Veterinary Surgical Instruments Market Summary

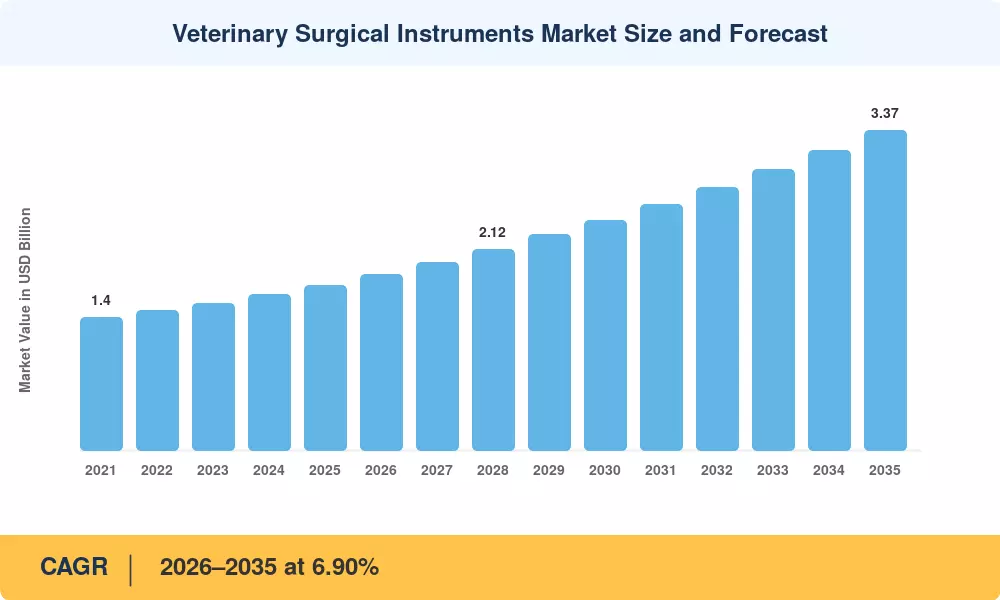

The Veterinary Surgical Instruments Market was valued at USD 1.74 Billion in 2025 and is projected to reach USD 1.85 Billion in 2026 before climbing to USD 3.37 Billion by 2035, expanding at a 6.90% CAGR during 2026–2035. Rising pet ownership rates across developed economies, combined with the widening scope of pet health insurance — now covering surgical procedures in over 40% of policies in the US and UK — are injecting sustained capital into the Veterinary Surgical Instruments Market [1]. Government livestock health programs, including the USDA's National Animal Health Monitoring System and the EU's Farm to Fork Strategy, are creating parallel demand channels for farm-animal surgical upgrades [2].

A technology shift is reshaping how veterinary clinics approach surgery. Legacy stainless-steel instrument sets, once considered lifetime purchases, are giving way to single-use sterilized kits and electrosurgical platforms with integrated smoke-evacuation systems. The global veterinary care services sector attracted over USD 7.2 Billion in private-equity investment between 2022 and 2024, accelerating equipment modernization cycles across corporate veterinary hospital chains [3]. High-definition endoscopic systems and AI-assisted surgical planning software are moving from university teaching hospitals into mid-tier referral practices, compressing adoption timelines that previously spanned a decade.

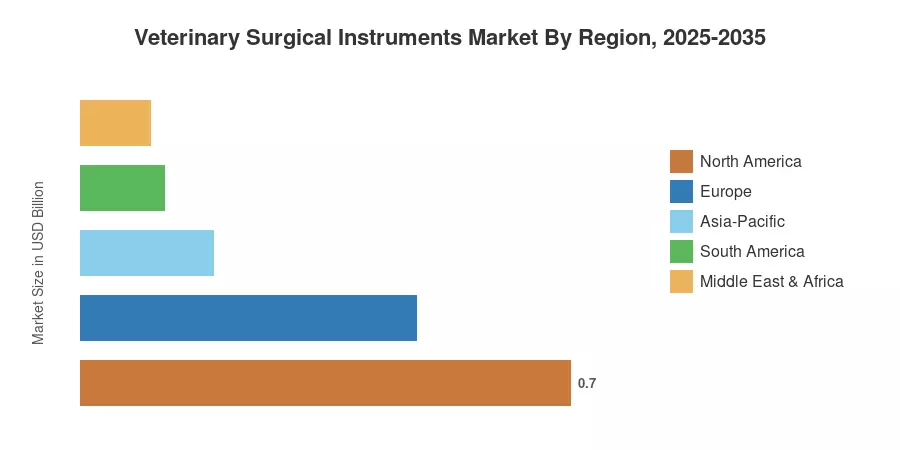

North America commands the largest share of the Veterinary Surgical Instruments Market at roughly 40.2% of 2025 revenue, anchored by mature companion-animal spending and a dense network of specialty referral centers. Asia-Pacific is the fastest-growing region, forecast to expand at a 10.80% CAGR through 2035, fueled by urbanization and government veterinary infrastructure investment across China and India. Europe holds the second-largest position with a 27.8% share, driven by stringent animal welfare mandates. The decade ahead will see precision-guided orthopedic procedures and tele-surgery platforms redefine Veterinary Surgical Instruments Market dynamics across all five regions.

Key Report Takeaways

• By Product

- Sutures and staplers accounted for a 35.5% revenue share in 2025, reflecting their universal use across virtually every surgical procedure type.

- Electrosurgery instruments are projected to grow at a 10.30% CAGR through 2035, outpacing every other product category in the Veterinary Surgical Instruments Market.

- Handheld instruments remain essential across all veterinary practice tiers, generating approximately USD 0.49 Billion in 2025 revenue.

• By Application

- Soft-tissue surgery held a 42.5% share of the Veterinary Surgical Instruments Market in 2025, driven by high-volume spay/neuter and tumor-removal caseloads.

- Orthopedic surgery is advancing at an 8.90% CAGR through 2035, propelled by custom implant adoption and aging pet populations.

• By Region

- North America generated 40.2% of 2025 revenue across the Veterinary Surgical Instruments Market.

- Asia-Pacific is forecast to grow at 10.80% CAGR to 2035, the highest of any region.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining top-down revenue analysis from manufacturer filings, bottom-up procedural volume models from veterinary associations, and cross-validation against distributor channel data. Historical figures (2021–2024) reflect actual reported values, while forecast projections (2026–2035) apply the calibrated 6.90% CAGR with adjustments for anticipated regulatory and technology inflection points.