Parking Management Market Summary

The Parking Management Market reached an estimated USD 6.01 billion in 2025 and is set to open the forecast window at roughly USD 6.59 billion in 2026, climbing to USD 15.16 billion by 2035 at a 9.7% CAGR. Two catalysts anchor this trajectory: municipal curb-digitization mandates spreading across North American and European cities, and a wave of national smart-city funding programs in Asia-Pacific that bundle parking sensors into broader mobility budgets. Cities that once treated parking as a static asset are now budgeting for it as a recurring data stream.

Legacy ticket-and-gate infrastructure is being replaced by cloud-native platforms that use license-plate recognition in conjunction with dynamic pricing algorithms. Several transportation agencies have committed nine-figure investments in curb-management overhauls, part of a broader shift away from one-off hardware purchases to subscription-based software and managed services. Networks of cameras and sensors that once merely counted automobiles now feed occupancy data into traffic-management and emissions-reporting systems.

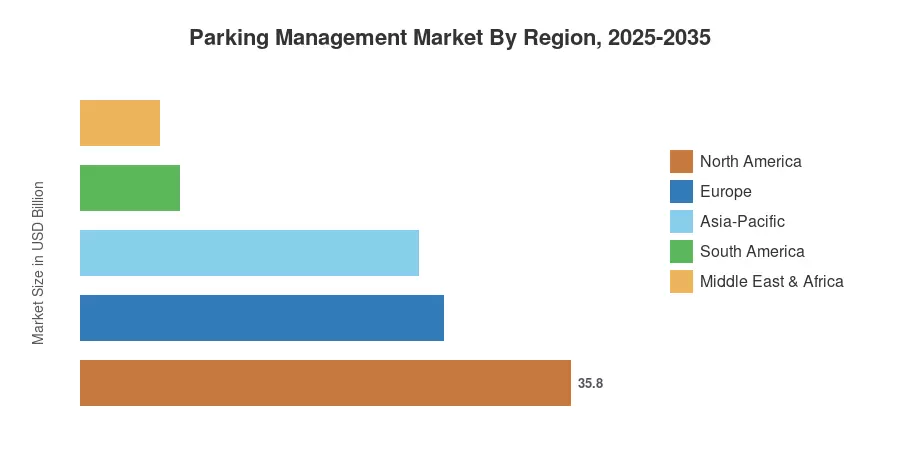

North America continues to be the largest area for the Parking Management Market and will generate revenue of around 35.8% by 2025, owing to the dense urban deployments and airport upgrade plans. Asia-Pacific is the fastest growing region, growing at an estimated 10.6% CAGR as Chinese and Indian cities digitize their inventory at scale. Sustainability standards related to low emission zones make Europe the second largest position. The next decade will favour operators who can turn parking infrastructure into a software-defined asset.

Key Report Takeaways

• By Technology

- Camera and license-plate-recognition systems held an estimated 39.5% share of the Parking Management Market in 2025, anchoring most municipal deployments.

- Mobile-app and Bluetooth-based solutions are forecast to expand at a 10.7% CAGR through 2035 as contactless payment habits solidify.

- Sensor-based single-space detection continues to underpin off-street facility upgrades across mature markets.

• By Sector

- Municipal and government operators accounted for an estimated 33.8% share of Parking Management Market revenue in 2025.

- Commercial off-street operators, including malls and mixed-use developments, are scaling fastest in secondary cities.

- Transit and airport operators are projected to grow at a 10.4% CAGR as terminal expansions bundle in digital parking.

• By Geography

- North America commanded an estimated 35.8% share of the Parking Management Market in 2025.

- Asia-Pacific is advancing at a 10.6% CAGR through 2035, the fastest of any region tracked.

- Europe's growth is increasingly tied to low-emission-zone enforcement budgets rather than new construction.

Market Size and Forecast (2021–2035)

Figures below aggregate triangulated procurement data from municipal tenders, vendor shipment estimates and operator revenue declarations. Historical years show a gradual recovery from pre-pandemic levels, while the forecast timeframe shows an acceleration of cloud-platform usage from 2026 onwards.