Patient Monitoring Devices Market Summary

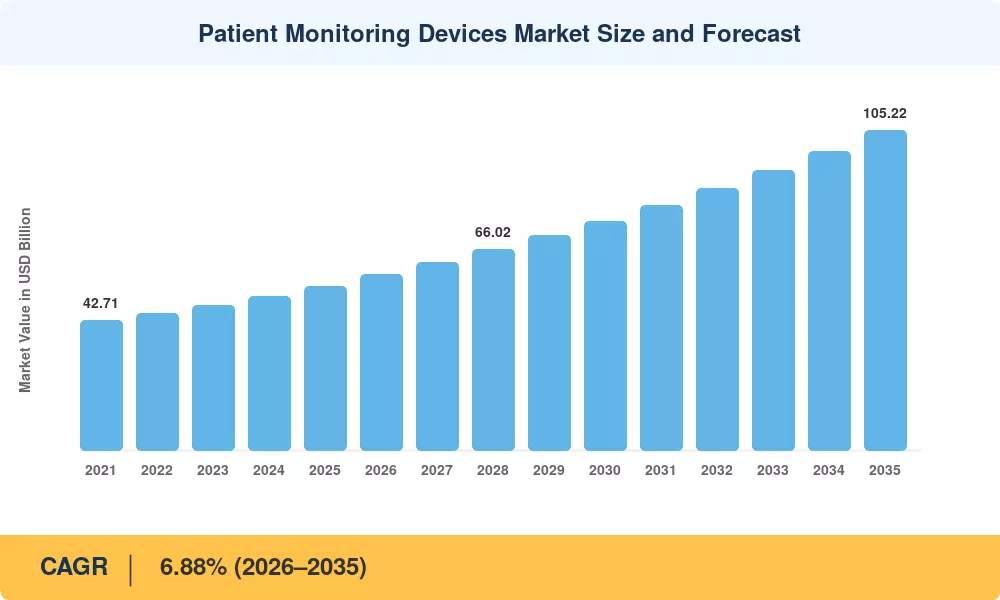

The Patient Monitoring Devices Market size was valued at USD 54.07 Billion in 2025, and the market is projected to grow from USD 57.79 Billion in 2026 to USD 105.22 Billion by 2035, registering a CAGR of 6.88% during the forecast period 2026–2035. Two policy catalysts anchor this trajectory: CMS's expanded reimbursement codes for remote therapeutic monitoring (RPM codes 98975–98981), which unlocked approximately USD 2.1 billion in new billable services since 2022 [1], and the EU Medical Device Regulation (MDR 2017/745) transition deadline, which compelled device manufacturers to invest heavily in post-market surveillance infrastructure [2]. These regulatory tailwinds continue to reshape how clinical data flows between care settings.

A generational technology transition is displacing legacy freestanding displays. Proprietary bedside units that required human charting are being replaced by cloud-connected platforms that can transmit physiological data via disposable biosensor patches, edge-computing hubs and smartphone-paired wearables. From 2021 to 2024, the FDA’s Digital Health Center of Excellence approved over 200 AI-enabled monitoring algorithms [3]. In 2024, global hospital IT capital investment on linked monitoring infrastructure alone exceeded USD 8.4 billion [4].

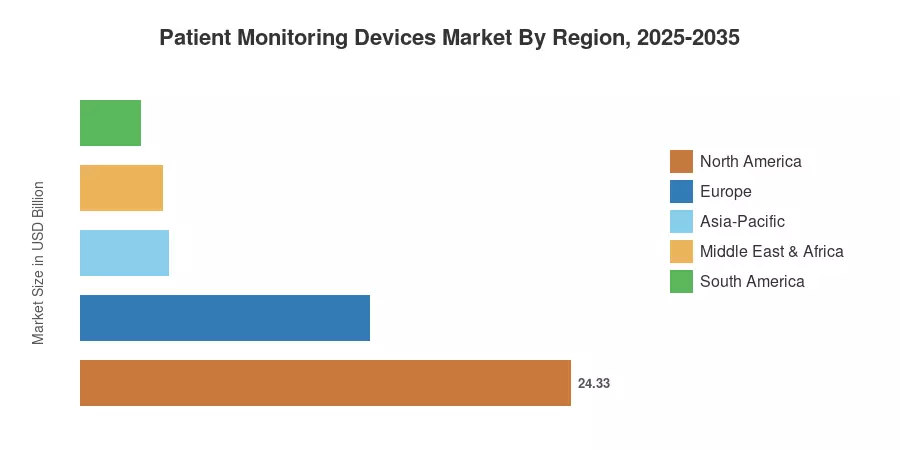

North America accounts for the greatest share of the Patient Monitoring Devices Market, with over 45.0% of 2025 revenue, owing to deep payer incentives and a mature hospital-IT backbone. Asia-Pacific has the highest regional CAGR of 8.10%, driven by government-led hospital digitization initiatives in India, China, and Southeast Asia. Europe is the second largest geographical position with about 26.5% share, showing a strong regulatory push for interoperability standards under the European Health Data Space program [5]. The Patient Monitoring Devices Market will transition from device-based to platform-based, outcome-based monitoring ecosystems over the next decade.

Key Report Takeaways

• By Device Type

- Multi-parameter monitors captured approximately 37.0% revenue share in 2024, maintaining their position as the anchor technology across acute-care settings.

- Neuromonitoring devices are forecast to expand at an 8.20% CAGR through 2035, propelled by rising neurosurgical procedure volumes and intraoperative monitoring mandates.

- Cardiac monitoring devices accounted for approximately USD 13.8 billion in 2024 revenue, reflecting sustained demand in electrophysiology and post-discharge surveillance.

• By End User

- Hospitals held approximately 62.5% of the Patient Monitoring Devices Market share in 2024, anchoring procurement cycles around integrated EMR-compatible systems.

- Home-care settings are advancing at an 8.70% CAGR through 2035, as RPM reimbursement and aging demographics redirect monitoring spend outside institutional walls.

• By Region

- North America contributed around 45.0% of global revenue in 2024, underpinned by payer-led RPM expansion and strong device replacement cycles.

- Asia-Pacific is the fastest-growing region at 8.10% CAGR, with China and India collectively adding over 12,000 ICU beds annually.

Market Size and Forecast (2021–2035)

Market Research Future estimates are derived from a triangulated methodology combining top-down revenue analysis from company filings, bottom-up demand modeling from hospital procurement databases, and cross-validated pricing benchmarks from GPO contract disclosures across 48 countries.