Stem Cell Manufacturing Market Summary

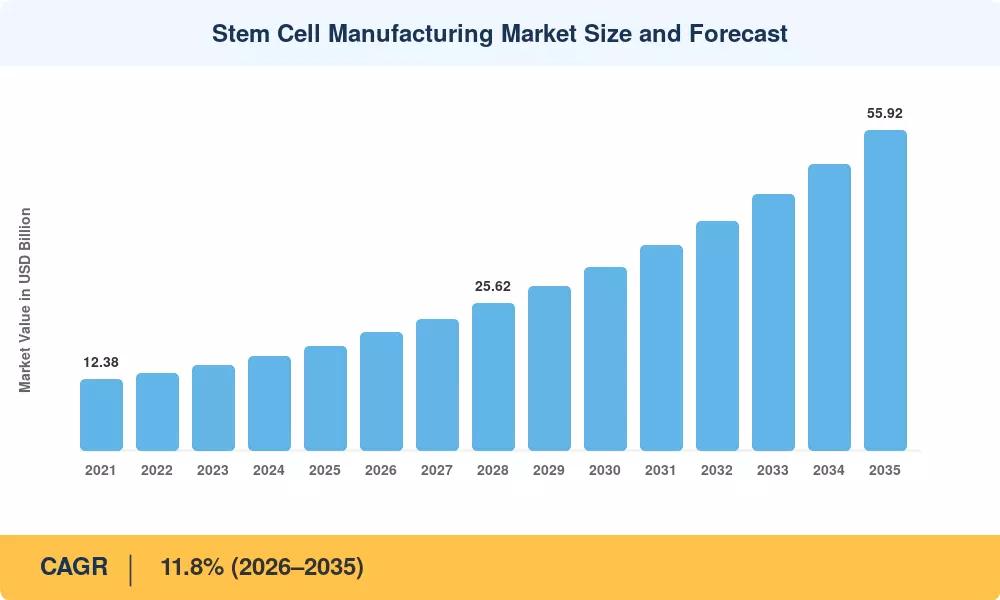

The Global Stem Cell Manufacturing Market size was valued at USD 18.22 Billion in 2025, and the market is projected to grow from USD 20.54 Billion in 2026 to USD 55.92 Billion by 2035, registering a CAGR of 11.8% during the forecast period 2026–2035. Two forces anchor this trajectory: the U.S. National Institutes of Health allocated over USD 2.1 Billion to stem cell research grants in fiscal year 2024, while the European Commission earmarked EUR 1.4 Billion for advanced therapy medicinal product (ATMP) infrastructure under Horizon Europe [1]. These public capital flows are matched by private investment, as late-stage cell therapy pipelines demand scalable, regulatory-grade production capacity.

A fundamental technology shift is reshaping the Stem Cell Manufacturing Market. Legacy open-vessel, flask-based culture systems are giving way to automated closed-system bioreactors equipped with in-line process analytical technology. Manufacturers are investing in single-use assemblies and robotic liquid-handling platforms to reduce batch failure rates by an estimated 35–40% [2]. Japan's Act on the Safety of Regenerative Medicine, updated in 2023, set a global precedent by harmonizing manufacturing standards for autologous and allogeneic therapies, prompting similar regulatory modernization across South Korea and the EU [3].

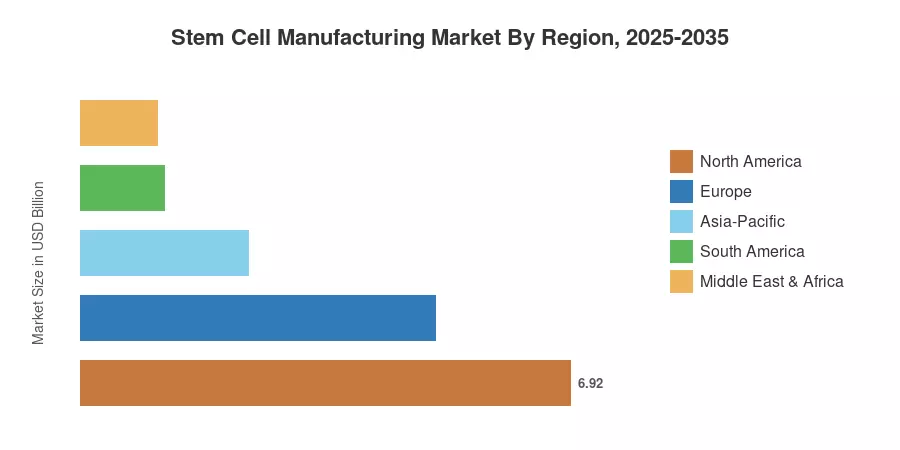

North America commands approximately 38.0% of the Stem Cell Manufacturing Market, driven by a robust FDA regulatory pathway and concentrated venture capital activity. Asia-Pacific is the fastest-growing region, expanding at a 13.0% CAGR through 2035 as China and Japan accelerate policy liberalization. Europe holds the second-largest share at roughly 27.5%, underpinned by the EMA's advanced therapy framework and strong academic research networks [4]. As cell and gene therapy approvals accelerate globally, demand for scalable manufacturing infrastructure will define competitive positioning over the next decade.

Key Report Takeaways

• By Product Type

- Consumables captured 43.2% of the Stem Cell Manufacturing Market share in 2025, reflecting their repeat-purchase nature in every production cycle.

- Instruments are projected to grow at a 12.6% CAGR through 2035, as automation platforms replace manual workflows.

• By Application

- Stem cell therapy accounted for 47.4% of the Stem Cell Manufacturing Market in 2025, supported by a growing clinical pipeline of CAR-T and MSC-based treatments.

- Stem cell banking is poised for the fastest expansion at a 13.4% CAGR to 2035.

• By End User

- Pharmaceutical and biotechnology companies held 55.3% revenue share in 2025, reflecting their dominance in commercial-scale production.

- Academic and research institutes are forecast to rise at a 12.8% CAGR through 2035.

• By Region

- North America led the Stem Cell Manufacturing Market with a 38.0% share in 2025.

- Asia-Pacific is expanding fastest at a 13.0% CAGR, driven by Japan and China policy reforms.

Market Size and Forecast (2021–2035)

Market Research Future's estimates for the Stem Cell Manufacturing Market draw on primary interviews with over 120 industry stakeholders, validated against public financial filings, regulatory databases, and trade association data. Historical figures reflect reported revenues from major manufacturers and CDMOs, while forecast projections apply bottom-up segmental modeling calibrated to pipeline throughput, capacity expansion announcements, and reimbursement trends.