Supply Chain Analytics Market Summary

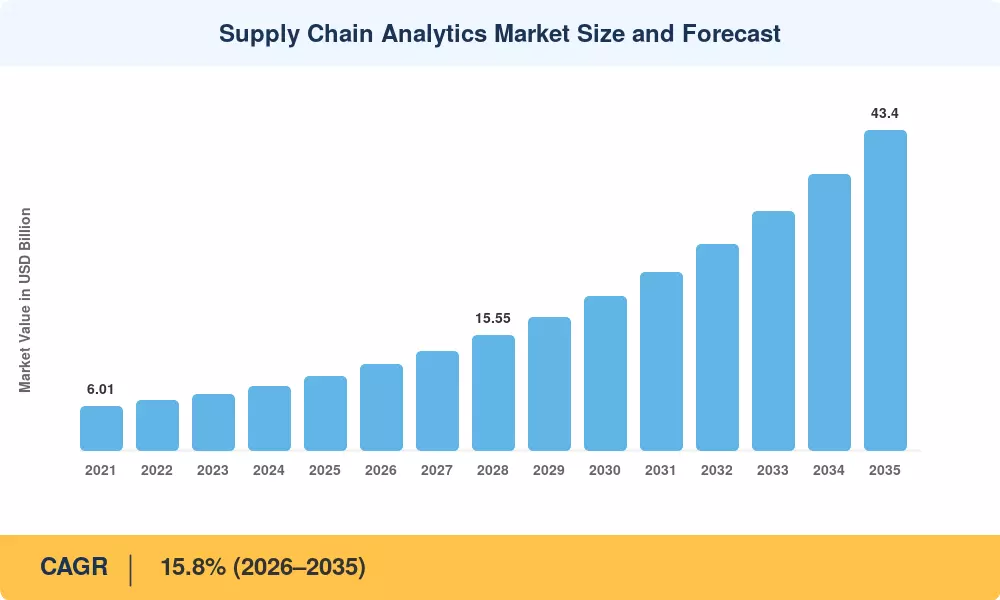

The Supply Chain Analytics Market was valued at USD 10.02 billion in 2025 and is projected to grow from USD 11.60 billion in 2026 to USD 43.40 billion by 2035, registering a CAGR of 15.8% during the forecast period (2026–2035). This expansion is anchored in the rapid digitization of procurement and logistics operations across industries, accelerated by government mandates such as the EU's Corporate Sustainability Reporting Directive (CSRD) and the U.S. SEC climate-disclosure rules that compel enterprises to instrument their supply chains with granular, auditable data pipelines [1].

Planning solutions tied to legacy ERP, which often only provide batch-processed, single-tier visibility, are being replaced by cloud-native, AI-enhanced platforms that can optimize many echelons in real time. It is believed that global organizations would have spent an estimated USD 18 billion on supply chain technology modernization for 2024 alone, with analytics platforms taking an increasing share of that spend [2]. Gen-AI copilots, digital-twin simulations and autonomous planning engines are shortening deployment timeframes from quarters to weeks, lowering the skill floor for mid-market adopters.

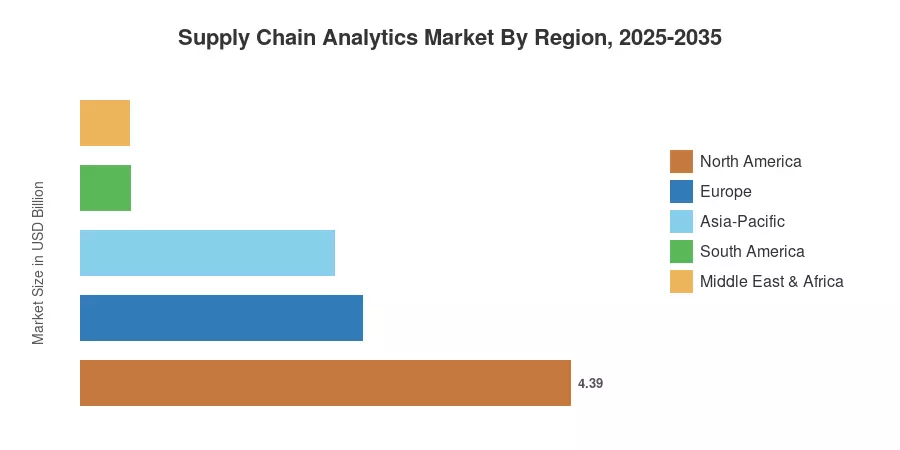

North America is anticipated to lead the Supply Chain Analytics Market with a projected share of 43.8% in 2025, fueled by established SaaS ecosystems and initial regulatory demands for Scope 3 reporting. Asia-Pacific is the fastest developing region with a projected CAGR of 22.8% through 2035, driven by manufacturing digitalization in China and India. Europe has the second greatest regional share of 25.2%, helped by CSRD compliance requirements and investment in green logistics. Analytics will go from a back-office cost center to a boardroom-grade strategic capability during the next decade.

Key Report Takeaways

• By Component

- Software accounted for approximately 71% of the Supply Chain Analytics Market in 2025, reflecting the maturity of demand-planning and network-design platforms.

- Services are expanding at a 22.5% CAGR through 2035, as implementation and managed analytics engagements grow alongside platform adoption.

• By Deployment

- Cloud deployment models held a 57% share in 2025 and continue to gain ground as subscription pricing displaces capital-intensive on-premise installations.

• By Application

- Inventory management captured a 30% share of the Supply Chain Analytics Market in 2025, anchored by safety-stock optimization and demand-sensing use cases.

• By Geography

- North America dominated with 43.8% of global revenue in 2025.

- Asia-Pacific is projected to register the highest CAGR at 22.8% during 2026–2035.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) employs a proprietary triangulation methodology in its market estimation and forecasting that references a number of data points for its validation purposes. Historical figures (2021-2024) are validated against publicly stated enterprise software revenues and third-party technology spending databases. The forecast forecasts incorporate industry-specific adoption curves and is stress-tested against GDP growth, volatility in trade flows and technology investment indexes.