Next-Generation Firewall Market Summary

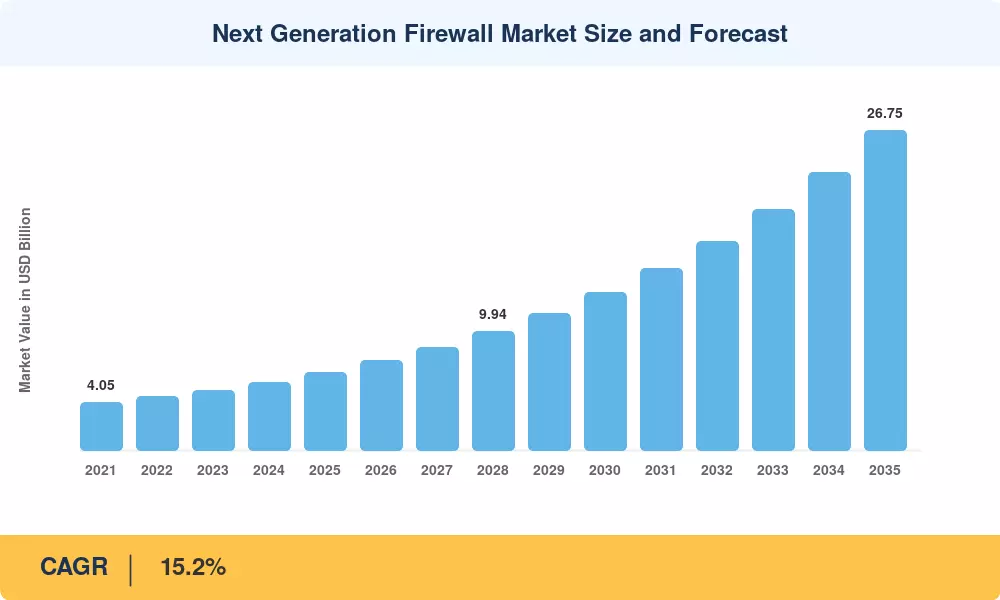

The Next-Generation Firewall Market stood at USD 6.50 billion in 2025 and is forecast to climb to USD 26.75 billion by 2035, registering a 15.2% CAGR across the 2026–2035 forecast period. Two forces are converging to accelerate spending: executive-level mandates tied to U.S. Executive Order 14028 on zero-trust adoption, and the European Union's NIS2 Directive—both compelling organizations to replace perimeter-only defenses with identity- and application-aware enforcement planes [1][2]. The result is a procurement wave that reaches well beyond traditional IT shops into operational-technology environments, healthcare networks, and sovereign-cloud programs.

Legacy stateful-inspection firewalls are giving way to platforms that unify application-aware traffic analysis, encrypted-session inspection, and real-time threat intelligence feeds on a single chassis or virtual instance. Fortinet's 2024 launch of custom ASIC-powered appliances capable of 400 Gbps threat throughput illustrates the performance benchmarks that enterprise buyers now demand [3]. Cloud-native form factors are gaining ground rapidly, with hyperscaler marketplaces hosting virtual firewall images that spin up alongside workloads in seconds rather than weeks.

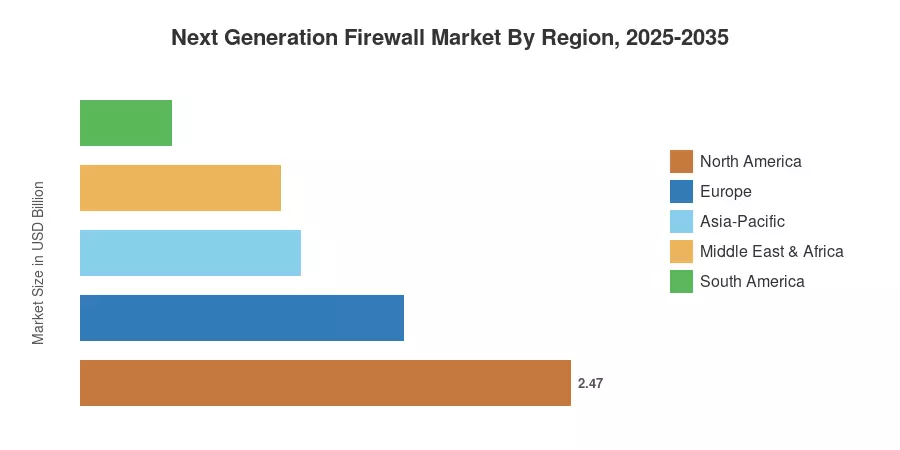

North America commands roughly 38% of global revenue in the Next-Generation Firewall Market, driven by dense cloud adoption and strict federal cybersecurity frameworks. Asia-Pacific is the fastest-growing region at a 17.1% CAGR, propelled by sovereign-cloud mandates in India, Japan, and ASEAN nations. Europe holds the second-largest share, anchored by NIS2 compliance spending and cross-border data-residency requirements. The decade ahead will reward vendors that combine hardware-level throughput, AI-driven detection, and unified multi-cloud policy orchestration.

Key Report Takeaways

• By Solution Type

- Hardware appliances accounted for roughly 58% of Next-Generation Firewall Market revenue in 2025, reflecting continued demand for dedicated throughput in data-center perimeters.

- Virtual and cloud-based firewall deployments are on track to grow at a 16.2% CAGR through 2035 as enterprises shift workloads to hybrid environments.

• By Enterprise Size

- Large enterprises represented approximately 74% of total spending in 2025, driven by complex multi-site architectures.

- SMEs are projected to expand at a 17.2% CAGR, fueled by managed-security-service offerings that lower the entry barrier.

• By End-User Industry

- IT and Telecom captured about 48% of the Next-Generation Firewall Market in 2025, reflecting dense traffic volumes and carrier-grade inspection needs.

- BFSI is the fastest-growing vertical, registering a 16.8% CAGR as real-time fraud prevention and regulatory audits intensify.

• By Region

- North America led with 38% of global revenue in 2025, with U.S. federal procurement cycles setting the pace.

- Asia-Pacific is anticipated to post the highest regional CAGR of 17.1% through 2035, underpinned by data-localization mandates.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up vendor-revenue aggregation with top-down demand-side modeling. Historical figures (2021–2024) are anchored to audited financial disclosures and channel-shipment data; forecast figures (2026–2035) layer macroeconomic indicators, enterprise IT-spending benchmarks from, and regulatory-impact assessments.