Palm Oil Market Summary

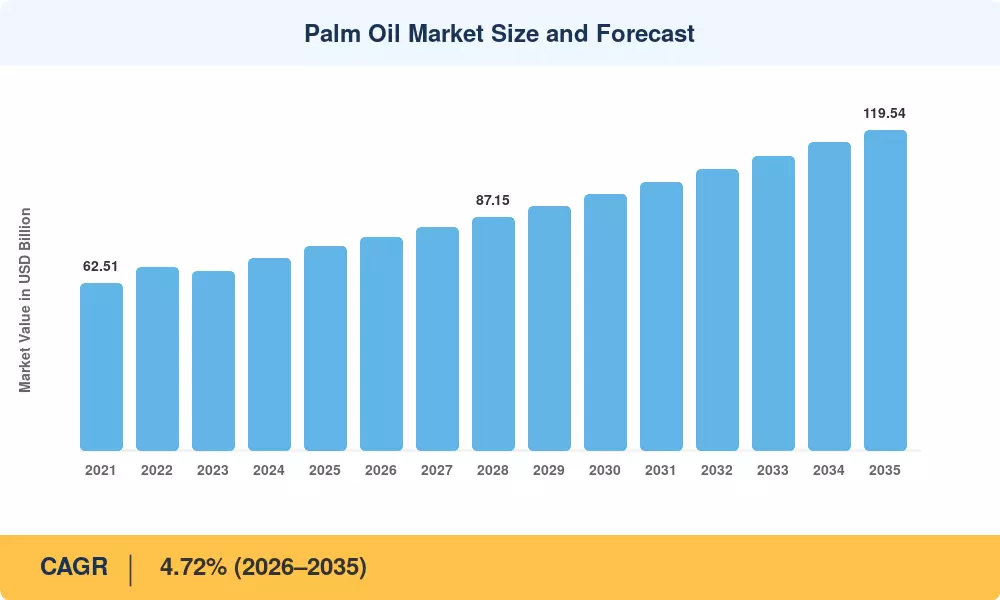

The Palm Oil Market was valued at USD 76.18 billion in 2025 and is projected to reach USD 79.46 billion in 2026 before climbing to USD 119.54 billion by 2035, advancing at a CAGR of 4.72% during the 2026–2035 forecast window. This trajectory reflects the commodity's deep integration into global food systems, personal care manufacturing, and the fast-expanding oleochemical sector. Government-backed biodiesel blending mandates across Southeast Asia — Indonesia's B40 program alone absorbs over 11 million metric tons of crude palm oil annually [2] — continue to underpin demand volumes that few alternative vegetable oils can match.

Sustainable palm oil production is reshaping the industry's operational DNA. Legacy plantation practices centered on slash-and-burn land clearing are giving way to precision-agriculture models that deploy satellite monitoring, drone-based canopy analysis, and IoT-enabled soil sensors. The Roundtable on Sustainable Palm Oil (RSPO) has certified over 4.8 million hectares globally, with RSPO-certified palm oil now commanding a 7–12% price premium over conventional grades [3]. Major FMCG buyers have pledged full traceability by 2030, channeling an estimated USD 2.4 billion in supply-chain digitization investments through 2028 [4].

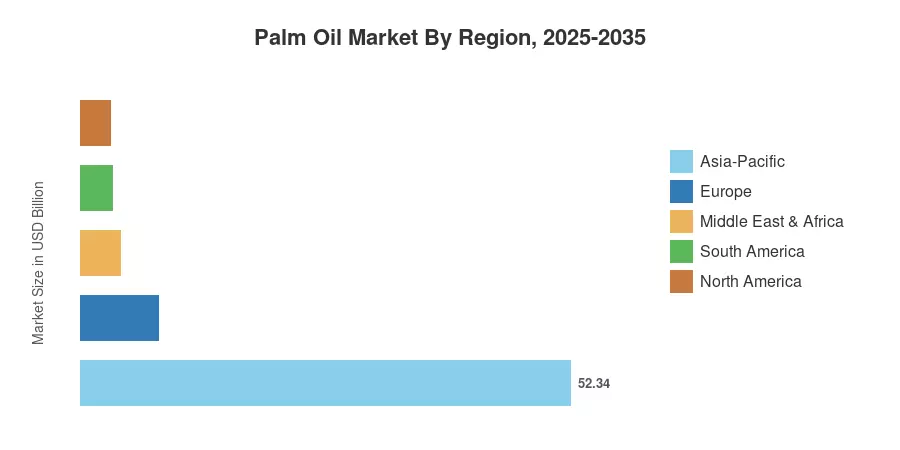

Asia-Pacific dominates the Palm Oil Market with roughly 68.7% of global revenue, anchored by Indonesia and Malaysia's combined output of over 85% of the world's supply. The Middle East & Africa region stands as the fastest-growing geography, posting a projected CAGR of 5.64% through 2035, driven by population growth and rising edible-oil consumption in Sub-Saharan Africa Europe represents the second-largest import bloc, though regulatory headwinds from the EU Deforestation Regulation will increasingly shape trade flows over the coming decade.

Key Report Takeaways

• By Product Type

- RBD palm oil captured a leading 42.3% revenue share of the Palm Oil Market in 2025, reflecting its dominance in frying, bakery, and confectionery applications

- Palm kernel extraction volumes are forecast to grow at a CAGR of 5.93% through 2035, propelled by rising demand for lauric-acid derivatives in cosmetics and surfactants

- Crude palm oil refining capacity expansions across Indonesia and India accounted for over USD 1.8 billion in capital expenditure commitments during 2023–2025

• By Nature

- Conventional palm oil held 84.6% of the Palm Oil Market in 2025, though tightening deforestation regulations are gradually eroding its share

- Organic-certified output is advancing at a 6.37% CAGR through 2035, the fastest pace within the nature segmentation

• By End Use

- Retail channels represented 51.4% of the Palm Oil Market demand in 2025

- Industrial end-use segments are expanding at a 7.08% CAGR through 2035 as oleochemical and biofuel applications scale

• By Region

- Asia-Pacific commanded approximately USD 52.34 billion of the Palm Oil Market in 2025

- The Middle East & Africa region will register the highest CAGR at 5.64% through 2035

Market Size and Forecast (2021–2035)

MARKET RESEARCH FUTURE (MRFR)'s market sizing integrates primary interviews with plantation operators, refiners, and commodity traders alongside secondary data from FAO, USDA, and national palm oil boards. Base-year (2025) revenue is triangulated using import-export volumes, average CPO benchmark pricing, and downstream value-addition estimates.

.webp?v=1783951509)