Platelet Rich Plasma Market Summary

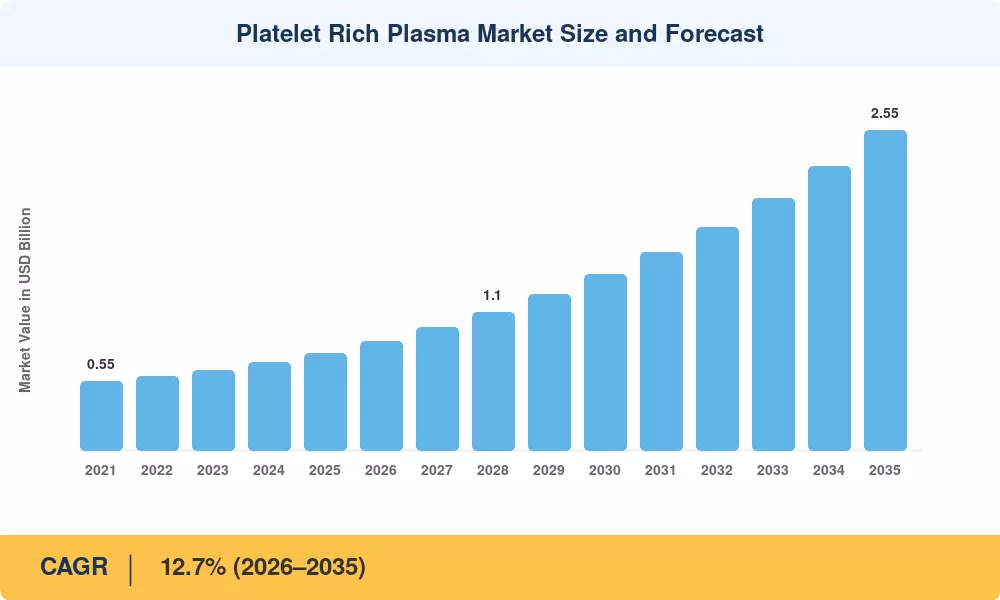

The Platelet Rich Plasma Market size was valued at USD 0.77 Billion in 2025, and the market is projected to grow from USD 0.87 Billion in 2026 to USD 2.55 Billion by 2035, registering a CAGR of 12.7% during the forecast period 2026–2035. This trajectory reflects a broader shift in clinical medicine toward minimally invasive biologics — a shift accelerated by insurance pathway expansion in orthopedic sports medicine and rising consumer willingness to pay out-of-pocket for aesthetic procedures [1]. The Platelet Rich Plasma Market sits at the intersection of regenerative medicine and point-of-care diagnostics, two sectors attracting sustained venture capital.

Clinical adoption has moved beyond early-adopter sports medicine clinics into mainstream hospital systems. Automated centrifuge platforms now standardize platelet concentration to within 5% variance, replacing manual preparation protocols that produced inconsistent yields. The U.S. FDA's updated guidance on autologous blood products (2024) reduced regulatory ambiguity, prompting device manufacturers to invest an estimated USD 320 million collectively in next-generation preparation kits between 2023 and 2025 [2]. These closed-system kits cut preparation time to under 15 minutes, making PRP viable in high-throughput outpatient settings.

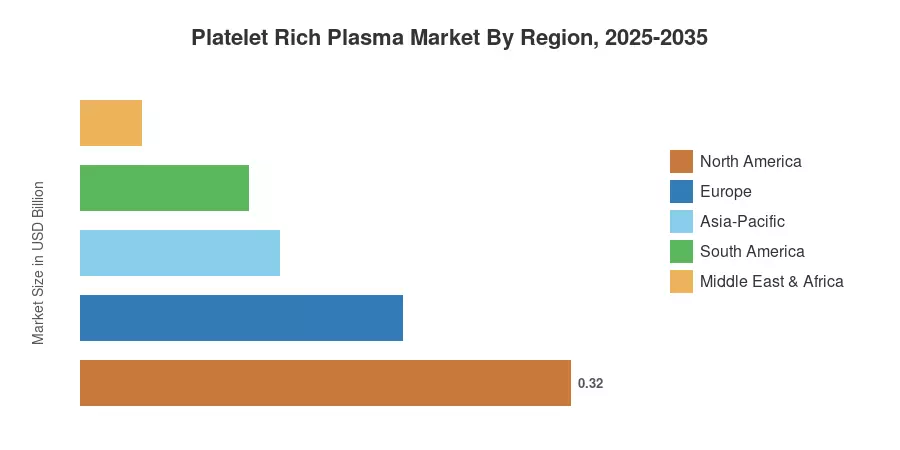

North America commanded approximately 42.0% of the Platelet Rich Plasma Market in 2025, anchored by insurance pilot programs and robust sports medicine infrastructure. Asia-Pacific is the fastest-growing region at a 16.7% CAGR through 2035, fueled by medical tourism demand and expanding private hospital networks. Europe held the second-largest position, driven by aesthetic medicine adoption in Germany, the UK, and France. As clinical evidence strengthens across dental, gynecological, and wound-care indications, the Platelet Rich Plasma Market is positioned for sustained double-digit expansion through the end of the forecast period.

Key Report Takeaways

• By Plasma Type

- Pure PRP captured 48.1% of the Platelet Rich Plasma Market in 2025, reflecting its broad applicability across orthopedic and aesthetic protocols.

- Leukocyte-Rich Fibrin is set for the fastest expansion at a 19.3% CAGR through 2035, driven by dental implantology and wound-healing applications.

• By Application

- Orthopedics and sports medicine represented 43.2% of the Platelet Rich Plasma Market share in 2025, underscoring the entrenched clinical adoption in tendon and ligament repair.

- Cosmetic and dermatological procedures are projected to escalate at an 18.9% CAGR, propelled by direct-to-consumer marketing and aesthetic tourism.

• By End User

- Hospital settings controlled 42.8% of the Platelet Rich Plasma Market size in 2025, owing to higher procedural volumes and reimbursement access.

- Specialty and ambulatory clinics are advancing at a 17.8% CAGR as PRP migrates into office-based settings.

• By Origin

- Autologous products constituted 91.3% of 2025 revenue, reflecting physician preference for patient-derived biologics.

- Allogeneic offerings are registering a 16.5% CAGR as donor-screening standardization matures.

• By Region

- North America held 42.0% of the Platelet Rich Plasma Market in 2025.

- Asia-Pacific is forecast to post the highest CAGR of 16.7% through 2035.

Platelet Rich Plasma Market Size and Forecast (2021–2035)

Market sizing draws on primary interviews with orthopedic surgeons, dermatologists, device distributors, and hospital procurement directors across 22 countries. Secondary inputs include FDA device clearance databases, national health expenditure registries, and peer-reviewed clinical trial repositories. All figures are expressed in USD Billion at constant 2025 exchange rates.