Market Share

Introduction: Navigating the Competitive Landscape of Power Semiconductors

The power semiconductor market is experiencing unprecedented competition, driven by rapid technological developments, changing regulations and a strong demand for energy efficiency and sustainable development. The main players, including system suppliers, IT service providers and system houses, are using the latest technology, such as artificial intelligence, the Internet of Things and green solutions, to establish their leadership in the market. Suppliers are focusing on improving the performance and reliability of their products, while IT companies are putting their focus on a perfect connection and automation. The new entrants, especially the AI startups, are challenging the established thinking and are changing the positioning of the suppliers. The opportunities for growth in the region, especially in Asia-Pacific and North America, are increasing, which is reflected in the strategic trends towards local production and sustainable production. In this dynamic environment, it is important to understand the technologically based differentiators that will determine market share and competitive advantage in the coming years.

Competitive Positioning

Full-Suite Integrators

These vendors offer a comprehensive range of power semiconductor solutions, integrating various technologies to serve diverse applications.

| Vendor | Competitive Edge | Solution Focus | Regional Focus |

|---|---|---|---|

| Infineon | Strong portfolio in power management | Power MOSFETs, IGBTs | Global |

| ON Semiconductor | Expertise in energy-efficient solutions | Power management ICs | North America, Europe, Asia |

| Texas Instruments | Broad analog and embedded processing | Power management solutions | Global |

| STMicroelectronics | Diverse semiconductor technologies | Power MOSFETs, IGBTs | Global |

Specialized Technology Vendors

These vendors focus on niche technologies within the power semiconductor space, providing specialized solutions for specific applications.

| Vendor | Competitive Edge | Solution Focus | Regional Focus |

|---|---|---|---|

| Vishay Intertechnology | Wide range of passive and active components | Power resistors, MOSFETs | Global |

| Renesas Electronics | Strong in automotive applications | Power management ICs | Asia, North America |

| Nexperia | Expertise in discrete semiconductors | Discrete MOSFETs, diodes | Global |

| Littelfuse | Focus on circuit protection solutions | Fuses, TVS diodes | Global |

Infrastructure & Equipment Providers

These vendors supply essential equipment and infrastructure for the production and application of power semiconductors.

| Vendor | Competitive Edge | Solution Focus | Regional Focus |

|---|---|---|---|

| Mitsubishi Electric Corporation | Strong in industrial applications | IGBTs, power modules | Asia, Europe |

| Toshiba | Innovative power device technologies | Power MOSFETs, IGBTs | Asia, North America |

| Fuji Electric | Expertise in power electronics | IGBT modules, power converters | Asia, Europe |

| Semikron | Focus on power semiconductor modules | IGBT modules, power modules | Global |

Emerging Players & Regional Champions

- GaN SYSTEMS of Canada specializes in gallium nitride power semiconductors for high-efficiency applications. It has recently won a contract to supply GaN power switches to a major manufacturer of EVs. GaN is replacing silicon in high-efficiency applications.

- Navitas Semiconductor (USA): focuses on GaN power ICs for fast charging and renewable energy applications. Recently it has teamed up with a leading mobile phone manufacturer to develop integrated charging solutions, thus complementing the traditional silicon suppliers with smaller, lighter, and more efficient solutions.

- Power Integrations (US): Offers power conversion solutions based on energy-efficiency principles. It recently launched a new family of ICs for EV chargers, thereby establishing itself as a challenger to established players by offering superior performance and lower costs.

- The first is Infineon. Infineon is a well-established company, but its recent focus on silicon carbide technology for use in the automobile makes it a regional champion. It has recently been awarded contracts from several European carmakers, enabling it to compete more successfully against the silicon suppliers.

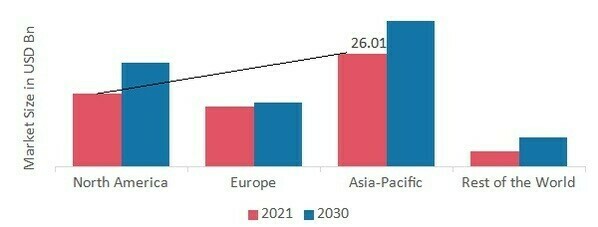

Regional Trends: In 2024, there is a noticeable trend towards the use of wide bandgap semiconductors, such as GaN and SiC, prompted by the growing demand for higher efficiency in electric vehicles and in the use of alternative energy sources. North America and Europe are the most specialised regions, with considerable R&D investment in advanced power semiconductors. In the meantime, Asia-Pacific is becoming a major manufacturing centre, with the local industry growing stronger.

Collaborations & M&A Movements

- Infineon and ST have joined together to develop next-generation power-diode solutions for the energy-saving drive of electric vehicles.

- In the beginning of 2024, Texas Instruments acquired the Analog Devices power-management division, in order to extend its product range and market share in the field of power semiconductors, in order to meet the increasing demand for power-efficient solutions in the field of consumer electronics.

- NXP Semiconductors and ON Semiconductors have entered into a joint venture to develop advanced power-management ICs for applications in the field of sustainable energy, thereby strengthening their position in the market for sustainable energy in the face of increasing regulatory pressure for green technology.

Competitive Summary Table

| Capability | Leading Players | Remarks |

|---|---|---|

| High-Efficiency Power Conversion | Infineon Technologies, Texas Instruments | CoolSiC technology from Infineon is well known for its power conversion applications. TI's power-management ICs are used extensively in the digital and mobile devices market. The company's power-management ICs are a good example of the company's strengths in high-efficiency solutions. |

| Wide Bandgap Semiconductors | Cree (Wolfspeed), ON Semiconductor | SiC has been a key technology in high-power applications, especially in electric vehicles and in applications for the production of energy from renewable sources. But the growth of GaN technology has also been very rapid. GaN solutions from ON Semiconductor are enabling the development of smaller, lighter and more efficient power systems. |

| Thermal Management Solutions | STMicroelectronics, Nexperia | STMicroelectronics offers advanced thermal management solutions integrated with their power semiconductors, enhancing reliability. Nexperia focuses on robust thermal performance in their MOSFETs, which are critical for automotive applications. |

| Integration with IoT | NXP Semiconductors, Analog Devices | NXP is leveraging its power semiconductors in IoT applications, providing secure and efficient power management. Analog Devices integrates power management with their sensor technologies, enhancing overall system performance in smart devices. |

| Sustainability Initiatives | Renesas Electronics, Infineon Technologies | Renesas is committed to sustainability, focusing on eco-friendly manufacturing processes and energy-efficient products. Infineon has launched initiatives to reduce carbon footprint in production, aligning with global sustainability goals. |

Conclusion: Navigating Power Semiconductor Market Dynamics

In 2024, the power-semiconductor market will be characterized by intense competition and significant fragmentation. Several companies will compete for the same share of the market, both from the historical and the new point of view. The regional trends are characterized by a growing focus on automation and sustainability, especially in North America and Asia-Pacific, where the demand for energy-saving solutions is increasing. Strategically, suppliers must strategically position themselves and rely on advanced capabilities such as artificial intelligence-driven design, flexible production and sustainable practices. The big companies, meanwhile, are focused on optimizing their existing technology, while new entrants are introducing innovations at a rapid pace, often outpacing the established way of thinking. It is therefore essential for decision-makers to be able to combine these capabilities in their strategies.

Leave a Comment