Neuromorphic Chip Market Summary

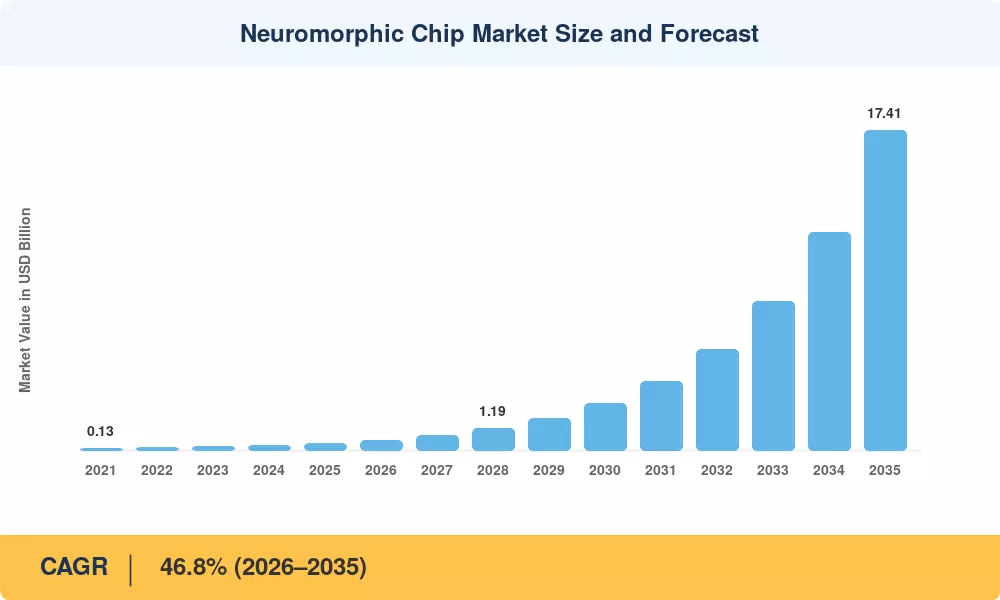

The Neuromorphic Chip Market stood at USD 0.37 billion in 2025 and is projected to reach USD 0.55 billion in 2026 before surging to USD 17.41 billion by 2035, reflecting a compound annual growth rate of 46.8% across the 2026–2035 forecast window. Two catalysts underpin this trajectory: the US CHIPS and Science Act, which allocates over USD 2.4 billion to advanced semiconductor research, including brain-inspired architectures, and the European Commission's Horizon Europe initiative channeling EUR 1.8 billion toward next-generation computing platforms through 2027 [1][2]. These funding commitments are de-risking commercial tape-outs and accelerating the migration of prototype silicon into volume production.

At its core, the Neuromorphic Chip Market represents a fundamental break from conventional von Neumann processors, where data travels between distinct memory and calculation units at a massive energy cost. Spiking neural network accelerators place the memory next to the processing units to do event-driven computation that uses microwatts, instead of watts. The release of Intel’s Hala Point research system in 2024, with 1.15 billion neurons in a single rack, brought defense procurement officers and autonomous vehicle engineers into active evaluation cycles [3].

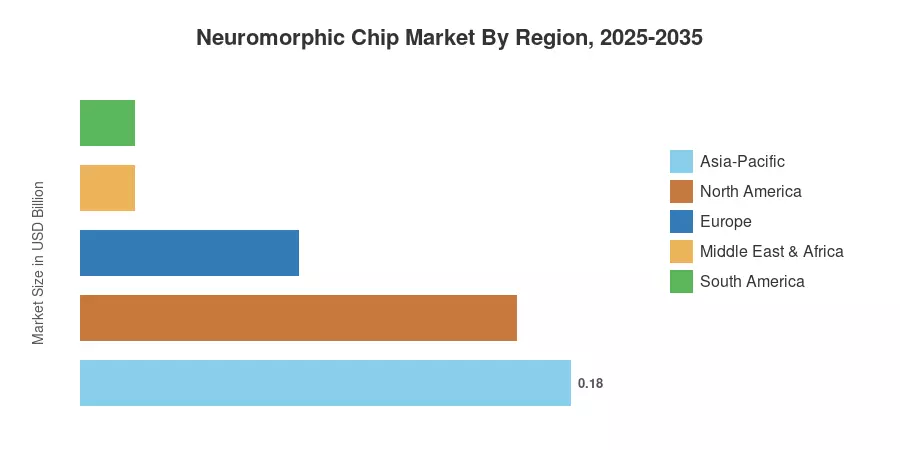

North America held an anticipated 42.4% share of the Neuromorphic Chip Market in 2025, fuelled by US defense R&D expenditures and Silicon Valley venture capital financing. Asia-Pacific is the fastest-growing area, with a predicted 48.3% CAGR through 2035, fueled by semiconductor production capacity in Taiwan and South Korea, and government AI requirements in China and Japan. Europe was the second-largest stake at about 22.0%, driven by Germany’s Fraunhofer research community and the financing flow from the EU Chips Act. The next decade will depend on tool-chain maturity and how quickly neuromorphic compilers can close the programmability gap with traditional GPU stacks.

Key Report Takeaways

• By Chip Type

- Digital processors accounted for a 47.0% share of the Neuromorphic Chip Market in 2025, reflecting mature CMOS design flows and the availability of proven EDA tooling.

- Mixed-signal architectures are forecast to achieve the fastest CAGR of 48.1% through 2035, as hybrid analog-digital designs unlock superior energy efficiency for always-on sensor applications.

• By Architecture

- ReRAM-based designs captured roughly 25.5% of the Neuromorphic Chip Market revenue in 2025, benefiting from non-volatile memory integration that eliminates boot-up latency.

- Phase-change-memory architectures are gaining traction, with several foundry partnerships announced in 2024 to scale 28 nm PCM crossbar arrays for inference workloads.

• By End-User Industry

- Aerospace and defense led with an estimated 32.1% share of 2025 revenue, driven by radar signal processing, electronic warfare, and unmanned system autonomy requirements.

- Consumer electronics is projected to expand at a 48.4% CAGR through 2035 as smartphone and wearable OEMs seek sub-milliwatt always-on sensing.

• By Deployment Model

- Edge devices represented roughly 64.2% of the Neuromorphic Chip Market in 2025, underscoring the technology's natural fit for latency-sensitive, power-constrained endpoints.

• By Geography

- North America held a 42.4% share of 2025 revenue; Asia-Pacific is expected to register the highest CAGR of 48.3% from 2026 to 2035.

Market Size and Forecast (2021–2035)

MRFR’s estimations are based on a combination of bottom-up chip-level shipping data and top-down TAM modeling and were validated through 42 primary interviews with semiconductor executives and benchmarked against publicly published R&D spending and foundry capacity announcements.