Surgical Navigation Systems Market Summary

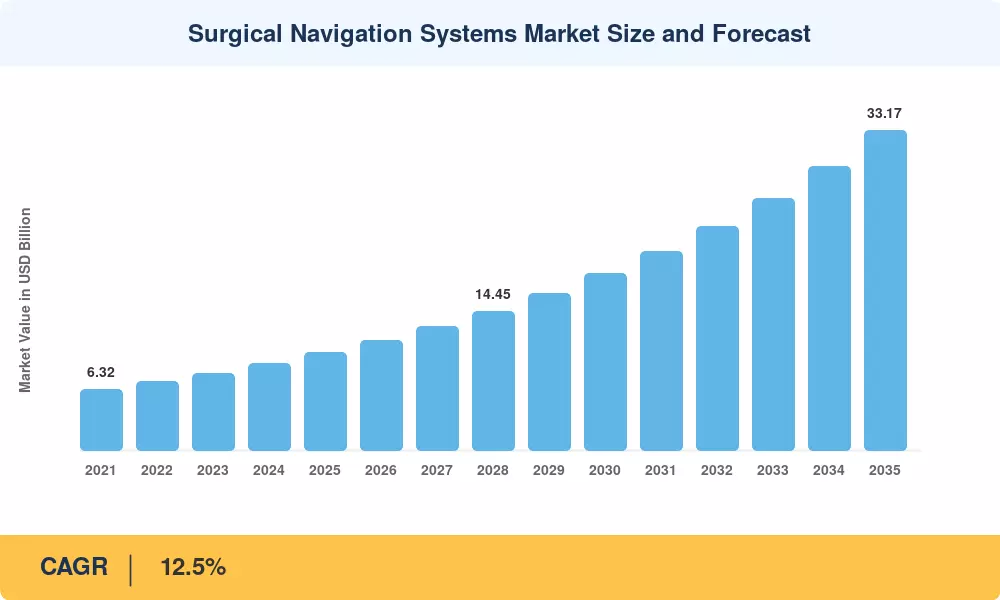

The Global Surgical Navigation Systems Market size was valued at USD 10.12 Billion in 2025, and the market is projected to grow from USD 11.49 Billion in 2026 to USD 33.17 Billion by 2035, registering a CAGR of 12.5% during the forecast period 2026–2035. Two powerful catalysts sit behind that trajectory: bundled-payment reimbursement models that reward hospitals for demonstrable outcome improvements, and a global push toward minimally invasive workflows that slash revision rates by up to 40% in complex spinal and cranial procedures[2]. These policy and clinical incentives have turned image-guided surgery systems from premium add-ons into operational necessities.

Legacy fluoroscopy-only setups are giving way to hybrid platforms that merge intraoperative navigation technology with AI-powered planning modules. Computer-assisted surgical planning now integrates pre-operative CT and MRI datasets into real-time anatomical tracking overlays visible during the procedure, cutting average operative times by 15–22 minutes in peer-reviewed orthopedic trials [3]. Capital commitments reflect the shift — Medtronic, Stryker, and Brainlab collectively channeled over USD 1.8 billion into R&D for 3D surgical navigation tools between 2023 and 2025, with a focus on machine-learning algorithms that adapt instrument trajectories mid-surgery [4].

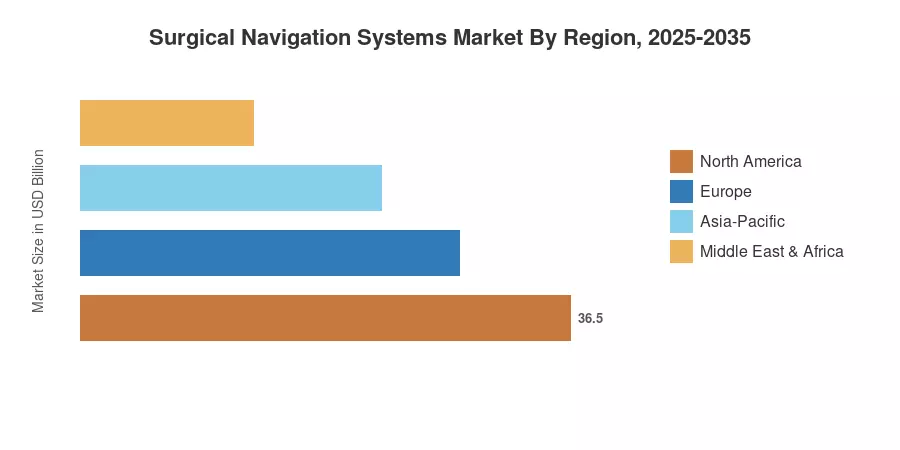

North America commands roughly 35.2% of the Surgical Navigation Systems Market, backed by high hospital IT maturity and favorable CMS reimbursement codes Asia-Pacific is the fastest-growing region at an 8.35% CAGR, driven by infrastructure buildouts across China, India, and ASEAN nations. Europe holds the second-largest share at approximately 28.5%, anchored by Germany's medtech export corridor and the UK's NHS digital-surgery programs [5]. As robotic-assisted platforms increasingly embed intraoperative GPS for surgeons, the competitive landscape will reward vendors that balance clinical precision with cybersecurity compliance.

Key Report Takeaways

• By Technology

- Electromagnetic navigation systems captured 38.2% of the Surgical Navigation Systems Market in 2025, reflecting deep clinical entrenchment in neurosurgery suites

- Optical navigation systems are projected to post the fastest segment CAGR of 7.45% through 2035, driven by 3D surgical navigation tools that pair with robotic arms

- Hybrid navigation systems accounted for approximately USD 2.18 billion in 2025 revenue, as hospitals consolidate image-guided surgery systems into single-platform ecosystems

• By Application

- Neurosurgery represented 36.4% share of the Surgical Navigation Systems Market in 2025, underscoring the criticality of real-time anatomical tracking in cranial procedures

- ENT surgery is the fastest-expanding application at an 8.55% CAGR through 2035

- Orthopedic surgery generated approximately USD 2.85 billion in 2025, with computer-assisted surgical planning gaining traction in joint-replacement workflows

• By End User

- Hospitals and academic medical centers held 62.8% of Surgical Navigation Systems Market revenue in 2025

- Ambulatory surgical centers recorded the strongest end-user CAGR of 9.35% through 2035

• By Region

- North America led with 35.2% share; Asia-Pacific posted the fastest growth at 8.35% CAGR

Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model triangulates bottom-up procedure volumes, average selling prices per navigation platform, and top-down healthcare capital expenditure data across 42 countries. Historical values (2021–2024) are anchored to audited company filings; the 2025 base year blends primary survey responses with secondary trade data. The forecast period (2026–2035) applies a compounding growth framework calibrated to clinical adoption curves and reimbursement expansion timelines.

.webp?v=1782976096)