Oats Market Summary

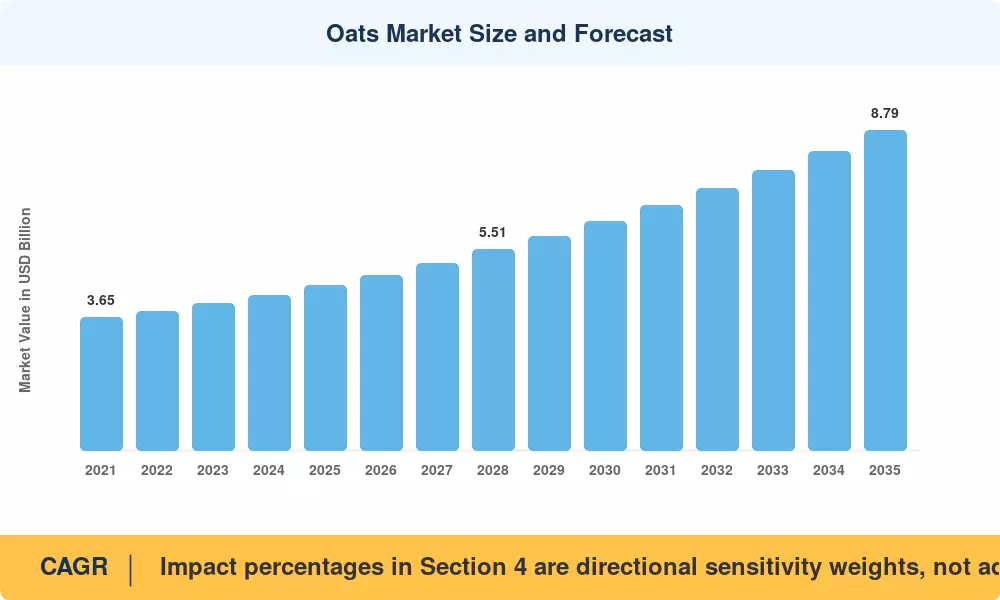

The global Oats Market stood at USD 4.53 billion in 2025 and is projected to reach USD 4.82 billion in 2026 before climbing to USD 8.79 billion by 2035, registering a CAGR of 6.9% during the 2026–2035 forecast period. This trajectory reflects a fundamental shift in consumer preferences toward whole-grain, nutrient-dense foods. Regulatory clarity from the U.S. FDA on the ≤ 20 ppm gluten threshold for food labeling has given manufacturers confidence to develop certified products for celiac and gluten-sensitive consumers, directly expanding the addressable Oats Market.

Processing innovation is reshaping how oats reach consumers. Traditional milling operations are giving way to advanced hydrothermal and enzyme-assisted processing lines that extend shelf life by up to 40% while preserving beta-glucan content and sensory properties [2]. The European Commission allocated EUR 120 million under Horizon Europe for sustainable cereal processing research in 2024, accelerating commercial adoption of these techniques across the continent [3].

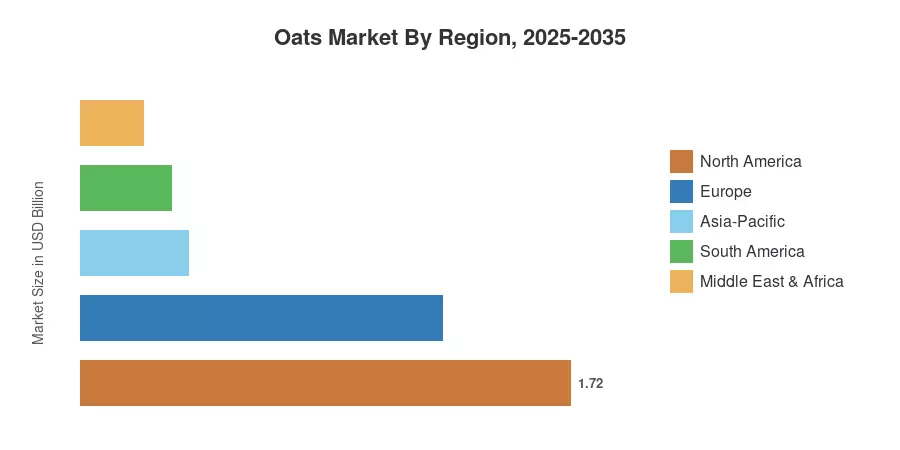

North America commands the largest share of the Oats Market at roughly 38% of global revenue, anchored by entrenched breakfast cereal habits across the United States and Canada. Asia-Pacific is the fastest-growing region, expanding at a CAGR exceeding 8.4%, fueled by rising health awareness among urban middle-class households in China and India. Europe holds the second-largest share at approximately 28%, supported by strong private-label oat product lines in Germany, the UK, and the Nordic countries. As online grocery platforms reduce entry barriers for emerging brands, the decade ahead promises intensifying competition and broader product diversification.

Key Report Takeaways

• By Product Type

- Rolled oats captured 37.3% of the oats market revenue in 2025, reflecting their dominance across breakfast and snacking occasions.

- Oat flour is on track for the fastest segment CAGR of 9.9% through 2035, driven by rising demand from bakery and plant-based food formulators.

• By Category

- Processed oats accounted for 76.1% of Oats Market value in 2025, underscoring consumer preference for convenience-ready formats.

• By Nature

- Organic variants are expanding at a 4.8% CAGR, attracting premium-oriented shoppers in North America and Europe.

• By Region

- North America led global revenue with a 38% share, while Asia-Pacific emerged as the fastest-growing region at 8.4% CAGR.

- Europe held the second-largest share at 28%, with Germany and the UK serving as primary consumption hubs.

Oats Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining top-down revenue analysis from trade databases (FAO, USDA), bottom-up production and pricing models from key exporting nations, and demand-side validation through proprietary consumer surveys across 22 countries[4].

.webp?v=1783951754)