Ultrasound Devices Market Summary

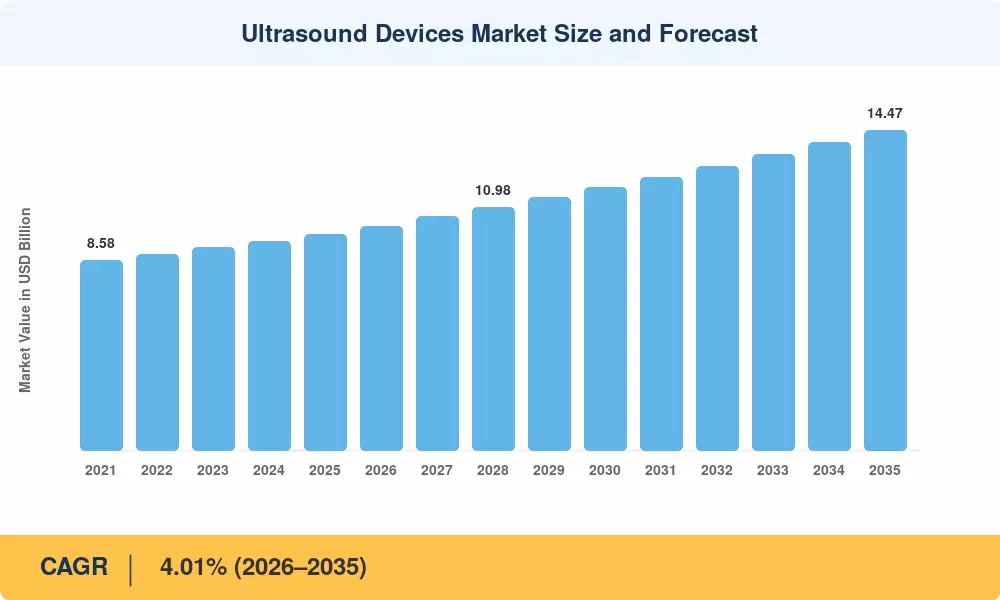

The Ultrasound Devices Market size was valued at USD 9.76 Billion in 2025, and the market is projected to grow from USD 10.15 Billion in 2026 to USD 14.47 Billion by 2035, registering a CAGR of 4.01% during the forecast period 2026–2035. Sustained clinical demand for radiation-free, real-time imaging continues to anchor growth, while national screening mandates — including expanded prenatal and cardiac programs funded under the U.S. Inflation Reduction Act and the EU4Health initiative — are channeling fresh capital into device procurement pipelines [1][2].

There is a clear shift in technology happening. Legacy cart-based AI-enabled 3D and 4D platforms are replacing 2D systems with automated measurements and quality rating. The extent of R&D commitment driving this change is shown by GE HealthCare’s more than USD 300 million investment in its Edison AI imaging ecosystem in 2024 [3]. Meanwhile, the downsizing of semiconductors has introduced probe-on-chip architectures into standard clinical processes, closing the price gap between handheld and traditional console devices.

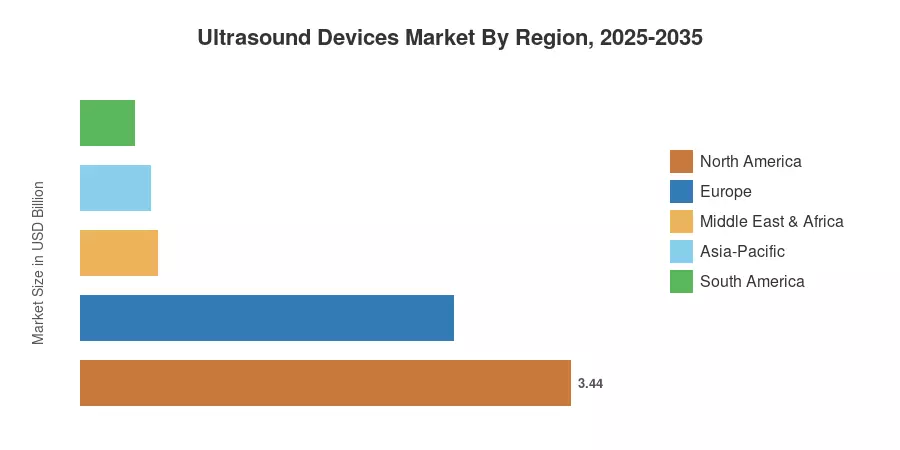

The North America region holds around 35.2% of the worldwide Ultrasound Devices market. The dense hospital infrastructure and good reimbursement regimes boost the market income. The fastest growth is in the Asia-Pacific area, at a CAGR of 5.03% through 2035, led by public-health digitization in India, China and Southeast Asia. Europe is the second largest with a share of roughly 26.8%, underpinned by aging populations and strong device replacement cycles. Those companies that combine AI-driven workflow automation with inexpensive portability will be rewarded in the next decade.

Key Report Takeaways

• By Technology

- 3D and 4D imaging platforms accounted for 48.1% of the Ultrasound Devices Market in 2025, driven by obstetric and musculoskeletal demand.

- High-intensity focused ultrasound (HIFU) is forecast to record the fastest segment CAGR of 5.38% through 2035, fueled by non-invasive oncology applications.

• By Application

- Radiology represented a 24.7% share of the Ultrasound Devices Market in 2025, reflecting broad-based screening volumes.

- Anesthesiology applications are poised to expand at a 5.13% CAGR to 2035, as nerve-block guidance becomes standard perioperative practice.

• By Geography

- North America led global revenue with a 35.2% share in 2025.

- Asia-Pacific is on track to grow at 5.03% CAGR, the highest among all regions, through 2035.

- Europe contributed approximately USD 2.62 billion in 2025, anchored by Germany, France, and the UK.

Ultrasound Devices Market Size and Forecast (2021–2035)

Market Research Future (MRFR) adopts a triangulated approach to estimate and forecast the market size. The MRFR triangulated approach combines the bottom-up device shipment tracking, top-down macroeconomic correlation, and primary interviews of procurement heads in 22 countries. Historical numbers (2021-2024) are based on reported revenue, while estimates (2026-2035) are based on segment-weighted growth assumptions and checked using hospital capital expenditure indexes.