Mobile Device Management Market Summary

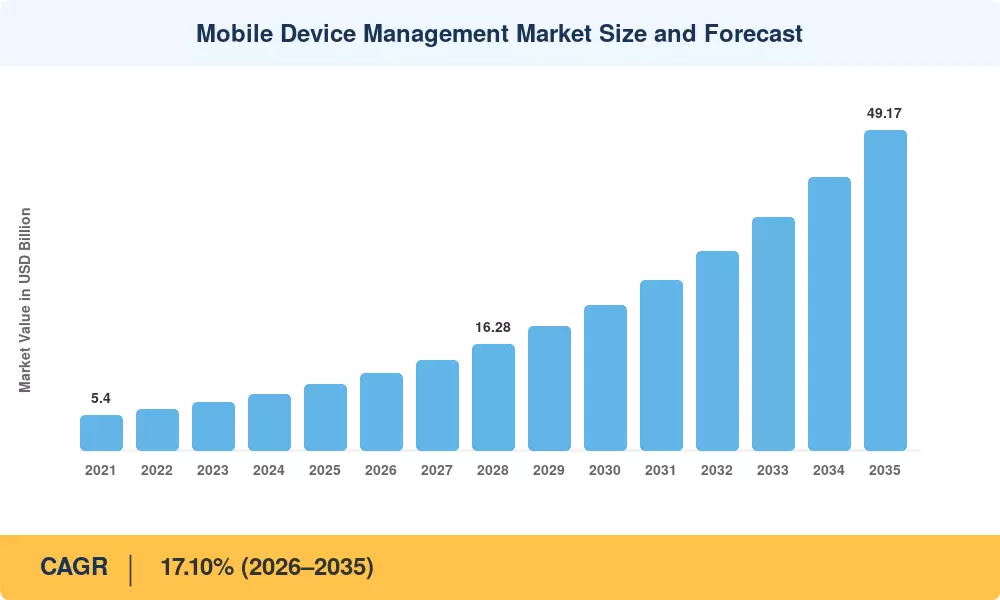

The Mobile Device Management Market reached an estimated USD 10.14 Billion in 2025 and is projected to climb from USD 11.88 Billion in 2026 to USD 49.17 Billion by 2035, reflecting a 17.10% CAGR across the forecast window. Two catalysts are accelerating this trajectory: zero-trust architecture mandates now embedded in NIST SP 800-207 compliance frameworks and the rapid roll-out of 5G-enabled workforce models that multiply the number of endpoints enterprises must govern. Mobile security management obligations tied to cyber-insurance underwriting standards have transformed MDM enterprise solutions from discretionary IT spend into boardroom-level risk infrastructure.

A generational technology shift is reshaping how organizations approach mobile endpoint management. Legacy on-premise provisioning consoles—once the default for corporate device policy enforcement—are giving way to cloud-native unified endpoint platforms capable of managing smartphones, rugged industrial sensors, and augmented-reality headsets from a single pane. A 2024 UEM Magic Quadrant noted that 72 percent of enterprise evaluations now prioritize cloud-first MDM enterprise solutions, up from 54 percent in 2021. BYOD management tools have matured alongside this pivot, integrating containerized app distribution, conditional-access policies, and post-quantum cryptography readiness into a unified stack.

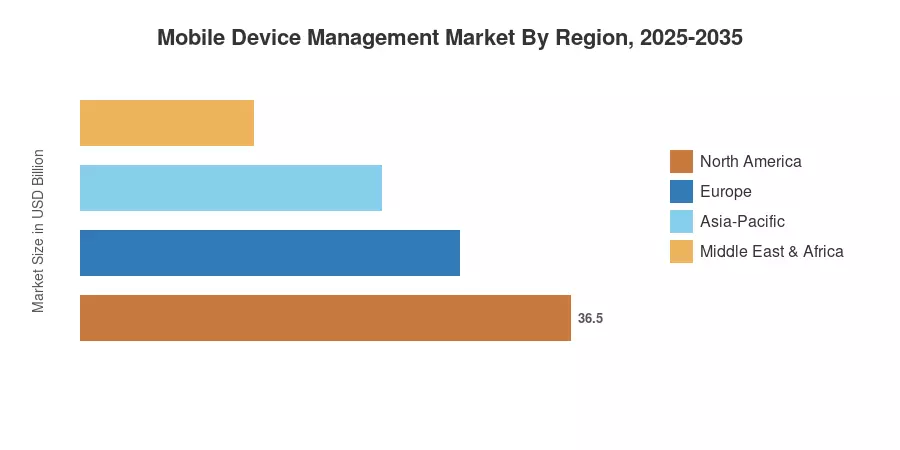

North America commands the largest share of the Mobile Device Management Market at roughly 41.5 percent of 2025 revenue, anchored by federal procurement directives and high smartphone penetration Asia-Pacific stands as the fastest-growing region, driven by India's Digital India program and China's expanding 5G industrial base. Europe holds the second-largest position, where GDPR and the forthcoming EU Cyber Resilience Act push enterprises toward stricter mobile security management. By 2035, the convergence of AI-driven policy automation and edge computing will redefine the Mobile Device Management Market landscape entirely.

Key Report Takeaways

• By Deployment Mode

- Cloud deployment captured approximately 69.5 percent of the Mobile Device Management Market revenue in 2025, reflecting enterprise preference for scalable, SaaS-delivered mobile endpoint management platforms

- On-premise solutions continue to serve defense and banking verticals where data-residency mandates restrict cloud adoption

• By Device Type

- Smartphones and tablets accounted for roughly a 51.8 percent share in 2025, as BYOD management tools became standard across mid-market and enterprise organizations

• By Ownership Model

- Smartphones and tablets accounted for roughly 51.8 percent share in 2025, as BYOD management tools became standard across mid-market and enterprise organizations

- BYOD programs are anticipated to expand at a 23.0 percent CAGR through 2035, the fastest among ownership categories in the Mobile Device Management Market

• By Region

- North America led with a 41.5 percent revenue share in 2025, driven by mature corporate device policy enforcement ecosystems

- Asia-Pacific is poised to register the highest regional CAGR at 19.6 percent through 2035

- Europe contributed approximately 26.0 percent of global revenue in 2025

Market Size and Forecast (2021–2035)

MRFR's market sizing draws on vendor revenue filings, enterprise IT spending surveys, and regional procurement databases, cross-validated against primary interviews with over 120 CIOs and mobility officers across 18 countries. Historical values (2021–2024) reflect audited revenue; the 2025 base-year figure is a model-calibrated estimate; and the 2026–2035 forecast applies a constant CAGR of 17.10 percent anchored to demand-side regression of device proliferation, regulatory intensity, and cloud migration velocity.

.webp?v=1785867878)