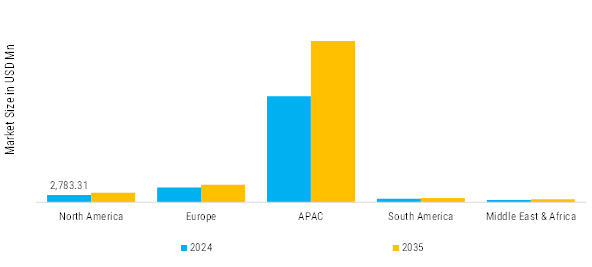

North America: Expanding Mature stainless-steel

North America represents a mature stainless-steel market with high per capita consumption, advanced manufacturing, and strict environmental regulations. The United States, Canada, and Mexico are the largest consumers, with applications across automotive, aerospace, chemical, energy, and construction sectors. Stainless steel demand is driven by replacement of carbon steel in corrosion-sensitive applications, infrastructure modernization, and automotive lightweighting initiatives to meet fuel efficiency standards. The region emphasizes high-quality, specialty, and value-added stainless-steel grades such as duplex and 316L for demanding industries. In the U.S., investment in renewable energy, defense, and medical equipment further supports consumption growth. While domestic production is robust, the region also imports stainless steel from Europe and Asia to meet demand for specific grades and finishes. Trade policies, tariffs, and technological innovations in processing and recycling influence market dynamics, making North America a stable yet competitive market for stainless steel.

Europe: Strong Production stainless-steel

Europe is a key global stainless-steel hub, characterized by strong production and consumption across Germany, Italy, France, and the UK. The market is driven by the automotive, aerospace, chemical, and construction sectors, where corrosion resistance, aesthetics, and sustainability are critical. European manufacturers focus on high-grade stainless steel, including duplex, 304, 316, and specialty finishes for industrial and architectural applications. Regulatory frameworks such as REACH and EU environmental standards drive demand for sustainable and recyclable materials. The region also emphasizes advanced manufacturing technologies and precision processing, including laser cutting, polishing, and surface treatments. Europe imports and exports stainless steel to meet grade-specific demands, particularly from Asia Pacific. Growth in infrastructure modernization, renewable energy projects, and premium consumer goods supports ongoing stainless-steel consumption. Overall, Europe maintains a mature, innovation-driven market with strong emphasis on quality, performance, and environmental compliance.

Asia Pacific: Fastest Growing stainless steel

Asia Pacific is the largest and fastest-growing stainless steel market globally, led by China, India, Japan, South Korea, and Southeast Asian countries. Growth is fueled by rapid urbanization, industrialization, infrastructure development, and expanding manufacturing sectors. China dominates production and consumption, supplying a wide range of stainless-steel grades to domestic and export markets. In India, rising automotive, construction, appliance, and energy sectors are driving strong demand. Stainless steel is increasingly used in high-value applications, including chemical plants, food processing, medical equipment, and renewable energy. Government initiatives supporting infrastructure and manufacturing under programs like “Make in India” are further boosting market potential. Asia Pacific also benefits from low production costs, large-scale mills, and investments in advanced processing technologies. The region’s robust industrial base, growing middle class, and rising export markets make it a key driver of global stainless-steel demand.

South America: Growing stainless steel

South America represents a growing stainless-steel market, led by Brazil, Argentina, and Chile, driven by automotive, construction, chemical, and food processing industries. Demand is influenced by industrial expansion, urban infrastructure projects, and growing middle-class consumption. Brazil is the largest consumer and producer, with stainless steel used in piping, storage tanks, food processing, and appliances. Import dependence remains significant for specialized grades and high-quality flat products. The region faces volatility due to economic fluctuations, currency instability, and trade policies, affecting stainless steel pricing and investment. Globally, South American countries rely on imports from Asia and Europe to meet demand for specialty grades and high-value products. With increasing infrastructure development, renewable energy projects, and industrial modernization, stainless steel consumption in South America is expected to grow steadily, especially in food, beverage, chemical, and automotive applications.

Middle East & Africa: Emerging stainless essentials

The Middle East & Africa (MEA) stainless steel market is primarily driven by oil & gas, petrochemicals, construction, and infrastructure projects. Countries such as Saudi Arabia, UAE, Qatar, South Africa, and Egypt are major consumers. Stainless steel is essential in pipelines, refinery equipment, storage tanks, and large-scale construction due to its corrosion resistance in harsh climates and saline environments. The region imports a significant share of stainless steel, particularly high-grade and specialty products, from Asia and Europe. Rising urbanization, large-scale construction, and industrial diversification programs, such as Saudi Vision 2030, are fueling stainless steel demand. In Africa, growth is supported by mining, infrastructure, and water treatment projects. Globally, MEA is considered a strategic market for stainless steel suppliers due to its high-value applications, long-term infrastructure investments, and emphasis on durability, reliability, and low-maintenance materials in extreme environmental conditions.