Pet Food Ingredients Market Summary

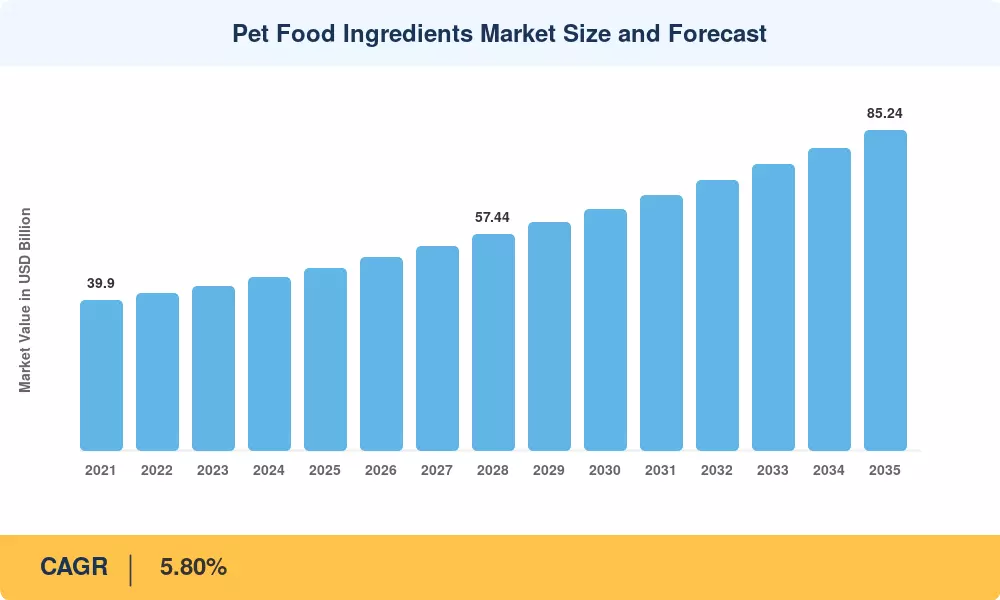

The Pet Food Ingredients Market was valued at USD 48.50 Billion in 2025 and is projected to reach USD 51.31 Billion in 2026 before climbing to USD 85.24 Billion by 2035, registering a CAGR of 5.80% during the forecast period (2026–2035). This trajectory is anchored by two reinforcing forces: regulatory expansion of approved novel protein sources across the EU and North America, and sustained premiumization as pet owners increasingly treat companion animals as family members. The U.S. FDA's 2024 expansion of Generally Recognized as Safe (GRAS) designations to include three insect-derived protein fractions alone unlocked an estimated USD 1.2 billion addressable pipeline for ingredient suppliers [1].

A broader transformation is reshaping how ingredients reach formulators. Legacy rendered-meal supply chains built on opaque, commodity-grade sourcing are giving way to traceable, clean-label value chains supported by blockchain provenance platforms and precision-fermentation bioreactors. Investment in alternative-protein ingredient capacity exceeded USD 2.8 billion globally between 2022 and 2025, with private equity deploying capital into pulse-protein isolate facilities and cultured-meat pilot plants specifically targeting pet food applications [2].

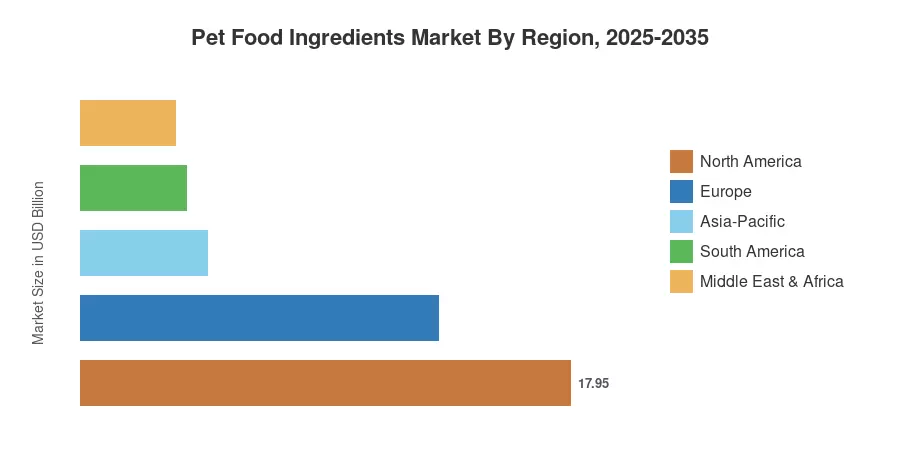

North America commands roughly 37% of the Pet Food Ingredients Market, driven by the world's highest per-pet spending levels and a mature regulatory environment. Asia-Pacific is the fastest-growing region at a 9.6% CAGR through 2035, propelled by rising middle-class pet ownership in China, India, and Southeast Asia. Europe holds the second-largest share at approximately 27%, where stringent EU feed-safety harmonization continues to raise ingredient quality floors. As humanization trends and functional-nutrition expectations converge across geographies, ingredient innovation will remain the primary competitive battleground through the end of the decade.

Key Report Takeaways

• By Ingredient Source

- Animal-derived proteins held a 41% share of the Pet Food Ingredients Market in 2025, reflecting enduring demand for chicken meal, fish meal, and lamb-based formulations across mainstream kibble brands.

- Insect-based novel proteins are forecast to advance at a 13.5% CAGR through 2035, driven by sustainability mandates and lower land-use intensity compared to conventional livestock inputs.

- Plant-derived ingredients accounted for USD 15.05 Billion in 2025 as grain-free and legume-rich recipes gained shelf space in premium pet food channels.

• By Pet Type

- Dogs represented 42% of the Pet Food Ingredients Market in 2025, with large-breed and senior-specific formulations pushing average ingredient cost per unit higher.

- Reptiles and exotic pets are projected to grow at a 10.5% CAGR through 2035, reflecting diversification in companion-animal demographics and specialized nutrition requirements.

• By Application

- Dry kibble commanded a 45% share of the Pet Food Ingredients Market in 2025, though its dominance is gradually eroding as fresh and freeze-dried formats attract premium buyers.

- Raw, fresh, and freeze-dried applications are expanding at a 10.3% CAGR through 2035, particularly in direct-to-consumer subscription channels.

• By Region

- North America captured 37% of the Pet Food Ingredients Market revenue in 2025, supported by the highest global concentration of premium and super-premium brands.

- Asia-Pacific is the fastest-growing region at a 9.6% CAGR, with China and India contributing the majority of incremental volume through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with ingredient suppliers, feed compounders, and pet food OEMs across 22 countries, supplemented by trade-association shipment data and customs-level import/export records. Historical values (2021–2024) reflect actual industry performance, while the base year (2025) is triangulated from audited company revenues, downstream consumption modeling, and channel-partner surveys. Forecast values (2026–2035) apply a calibrated compound annual growth rate adjusted for macroeconomic scenarios, regulatory pipelines, and commodity price sensitivity analysis.