Video Game Market Summary

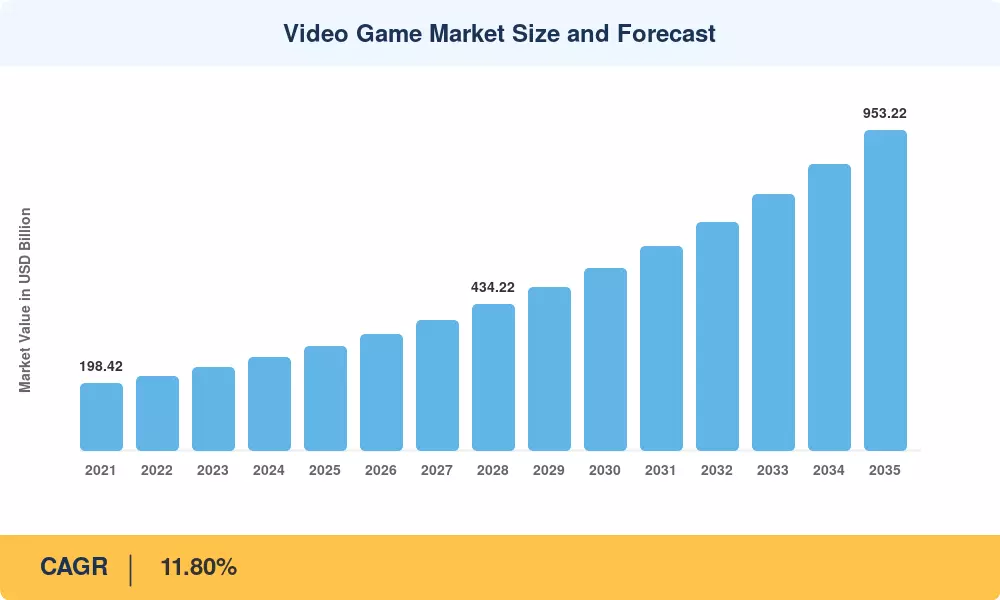

The Video Game Market was valued at USD 310.00 Billion in 2025 and is projected to grow from USD 349.30 Billion in 2026 to USD 953.22 Billion by 2035, registering a CAGR of 11.80% during the forecast period (2026–2035). This expansion sits on two pillars: the global rollout of 5G networks — with over 5.5 billion subscriptions expected by 2030 according to the GSMA [1] — and the pivot toward subscription-based distribution that is rewriting publisher economics. Government-led digital infrastructure programs in India's Bharat Net initiative and China's "East Data West Compute" project are widening addressable audiences in regions that previously lacked the bandwidth for high-fidelity streaming [2].

A generational technology shift is reshaping the Video Game Market from the inside out. Legacy retail-centric distribution has given way to cloud-native delivery, where titles stream directly to smartphones, smart TVs, and lightweight laptops without dedicated hardware. Generative-AI pipelines now compress asset-production timelines by 30–40%, allowing studios to maintain always-on live-service titles at a fraction of prior costs [3]. Microsoft's USD 68.7 billion acquisition of Activision Blizzard underscored how seriously platform holders view content as a service [4].

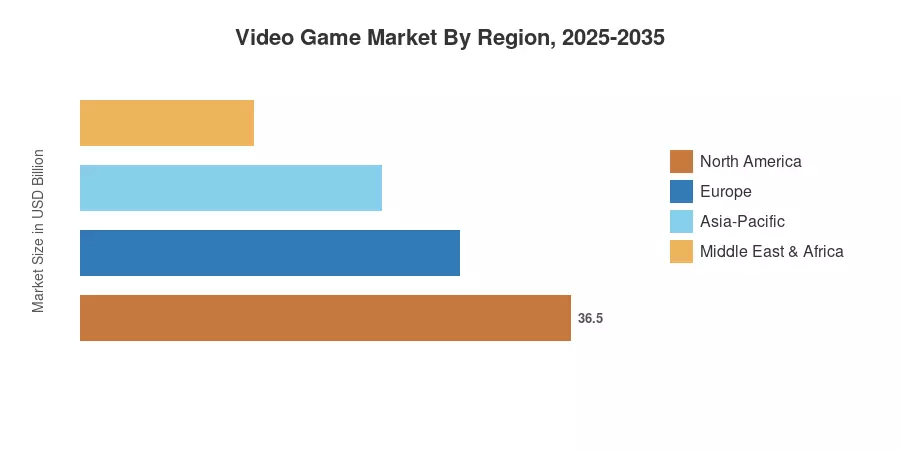

Asia-Pacific commands roughly 51.0% of the Video Game Market, anchored by China, Japan, and South Korea's mature ecosystems. The Middle East & Africa region is the fastest-growing at a 15.10% CAGR, fueled by youthful demographics and aggressive telecom investment in Saudi Arabia and the UAE. North America — accounting for approximately 24.5% of global revenue — remains the epicenter of AAA development and competitive esports viewership. As cloud infrastructure matures and cross-platform interoperability becomes standard, the Video Game Market is set to enter its most dynamic decade yet.

Key Report Takeaways

• By Device Type

- Mobile platforms captured the largest share of the Video Game Market in 2025, accounting for approximately 52.30% of total industry revenue.

- Cloud-gaming devices are forecast to expand at a 28.20% CAGR through 2035, the fastest rate of any device category.

• By Genre

- Action titles led genre-level revenue in 2025 with a 22.30% share of the Video Game Market.

• By Revenue Model

- Free-to-play models represented an estimated USD 186.98 Billion in 2025, dominating the revenue mix.

- Subscription-based platforms are rising at a 21.00% CAGR, reflecting a structural shift in how players access content.

• By End-User

- Casual gamers constituted roughly 63.20% of the 2025 player base.

- Professional esports athletes represent the fastest-growing end-user segment at an 18.80% CAGR.

• By Region

- Asia-Pacific dominated the Video Game Market with approximately 51.0% of 2025 revenue.

- The Middle East & Africa region is set to record the highest regional CAGR of 15.10% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines top-down revenue analysis from publicly listed publishers, bottom-line consumer-spending data from app-store intelligence platforms, and primary interviews with studio executives across 22 countries. Historical figures (2021–2024) are validated against financial disclosures; forecast figures (2026–2035) apply the calibrated 11.80% CAGR while accounting for cyclical hardware launches and regulatory headwinds.