Mental Health Market Summary

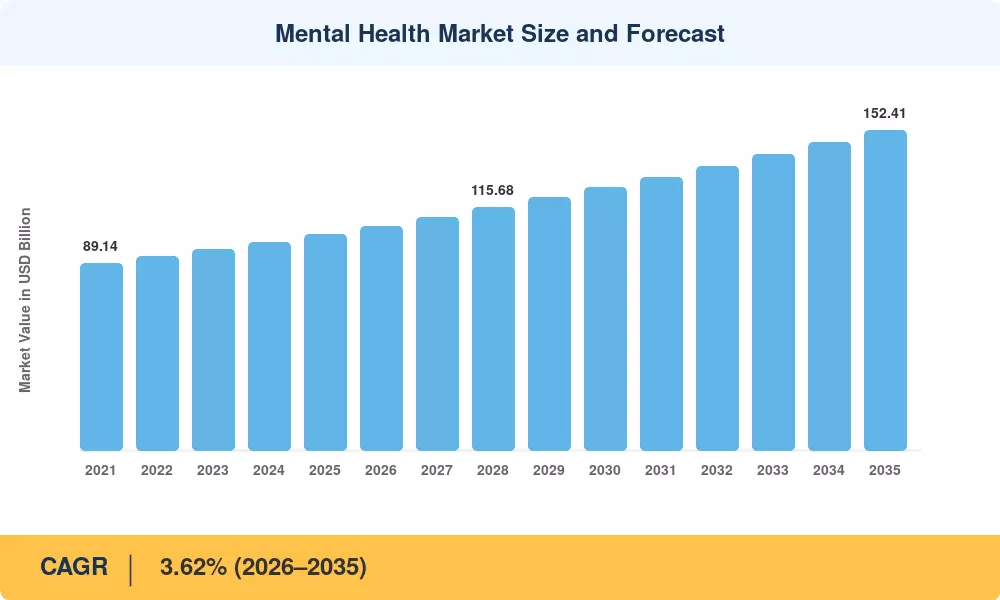

The mental health market reached an estimated USD 102.78 billion in 2025 and is projected to grow from USD 106.58 billion in 2026 to USD 152.41 billion by 2035, registering a CAGR of 3.62% across the forecast window. Two catalysts are reshaping this trajectory: the enforcement of behavioral-physical parity laws now active in 16 U.S. states, and employer-funded digital platforms that absorbed roughly 24% more counseling sessions in 2025 than legacy employee assistance programs [1]. These policy and spending shifts have turned psychiatric disorder treatment from a clinical afterthought into a boardroom priority.

A technological transformation is underway. Brick-and-mortar therapy models are yielding ground to FDA-cleared digital therapeutics for anxiety and depression care, bolstered by new CPT reimbursement codes introduced in 2024 that unlocked Medicare coverage for software-based behavioral therapy interventions [2]. Venture-backed platforms such as Spring Health and Lyra Health have compressed time-to-care by approximately 37%, forcing traditional providers to invest in data-integrated triage or risk margin erosion. The U.S. Department of Health and Human Services allocated USD 1.5 billion toward community mental wellness counseling centers in FY 2025, underscoring the federal commitment [3].

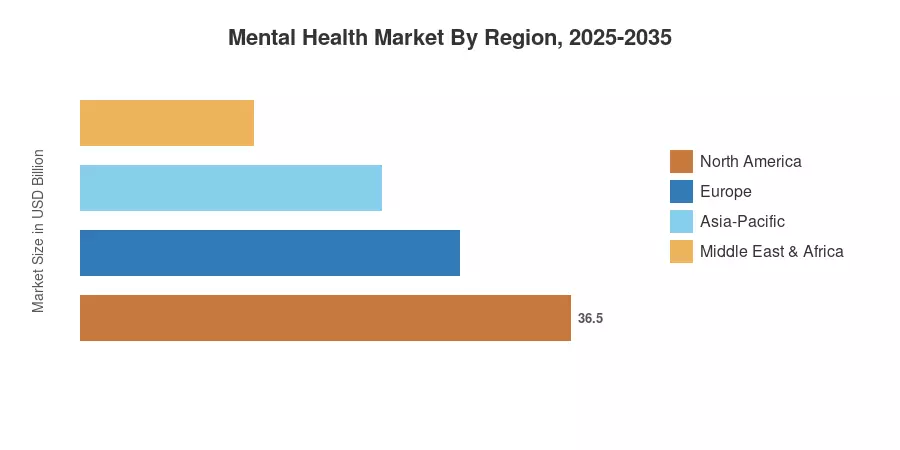

North America commands roughly 41% of the mental health market, anchored by insurance mandates and corporate wellness budgets. Asia-Pacific is the fastest-growing region at a projected 6.18% CAGR, driven by India's National Tele Mental Health Programme and China's expanding psychopharmacology medications reimbursement lists [4]. Europe holds the second-largest share, near 27%, supported by the EU's Comprehensive Approach to Mental Health adopted in 2023. The decade ahead will hinge on whether low- and middle-income nations can scale task-shifting models fast enough to close a global psychiatrist shortfall that still averages just 2.1 clinicians per 100,000 population [5].

Key Report Takeaways

• By Disorder

- Depression accounted for a 37.94% revenue share of the mental health market in 2025, driven by rising screening mandates across primary-care settings

- PTSD is positioned as the fastest-expanding disorder segment, advancing at a 5.68% CAGR through 2035 as veteran-focused clinics and trauma-informed care models proliferate

- Anxiety disorders contributed approximately USD 24.67 billion in 2025, reflecting increased diagnosis rates among working-age adults

• By Service Type

- Outpatient counseling held a 45.39% share of the mental health market in 2025, reinforced by telehealth parity legislation

- Digital therapeutics are progressing at a 7.18% CAGR, the fastest service-type growth rate, as payers expand reimbursement for app-based behavioral therapy interventions

• By Region

- North America led with 41.02% of global value in 2025

- Asia-Pacific is projected to record a 6.18% CAGR to 2035, making it the fastest-growing region for the mental health market

- Europe captured roughly USD 27.75 billion in 2025

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s estimates combine bottom-up revenue modeling from provider and payer databases with top-down cross-validation against national health expenditure accounts, WHO mental health atlases, and proprietary survey panels covering 42 countries. Historical figures reflect actual reported revenues; forecast values apply the calibrated 3.62% CAGR with adjustments for regulatory milestones and demographic shifts in psychiatric disorder treatment demand.