Smart Transportation Market Summary

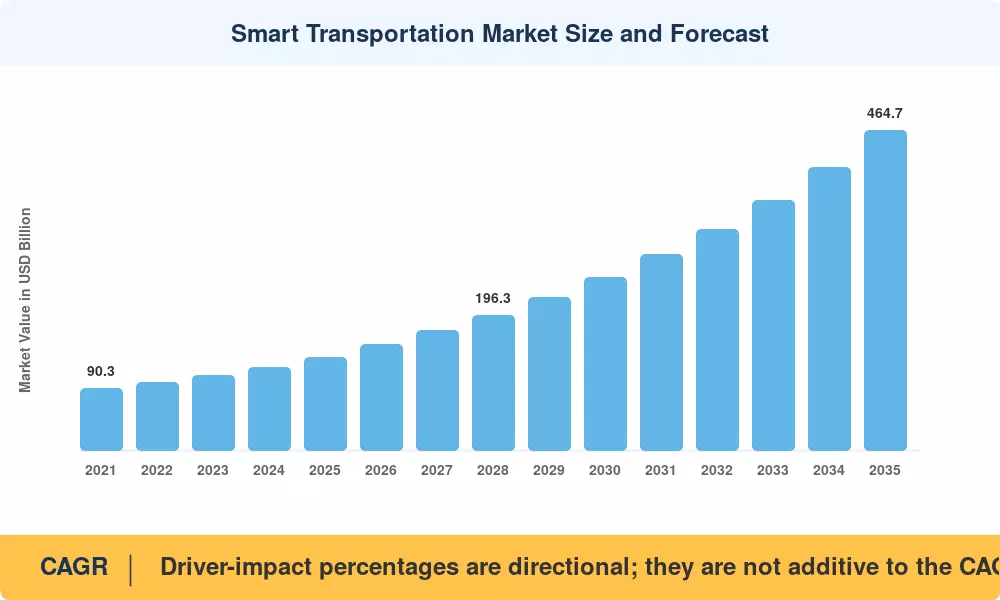

The Smart Transportation Market reached an estimated USD 134.50 billion in 2025 and is projected to grow from USD 153.50 billion in 2026 to USD 464.70 billion by 2035, registering a CAGR of 13.10% across the forecast window. This expansion is anchored in aggressive public-sector capital commitments — the United States alone approved more than USD 4.5 billion for next-generation mobility projects in late 2024, while the European Union's Sustainable and Smart Mobility Strategy is channeling billions into zero-emission corridors and open-data mandates across all transport modes [1][2]. These policy catalysts are converting pilot-stage technology into system-wide deployments at an unprecedented pace.

Legacy traffic control hardware — loop detectors, fixed-timing signals, and siloed fare-collection platforms — is giving way to cloud-native analytics, 5G-enabled vehicle connectivity, and digital-twin modeling that can simulate entire metropolitan corridors before a single sensor is installed. The Smart Transportation Market is absorbing this technology shift as cities discover that data-centric traffic systems deliver measurably more capacity without additional lane construction [3]. Cooperative vehicle systems and AI-driven signal optimization are moving from research papers to production intersections.

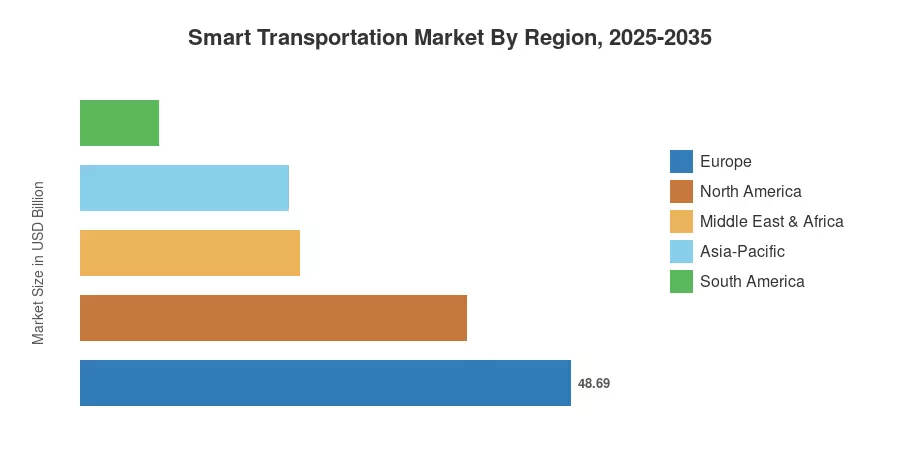

Europe commands approximately 36.20% of the Smart Transportation Market, backed by regulatory harmonization and a continent-wide C-ITS deployment roadmap. Asia-Pacific is the fastest-growing region, propelled by megacity-scale intelligent highway and connected vehicle infrastructure programs in China, India, and Southeast Asia. North America holds the second-largest share at roughly 28.50%, driven by federal grant cycles and private-sector autonomy pilots. Over the coming decade, convergence of electrification, autonomy, and platform economics will redefine how people and freight move through urban and intercity networks.

Key Report Takeaways

• By Application & Product Type

- Traffic management accounted for an estimated 34.50% of the Smart Transportation Market in 2025, underpinned by municipal demand for adaptive signal control and real-time congestion analytics.

- Advanced transportation management systems (ATMS) commanded roughly 28.90% of the Smart Transportation Market in 2025, reflecting widespread replacement of legacy fixed-timing infrastructure.

- Cooperative vehicle systems are expanding at a 18.10% CAGR through 2035 as V2X mandates gain traction across North America and Europe.

• By Service & Connectivity

- Cloud services captured approximately 44.20% share in 2025, driven by municipal preference for scalable, subscription-based traffic platforms.

- Cellular and C-V2X connectivity technology held around 54.50% of the Smart Transportation Market in 2025.

• By Region

- Europe led the Smart Transportation Market with 36.20% revenue share in 2025, anchored in EU regulatory mandates.

- Asia-Pacific is the fastest-growing region, forecast to expand at a 15.40% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates primary interviews with transport-agency procurement officers, OEM revenue disclosures, government budget allocations, and bottom-up technology-adoption curves validated against secondary databases. Historical figures (2021–2024) are actuals; 2025 is the calibrated base year; and 2026–2035 projections apply a constant 13.10% CAGR adjusted for anticipated policy and technology inflections.