Firewall as a Service Market Summary

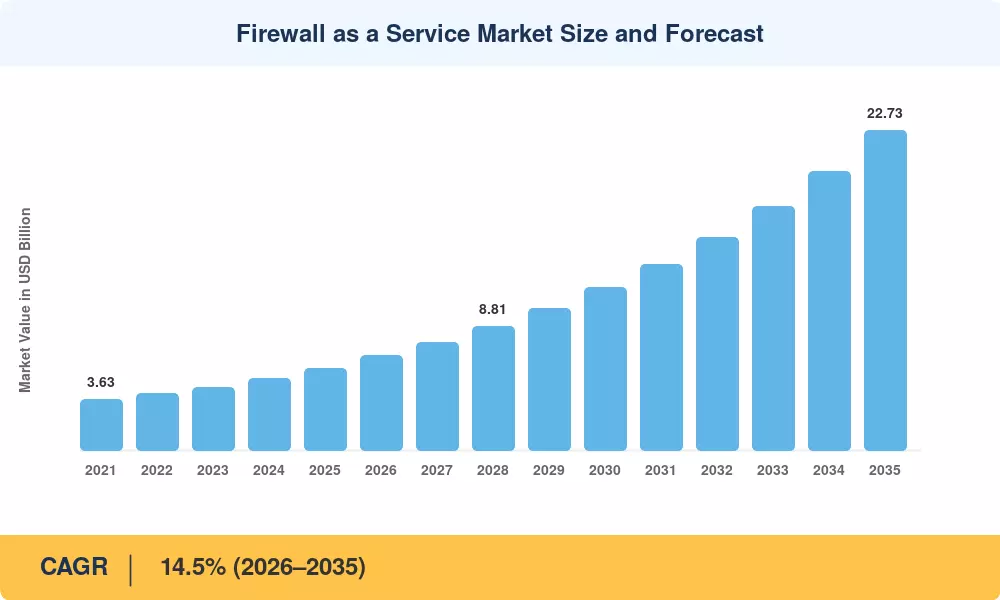

The Firewall as a Service Market was valued at USD 5.81 Billion in 2025, with the forecast period beginning at USD 6.72 Billion in 2026 and climbing to USD 22.73 Billion by 2035 at a compound annual growth rate of 14.5% [1]. Two structural forces anchor this trajectory: the federal zero-trust architecture mandate codified in Executive Order 14028, which requires all U.S. civilian agencies to adopt identity-verified, perimeter-less security frameworks, and the EU's NIS2 Directive that imposes breach-notification and risk-management obligations on critical-infrastructure operators across 27 member states [2]. Together, these policy instruments channel billions in compliance-driven spending directly into cloud-delivered firewall procurement.

Legacy appliance-based perimeters are giving way to software-defined, API-orchestrated inspection engines distributed across global points of presence. A recent source estimates that by 2027, over 65% of enterprise firewall spend will shift to cloud-delivered models, up from roughly 30% in 2023 [3]. Persistent chip-supply bottlenecks and multi-year lead times for high-throughput ASIC-based appliances are accelerating this transition, pushing procurement teams toward subscription-based delivery that decouples security capacity from hardware procurement cycles.

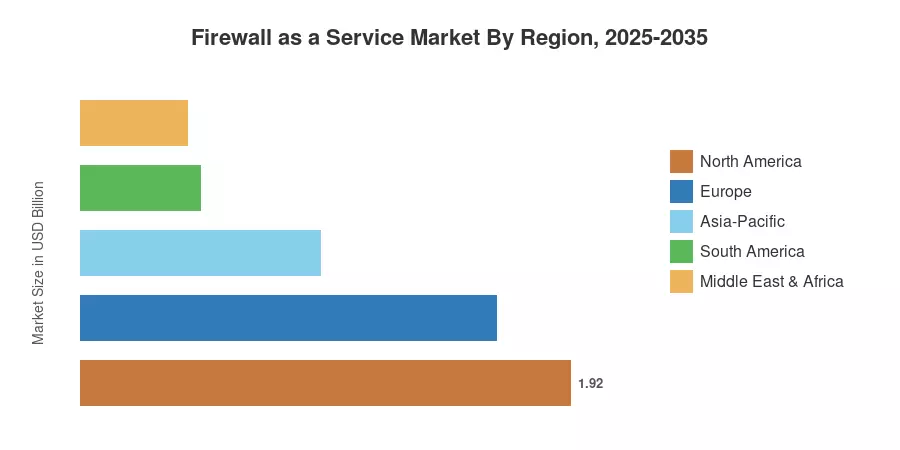

North America held approximately 33% of the Firewall as a Service Market in 2025, anchored by hyperscaler density and early zero-trust adoption. Asia-Pacific is the fastest-growing region at a projected 16.2% CAGR through 2035, propelled by digital-infrastructure investment programs across India, China, and ASEAN economies. Europe claimed the second-largest share at roughly 28%, driven by regulatory harmonization under NIS2 and GDPR enforcement intensity [4]. As SASE convergence deepens, the Firewall as a Service Market is poised to absorb adjacent spend from standalone VPN, CASB, and SWG categories over the coming decade.

Key Report Takeaways

• By Service Model

- Software-as-a-Service captured approximately 43% revenue share of the Firewall as a Service Market in 2025, reflecting enterprise preference for opex-friendly consumption.

- Platform-as-a-Service is advancing at a 15.5% CAGR through 2035 as vendors expand developer-facing policy-as-code capabilities.

• By Deployment Model

- Public cloud accounted for about 53% of the Firewall as a Service Market in 2025, driven by workload migration to AWS, Azure, and GCP environments.

- Hybrid cloud deployment is growing at a 15.3% CAGR, reflecting regulated-industry requirements for on-premises data residency paired with cloud inspection.

• By Enterprise Size

- Large enterprises represented approximately 61% of the Firewall as a Service Market in 2025.

- SMEs are expanding at a 15.1% CAGR as vendors introduce simplified, self-service tiers targeting mid-market buyers.

• By Industry Vertical

- BFSI captured roughly a 25.5% share of the Firewall as a Service Market in 2025.

- Healthcare is forecast to register a 16.0% CAGR, accelerated by telehealth expansion and HIPAA modernization requirements.

• By Security Type

- Next-generation firewall solutions controlled approximately 38% of the Firewall as a Service Market in 2025.

- Distributed firewalls are expanding at a 15.7% CAGR as micro-segmentation demand intensifies across containerized environments.

• By Region

- North America contributed about 33% of global Firewall as a Service Market revenue in 2025.

- Asia-Pacific is expected to grow at a 16.2% CAGR between 2026 and 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a bottom-up revenue model that aggregates vendor-reported subscription, licensing, and professional-services revenue across all tracked segments. Historical figures (2021–2024) are validated against SEC filings, annual reports, and cross-checked with IT spend benchmarks. Forecast projections (2026–2035) apply segment-weighted growth assumptions calibrated to policy timelines, technology adoption curves, and macroeconomic scenarios.