Transaction Monitoring Market Summary

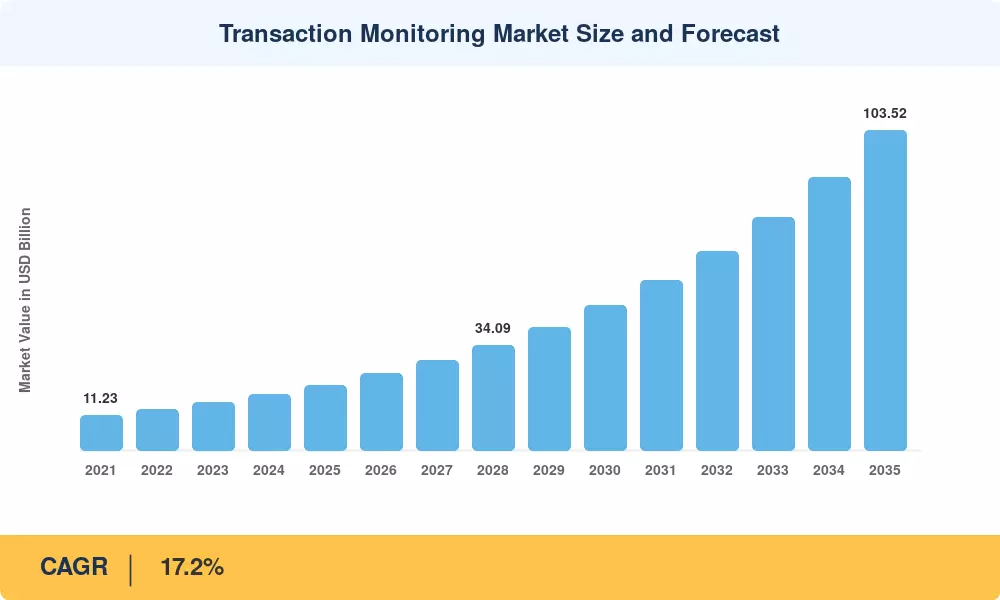

The Transaction Monitoring Market was valued at USD 21.18 Billion in 2025 and is projected to reach USD 24.82 Billion by 2026, climbing to USD 103.52 Billion by 2035 at a CAGR of 17.2% during the forecast period (2026–2035). This acceleration is rooted in tightening global anti-money-laundering mandates — the EU's Anti-Money Laundering Authority (AMLA), formally seated in 2025, now compels direct supervisory oversight of high-risk financial institutions across 27 member states [1]. Simultaneously, the Financial Crimes Enforcement Network (FinCEN) in the United States expanded beneficial-ownership reporting requirements under the Corporate Transparency Act, broadening the compliance surface area for banks, fintechs, and payment processors [2].

A decisive shift is underway from static, rule-based alert engines toward AI-native platforms that fuse entity resolution, network analytics, and real-time payment monitoring into unified compliance stacks. Legacy systems built on batch-processing architectures are giving way to cloud-deployed microservices capable of scoring millions of transactions per second. Global spending on compliance technology surpassed USD 35 Billion in 2024, with financial institutions channeling roughly 18% of that figure into transaction surveillance modernization [3]. Integrated "FRAML" architectures — combining fraud, AML, and sanctions screening in a single data pipeline — are rapidly becoming the procurement default for Tier-1 and Tier-2 banks.

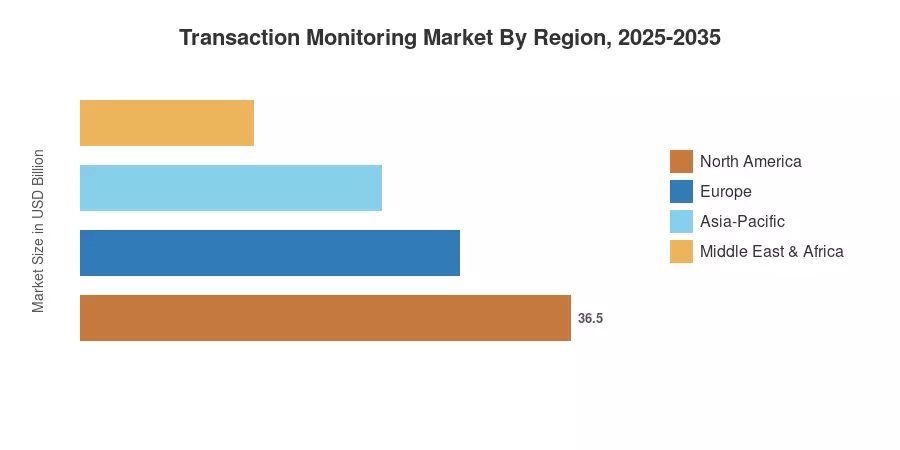

North America commanded approximately 30.4% of the Transaction Monitoring Market in 2025, anchored by stringent U.S. Bank Secrecy Act enforcement and Canada's FINTRAC regime. Asia-Pacific is the fastest-growing region at an 18.5% CAGR through 2035, driven by India's Digital Personal Data Protection Act and China's cross-border payment oversight expansion. Europe holds the second-largest share, propelled by MiCA implementation and AMLA's cross-border supervisory mandates. As digital payment volumes accelerate past USD 15 Trillion annually worldwide, the Transaction Monitoring Market is positioned for sustained double-digit expansion through the end of the decade and beyond [4].

Transaction Monitoring Market — Key Report Takeaways

By Component

- Solutions accounted for 65.9% of the Transaction Monitoring Market in 2025, reflecting enterprise demand for end-to-end platforms that bundle case management, alert triage, and regulatory reporting.

- Services are expanding at a 19.6% CAGR through 2035 as institutions increasingly outsource model validation, tuning, and managed-detection operations to specialist providers.

By Deployment Mode

- Cloud deployment is growing at a 20.8% CAGR between 2026 and 2035, outpacing on-premises alternatives as banks pursue elastic scalability and lower infrastructure overhead.

By Application

- Anti-money laundering held a 38.5% revenue share in 2025, remaining the largest application category.

- Fraud detection and prevention is advancing at the fastest pace with a 22.3% CAGR to 2035, spurred by card-not-present fraud losses exceeding USD 10 Billion annually in the U.S. alone.

By Region

- North America led the Transaction Monitoring Market with a 30.4% share in 2025, underpinned by FinCEN enforcement actions and high banking technology adoption.

- Asia-Pacific records an 18.5% CAGR through 2035, supported by rapid UPI and e-wallet penetration across India, Indonesia, and the Philippines.

Transaction Monitoring Market — Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with compliance officers, vendor briefings, regulatory filings, and proprietary demand models calibrated against published benchmarks. Historical figures reflect actual vendor revenues and institutional spending disclosures; forecast values apply a compound growth trajectory informed by regulatory pipeline analysis and digital-payment volume projections.