Retail Cloud Market Summary

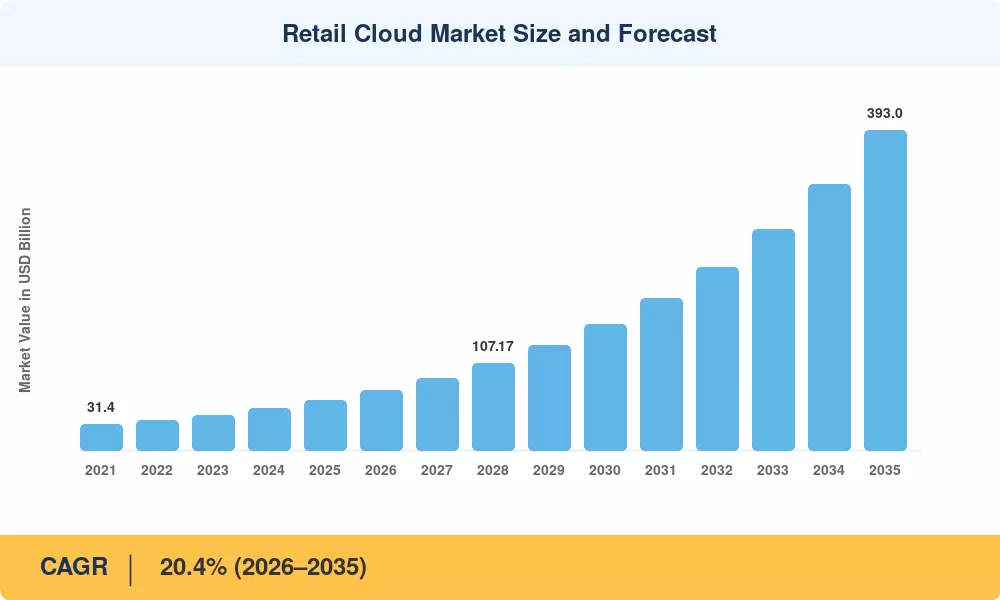

The Retail Cloud Market was valued at USD 61.40 Billion in 2025 and is projected to reach USD 393.00 Billion by 2035, expanding at a CAGR of 20.4% during the forecast period (2026–2035). This growth trajectory reflects the acceleration of digital commerce infrastructure worldwide, with retailers committing capital budgets to replace legacy on-premise systems. The U.S. National Retail Federation reported that IT spending among top-100 retailers climbed 14% year-over-year in 2024, with cloud migration accounting for the largest single budget line [1]. Government-led digital economy programs in the EU and India are compounding that momentum, pulling mid-market retailers toward hosted platforms faster than at any point in the past decade.

The technical shift transforming the Retail Cloud Market is the move from monolithic enterprise resource planning (ERP) installations to modular API-driven cloud systems. Retailers previously trapped into five-year on-premise upgrade cycles may now subscribe to always-updated platforms that include inventory, staff scheduling, and customer analytics in a single tenant. [2] 68% of tier-one retailers are expected to adopt cloud-first IT stacks in 2028, up from 41% in 2024. This change is driving spending at scale – worldwide retail IT investment reached USD 292 Billion in 2024, with about 22% of that going to cloud workloads [3].

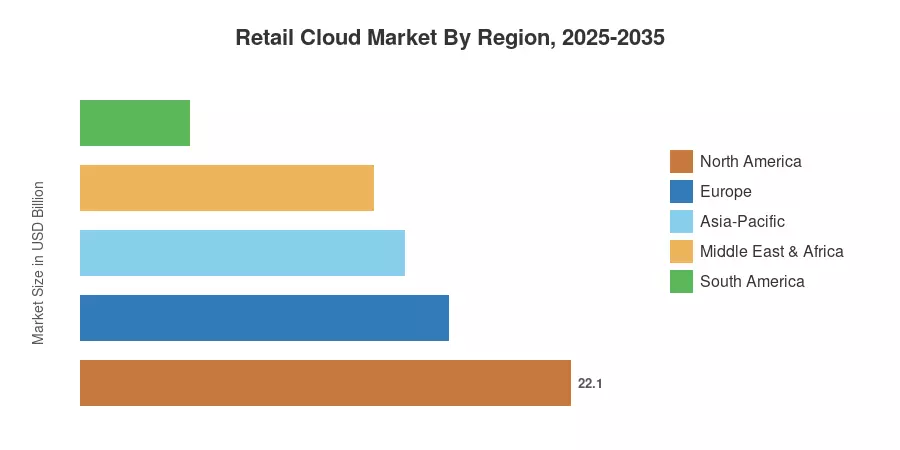

The U.S. and Canada have hyperscaler infrastructure and a developed e-commerce penetration, which is why North America accounts for about 36% of the Retail Cloud Market. The Asia-Pacific area is witnessing the fastest growth, with a predicted CAGR of 23.8%. This growth is being fueled by India’s Open Network for Digital Commerce (ONDC) program and the rising number of digitally-savvy consumers in Southeast Asia. Europe takes second place with roughly 27%, buoyed by the EU Digital Markets Act and cross-border retail harmonisation. The Retail Cloud Market is set to reshape the intersection of physical and digital retail for the remainder of the decade as cloud-native architectures develop and edge computing goes to store-level deployments.

Key Report Takeaways

• By Solution

- Customer Management solutions represent approximately 24% of the Retail Cloud Market, reflecting the priority retailers place on personalization engines and loyalty platforms.

- Supply Chain Management is projected to grow at a CAGR of 22.1% through 2035, fueled by demand for real-time visibility and predictive logistics.

- Reporting and Analytics solutions reached USD 9.82 billion in 2025 as retailers invested in unified dashboards spanning in-store and online channels.

• By Service Type

- SaaS dominates the Retail Cloud Market with roughly 52% revenue share, driven by low upfront costs and rapid deployment cycles.

- IaaS is expanding at a CAGR of 21.6% as large retailers build proprietary data lakes on hyperscaler infrastructure.

• By Region

- North America leads the Retail Cloud Market with a 36% share, supported by early hyperscaler adoption and high per-capita digital spend.

- Asia-Pacific is forecast to add USD 78.50 billion in incremental market value between 2026 and 2035, making it the top growth engine.

Market Size and Forecast (2021–2035)

Market Research Future's estimates combine bottom-up revenue modeling from vendor financials, top-down benchmarking against IT spending surveys, and primary interviews with CIOs across 18 retail sub-verticals. Historical figures reflect actual performance, while forecast values apply the calibrated 20.4% CAGR with adjustments for macro-economic cycles.