Nutraceutical Excipients Market Summary

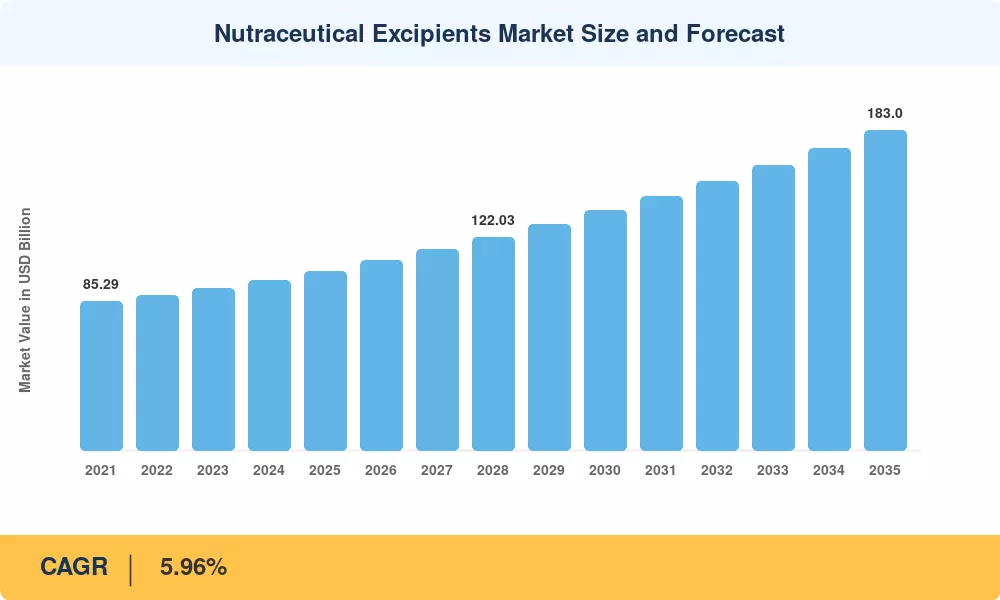

The Nutraceutical Excipients Market size was valued at USD 102.58 Billion in 2025, and the market is projected to grow from USD 108.69 Billion in 2026 to USD 183.00 Billion by 2035, registering a CAGR of 5.96% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the global pivot toward preventive nutrition — now a stated policy priority in the EU Farm to Fork Strategy and China's 14th Five-Year Health Plan — and consumer willingness to pay premium prices for products that deliver clinically validated health outcomes. The Nutraceutical Excipients Market benefits from aging demographics worldwide, with the WHO projecting that adults aged 60-plus will double to 2.1 billion by 2050, sharply increasing demand for supplement formulations [1].

A technology transformation is reshaping how ingredients reach consumers. Legacy bulk-powder blending operations are giving way to precision encapsulation platforms and clean-label extraction systems that preserve bioactive potency. Investment in these next-generation processing lines exceeded USD 4.8 billion globally in 2024, according to industry consortium estimates [2]. Regulatory frameworks such as the U.S. FDA's New Dietary Ingredient notification pathway and the EU Novel Food Regulation (EC 2015/2283) are accelerating this shift by demanding higher evidence standards for health claims [3].

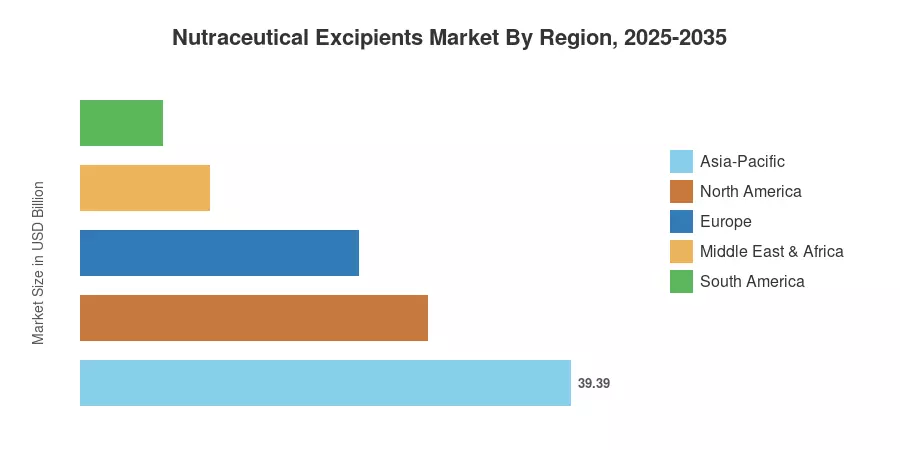

Asia-Pacific commands roughly 38.4% of the Nutraceutical Excipients Market, driven by China's and India's massive population bases and rising disposable incomes. The Middle East & Africa region is the fastest-growing region, expanding at an estimated 10.1% CAGR, fueled by Gulf-state investments in food security and nutraceutical manufacturing zones. North America holds the second-largest position at approximately 27.2% share, anchored by a mature dietary supplement culture and robust clinical research infrastructure. The decade ahead will be defined by how quickly smaller producers adopt advanced formulation technologies to meet escalating regulatory and consumer demands.

Key Report Takeaways

• By Product Type

- Probiotics captured a leading 31.2% share of the Nutraceutical Excipients Market in 2025, reflecting strong consumer interest in gut-health solutions across all age groups.

- Omega-3 ingredients are expected to expand at an 8.4% CAGR through 2035, underpinned by cardiovascular and cognitive health claims gaining clinical backing.

- Vitamins accounted for USD 18.72 billion in 2025, supported by post-pandemic immunity-focused purchasing behavior.

• By Form

- Powder formats represented 62.4% of the Nutraceutical Excipients Market in 2025, preferred for shelf stability and dosing flexibility.

- Liquid forms are projected to grow at a 7.6% CAGR to 2035, driven by ready-to-drink nutraceutical beverages gaining retail shelf space.

• By Application

- Dietary supplements held a 37.9% share of the Nutraceutical Excipients Market in 2025.

- Functional beverages are forecast to register a 10.2% CAGR between 2026 and 2035, the fastest among application segments.

• By Region

- Asia-Pacific led with a 38.4% revenue share in 2025, with China and India together generating more than half of regional demand.

- The Middle East & Africa region is projected to post the fastest CAGR of 10.1% through 2035.

Nutraceutical Excipients Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates proprietary primary interviews with over 200 industry stakeholders, cross-validated against trade data from Euromonitor, FAO, and national regulatory filings. Historical figures (2021–2024) reflect audited company revenues and import-export statistics; forecast values (2026–2035) are derived using bottom-up segment aggregation and top-down macroeconomic calibration.