Sexual Wellness Market Summary

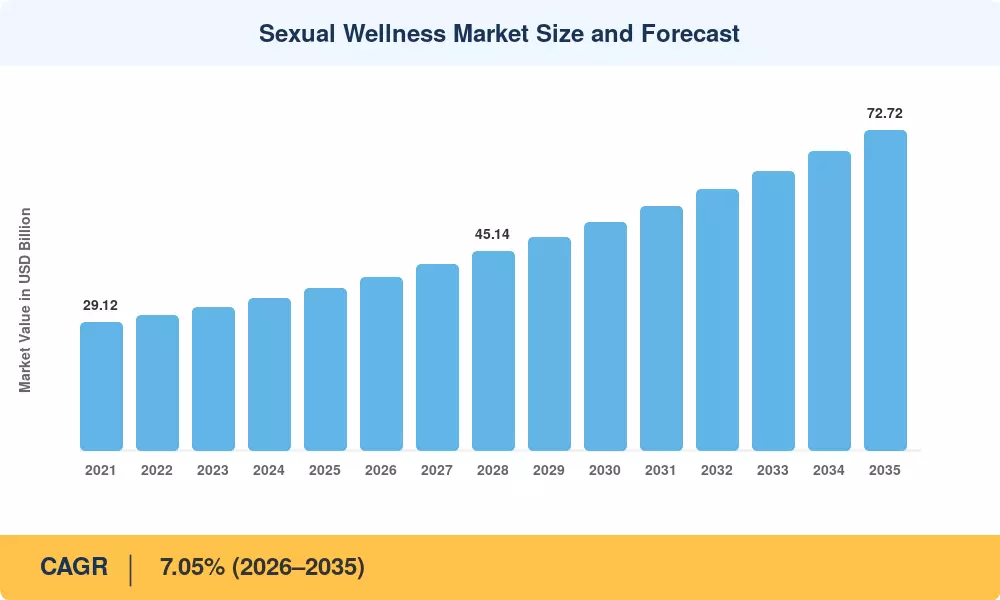

The Sexual Wellness Market size was valued at USD 36.80 Billion in 2025, and the market is projected to grow from USD 39.39 Billion in 2026 to USD 72.72 Billion by 2035, registering a CAGR of 7.05% during the forecast period 2026–2035. Two structural catalysts are propelling this expansion: a global destigmatization wave anchored by public health campaigns—most recently, the UNFPA's USD 1.2 billion sexual and reproductive health initiative across 46 countries [1]—and the rapid shift of purchasing behavior onto digital platforms that reward discretion and personalization.

A technological transformation is reshaping the Sexual Wellness Market from the inside out. Legacy analog products—basic latex condoms, generic lubricants—are being supplemented by app-connected devices, body-safe medical-grade silicone formulations, and subscription-based wellness kits that leverage behavioral data to drive repeat engagement. Corporate venture arms poured an estimated USD 480 million into intimate-technology startups between 2022 and 2024, signaling that investors view this category as a mainstream consumer health play rather than a niche segment [2].

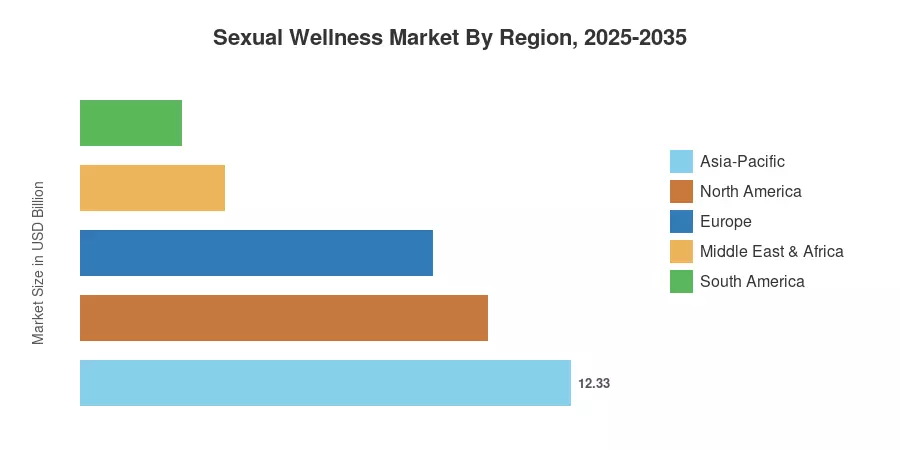

Asia-Pacific commands roughly 33.50% of global Sexual Wellness Market revenue, driven by high population density and rapidly expanding e-commerce infrastructure across China, India, and Southeast Asia. Middle East & Africa is the fastest-growing region at a 9.85% CAGR, propelled by smartphone-led retail adoption that bypasses traditional brick-and-mortar distribution barriers. Europe holds the second-largest share at 24.10%, supported by progressive regulatory frameworks and robust pharmacy-based distribution channels. As connected devices and telehealth platforms continue to blur the line between consumer wellness and clinical health, the Sexual Wellness Market is positioned for sustained double-digit growth in several sub-segments through 2035.

Key Report Takeaways

• By Product

- Condoms accounted for 38.50% of the Sexual Wellness Market in 2025, reflecting entrenched retail distribution and public health procurement channels.

- Connected sex toys are advancing at a 12.60% CAGR through 2035, the fastest-growing product category within the Sexual Wellness Market.

• By Material

- Latex and natural rubber commanded 50.80% of the Sexual Wellness Market by material in 2025.

- Medical-grade silicone is expanding at an 11.70% CAGR, driven by allergen-free and body-safe positioning.

• By Distribution Channel

- Online retail captured 47.40% of the Sexual Wellness Market in 2025 and leads future growth at a 12.85% CAGR.

• By End User

- Women represented 58.20% of the Sexual Wellness Market in 2025.

- The LGBTQ+ cohort is the fastest-growing end-user segment at a 10.25% CAGR.

• By Region

- Asia-Pacific held 33.50% of Sexual Wellness Market revenue in 2025.

- Middle East & Africa is expanding at a 9.85% CAGR, the quickest among all regions.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework triangulates bottom-up revenue tracking from manufacturer shipments, retail panel data, and e-commerce analytics against top-down demand models calibrated to demographic, regulatory, and macroeconomic indicators. Historical figures (2021–2024) reflect audited industry data; the base year (2025) is the latest validated estimate; forecast values (2026–2035) apply a compound growth trajectory consistent with structural demand drivers identified in Sections 4–6.