Soda Ash Market Summary

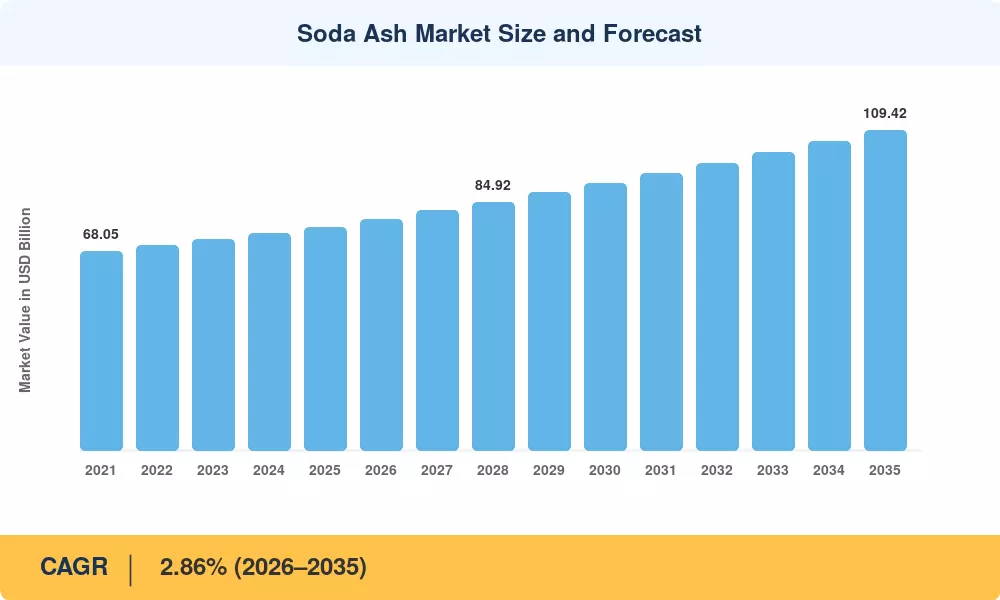

The Soda Ash Market reached an estimated 76.18 million tons in 2025 and is projected to start the forecast window at 78.04 million tons in 2026 before climbing to 109.42 million tons by 2035, registering a CAGR of 2.86% across the outlook period. Two catalysts anchor that trajectory: India's Production-Linked Incentive scheme channeling over USD 1.2 billion into flat-glass capacity, and China's mandate requiring 30% cullet utilization in container glass by 2030—both of which sustain robust sodium carbonate offtake [2][3].

A structural production shift is reshaping the Soda Ash Market's cost curve. Carbon-intensive Solvay-process plants in Europe and China face tightening emissions caps under the EU Carbon Border Adjustment Mechanism, accelerating retirement of legacy synthetic capacity. Trona-based producers in Wyoming's Green River Basin and Türkiye's Kazan district are absorbing the displaced volume, with Genesis Energy and WE Soda collectively investing over USD 800 million in solution-mining expansions through 2028 [4]. Dense soda ash availability is tightening as photovoltaic glass production scales, pushing producers to prioritize industrial alkali materials for solar panel manufacturing lines.

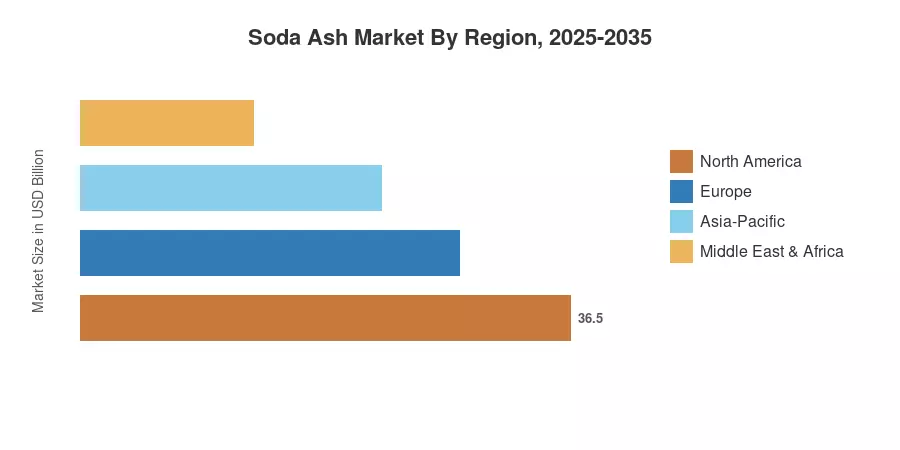

Asia-Pacific commands roughly 46% of global consumption, underpinned by China's glass manufacturing chemicals demand and India's detergent sector expansion. The Middle East & Africa region is the fastest-growing corridor in the Soda Ash Market, driven by Gulf construction megaprojects, while North America holds the second-largest share at approximately 21%, buoyed by natural trona extraction advantages

Key Report Takeaways

• By Type

- Dense soda ash led with approximately 62% of Soda Ash Market volume in 2024, reflecting persistent pull from flat glass and photovoltaic glass lines

- Light soda ash is forecast to expand at a 4.21% CAGR through 2035, propelled by rising detergent chemicals consumption across South and Southeast Asia

• By Source

- Synthetic plants (Solvay, Hou, dual-process) retained roughly 56% revenue share in 2024, though tightening carbon regulations erode their cost advantage

- Natural trona-based extraction is positioned to grow at a 4.48% CAGR between 2026 and 2035

• By Application

- Glass manufacturing captured an estimated 55% of the Soda Ash Market revenue in 2024, spanning flat, container, and specialty glass segments

- Water treatment chemicals applications show the fastest trajectory at a 5.34% CAGR through 2035

• By End-User

- Building and construction commanded roughly 41% of 2024 revenues within the Soda Ash Market

- Renewable energy end-uses are projected to climb at a 5.52% CAGR through 2035

• By Region

- Asia-Pacific accounted for 46% of 2024 consumption in the Soda Ash Market

- The Middle East & Africa region promises the fastest regional expansion, with a CAGR of 4.08% over the outlook period

Soda Ash Market Size and Forecast (2021–2035)

MRFR's estimates blend bottom-up plant-level capacity data with top-down trade-flow modeling. Historical figures draw on UN Comtrade records, national chemical industry associations, and company annual reports. Forecast projections apply a calibrated CAGR anchored to glass manufacturing chemicals demand pipelines, detergent chemicals consumption surveys, and announced capacity expansions across trona and synthetic routes[5].