Retail Analytics Market Summary

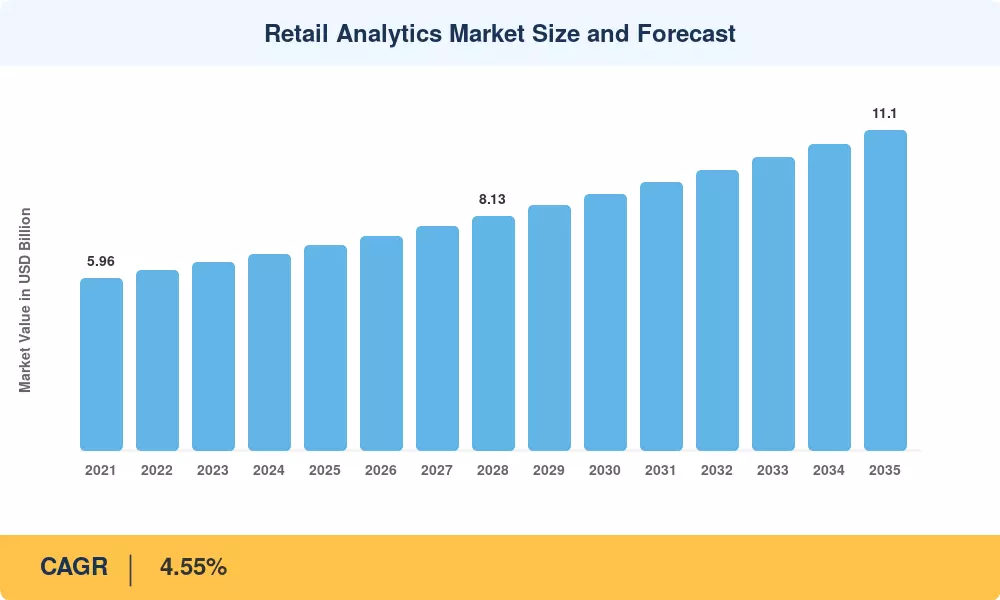

The Retail Analytics Market reached an estimated USD 7.12 Billion in 2025, with the forecast period opening at USD 7.44 Billion in 2026 and climbing to USD 11.10 Billion by 2035 at a 4.55% CAGR. Surging omnichannel commerce and a rapid pivot toward AI-embedded decision-making are compelling retailers to treat customer behavior analysis as an operational backbone rather than a discretionary investment. Governments in North America and the EU have also tightened data-governance mandates, which paradoxically accelerated analytics adoption by forcing brands to consolidate fragmented data lakes into compliant, insight-ready platforms [2].

Traditional spreadsheet-based reporting and segregated point-of-sale data analytics stacks are being replaced by cloud-native platforms that combine prescriptive inventory optimization tools with generative AI copilots. According to Adobe’s 2025 Digital Trends survey, 63% of today’s large retailers spend more than 5% of their digital budgets on real-time personalization engines, compared to less than 30% three years ago [1]. This shift is rethinking how merchants think about price, store space and promotional tempo.

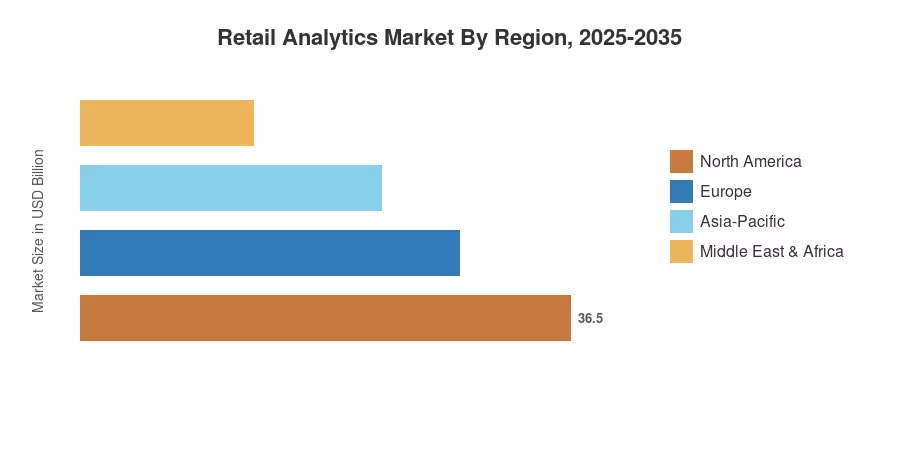

North America accounts for around 35.0% of the Retail Analytics Market, buoyed by a dense ecosystem of SaaS vendors and early-adopter supermarket and apparel chains. Asia-Pacific is the fastest expanding market with a predicted CAGR of 5.60% through 2035, led by the rise of digital retail in India, China and Southeast Asia. Europe is the second greatest contributor, boosted by improvements in data infrastructure during the GDPR era that now feed complex retail sales forecasting pipelines. The convergence of generative AI and prescriptive analytics points to a clear growth trajectory for the industry.

Key Report Takeaways

• By Solution

- Software accounted for 66.8% of the Retail Analytics Market expenditure in 2025, reflecting demand for unified dashboards and shopper journey insights platforms.

- Services represent the quickest-growth path at an 8.1% CAGR through 2035, driven by managed analytics and consulting engagements.

• By Function

- Customer management analytics captured a 23.5% share of the Retail Analytics Market in 2025, the largest functional slice.

- Marketing and merchandising analytics are on track for the sharpest acceleration at an 8.55% CAGR to 2035.

• By Geography

- North America dominated the Retail Analytics Market with a 35.0% revenue share in 2025, underpinned by retail sales forecasting maturity among top-50 chains.

- Asia-Pacific is forecast to grow at a 5.60% CAGR through 2035, the fastest of all regions.

Retail Analytics Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a combination of bottom-up vendor revenue modeling and top-down macroeconomic cross-checks for its estimates. Historical data (2021-2024) is based on published company filings. Forecasts are based on adoption surveys, IT budget trackers and point-of-sale data analytics implementation benchmarks from more than 400 retailers worldwide [3].