Vinyl Ester Market Summary

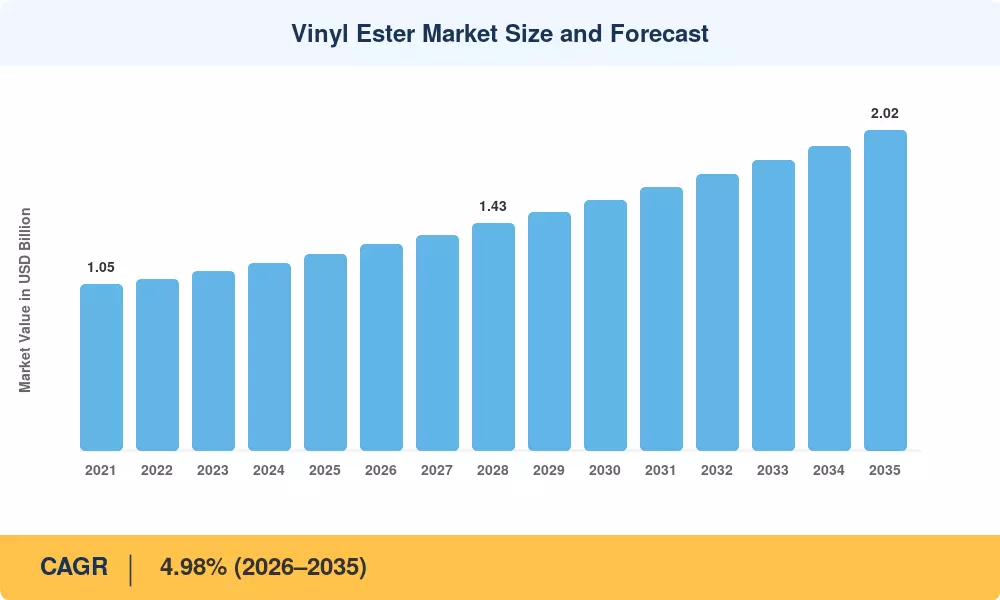

The global Vinyl Ester Market reached an estimated USD 1.24 Billion in 2025 and is projected to grow from USD 1.30 Billion in 2026 to USD 2.02 Billion by 2035, registering a CAGR of 4.98% during the forecast period. Accelerating demand from chemical processing, water treatment, and energy infrastructure is anchoring this expansion. Governments across Asia and North America have earmarked over USD 340 billion in combined infrastructure and industrial modernization programs between 2024 and 2030, creating a sustained pull for high-performance lining and structural materials [1][2].

A technical revolution is changing the way end customers specify their resin systems. The vinyl ester formulations are steadily gaining popularity over traditional polyester and isophthalic resins by providing better resistance against hydrolysis, chlorine attack and heat cycling. The U.S. Department of Energy’s 2024 Advanced Manufacturing Initiative dedicated USD 1.8 billion to next-generation process equipment, explicitly naming vinyl ester-lined containers as a benchmark technology for severe chemical conditions [3]. This tailwind is pushing specifiers and fabricators toward higher-performance Vinyl Ester Market product lines across numerous verticals.

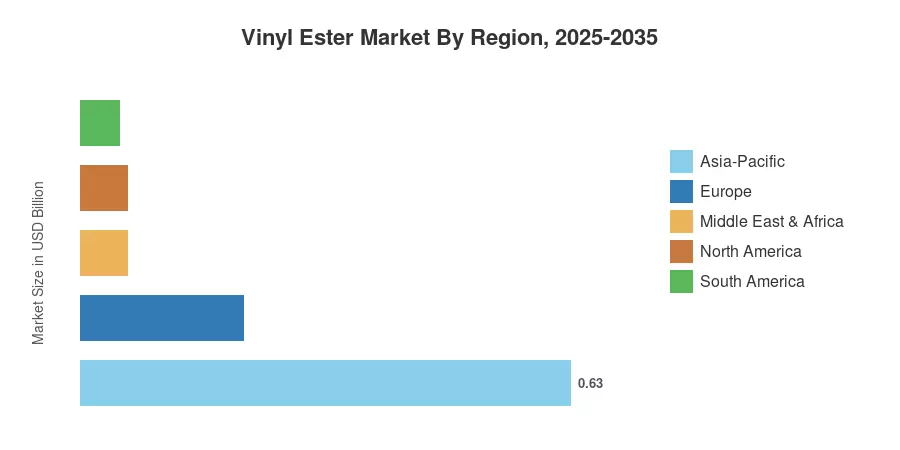

The Asia-Pacific region accounts for around 51% of the global Vinyl Ester Market revenue, as a result of fast-paced capacity build-outs in China, India and Southeast Asia. The region also has the highest CAGR of 5.20% until 2035. North America’s market share is roughly 22% due to refurbishment cycles in aged petrochemical and pulp-and-paper facilities, while Europe’s is around 17%, driven by offshore wind and wastewater infrastructure upgrades. Vinyl Ester Market set for a decade of compounding growth as regulatory standards tighten and asset owners desire longer service life.

Key Report Takeaways

• By Type

- DGEBA-based resins captured approximately 57% of the Vinyl Ester Market in 2025, reflecting broad adoption across corrosion-barrier and structural laminate applications.

- Epoxy Phenol Novolac (EPN) resins are expanding at a CAGR of 4.62%, gaining share in high-temperature chemical processing environments.

• By Application

- Pipes and tanks represented roughly 69% of the Vinyl Ester Market in 2025, underpinned by global water and wastewater capital programs.

- Paints and coatings applications are growing at a 4.45% CAGR as asset owners shift to longer-lasting protective systems.

• By Geography

- Asia-Pacific held the largest share of the Vinyl Ester Market and is projected to record a 5.20% CAGR through 2035.

- North America accounted for an estimated USD 0.27 Billion in 2025, led by U.S. chemical plant reinvestment.

Vinyl Ester Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a triangulated approach to estimate demand, combining bottom-up resin shipment numbers from trade bodies, top-down demand modeling from end-use verticals, and firsthand interviews with formulators and distributors. Industry association filings and customs data corroborate historical figures. Forecast Projections use the calibrated 4.98% CAGR with modifications for cyclical capex timing and raw material price corridors.

.webp?v=1784027963)