legacy geostationary platforms — large, expensive, and slow to deploy — are giving way to proliferated low-Earth-orbit (LEO) constellations that offer resilience through redundancy. The U.S. Space Development Agency's Proliferated Warfighter Space Architecture (PWSA) calls for hundreds of satellites in LEO to create a mesh network resistant to single-point failures [3]. Artificial intelligence now handles onboard image processing, cutting the sensor-to-shooter loop from hours to near-real time. France committed EUR 5.3 billion to its 2024–2030 military space program, while Japan has accelerated its Information Gathering Satellite refresh cycle [4].

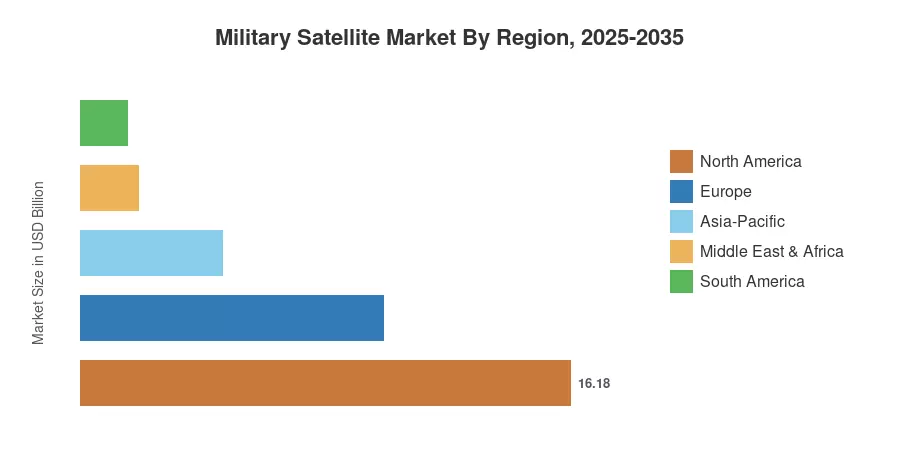

North America dominates the Military Satellite Market with roughly 42% of global revenue, anchored by U.S. Department of Defense procurement. Asia-Pacific is the fastest-growing region, expanding at a CAGR of approximately 12.2%, driven by modernization campaigns in China, India, and South Korea. Europe holds the second-largest share near 26%, underpinned by coordinated EU and NATO space strategies. As orbital congestion intensifies and anti-satellite threats multiply, the Military Satellite Market is poised for sustained double-digit growth through 2035.

Key Report Takeaways

• By Satellite Mass

- The 100–500 kg segment commands a leading share of approximately 34% of the Military Satellite Market, reflecting demand for medium-class reconnaissance and communications platforms.

- The below-10 kg nanosatellite category is expanding at the fastest pace, with defense agencies testing swarm architectures for tactical intelligence.

• By Application

- Communication satellites account for the largest revenue pool in the Military Satellite Market, valued at an estimated USD 14.8 billion in 2025.

- Earth observation platforms are growing rapidly as theater commanders require persistent wide-area surveillance.

• By Region

- North America leads the Military Satellite Market, contributing approximately 42% of total spending in 2025.

- Asia-Pacific is the fastest-growing region, registering a CAGR of 12.2% during the forecast period.

- Europe holds the second-largest regional share, fueled by NATO interoperability mandates and national space programs.

Military Satellite Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from verified defense procurement records, satellite launch manifests, and disclosed program budgets. Forecast projections apply a bottom-up build from segment-level demand models, cross-validated with top-down macroeconomic defense-spending trajectories and orbital launch capacity growth curves.