Watch Market Summary

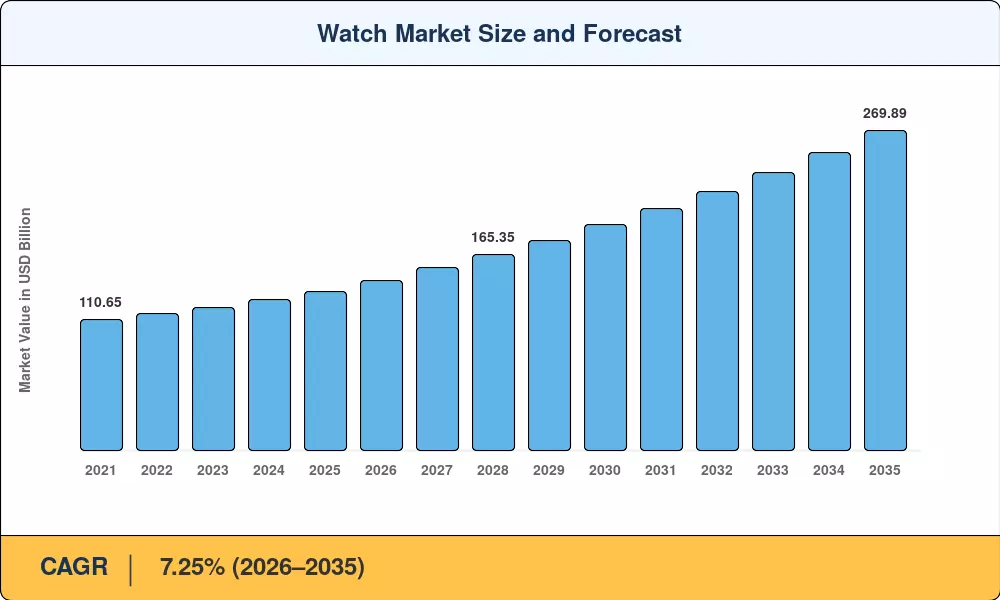

The global Watch Market stood at USD 134.10 Billion in 2025 and is projected to reach USD 143.75 Billion in 2026 before climbing to USD 269.89 Billion by 2035, expanding at a 7.25% CAGR across the 2026–2035 forecast window. This trajectory reflects an industry pushed forward by two simultaneous forces: consumers' enduring attachment to traditional horology and their accelerating appetite for connected wrist devices. Government-backed digitization agendas across Asia, coupled with rising luxury spending by the global middle class, have injected fresh capital into product development and retail infrastructure [1].

A significant transformation is reshaping how watches reach end users. Legacy wholesale models are giving way to direct-to-consumer platforms, while brands that once resisted digital integration are now embedding health-monitoring sensors and NFC payment modules into classic case designs. Global investment in wearable electronics surpassed USD 78 Billion in 2024, according to estimates, and a meaningful share of that capital flowed directly into the Watch Market [2].

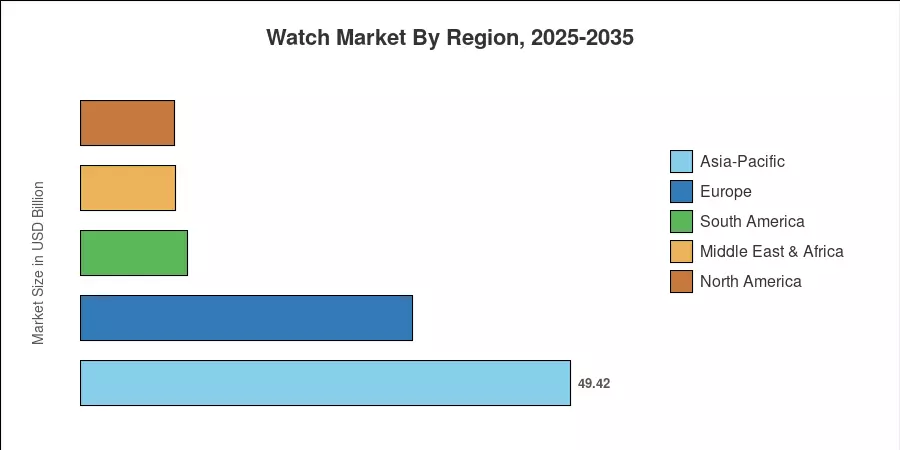

Asia-Pacific commands the largest regional footprint with 36.85% of 2025 revenue, driven by expanding urban populations in China, India, and Southeast Asia. South America represents the fastest-growing region, registering an anticipated 8.05% CAGR through 2035, while Europe holds the second-largest share at roughly 25% of global sales, anchored by Switzerland's manufacturing ecosystem and strong domestic demand in Germany, France, and the UK.

Key Report Takeaways

• By Product Type

- Quartz and mechanical lines captured 63.15% of the Watch Market in 2025, underscoring sustained consumer preference for analog timepieces.

- Digital watches are on course to record the fastest segment CAGR of 7.68% through 2035, fueled by fitness tracking and smart connectivity features.

• By Category

- The mass-tier segment accounted for 64.85% of 2025 Watch Market sales, reflecting broad affordability across emerging economies.

- Premium-category watches are projected to expand at a 7.25% CAGR to 2035 as luxury consumption rises in Asia and the Middle East.

• By End User

- Men's models represented the largest share at 37.35% of Watch Market revenue in 2025.

- Unisex designs are poised for the fastest growth at a 7.95% CAGR, reflecting shifting consumer attitudes toward gender-neutral accessories.

• By Distribution Channel

- Specialty stores retained 51.75% of the 2025 Watch Market revenue through curated in-store experiences.

- Online retail channels are forecast to grow at a 9.35% CAGR, the highest among all distribution segments.

• By Region

- Asia-Pacific led the Watch Market with 36.85% of 2025 sales.

- South America is expected to register the quickest regional CAGR of 8.05% through 2035.

Watch Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining primary interviews with watch brand executives, distributors, and component suppliers alongside secondary data from trade associations, customs databases, and published financials. Historical figures (2021–2024) are validated against Federation of the Swiss Watch Industry export data and Euromonitor retail audits[4]. Forecast projections apply regression-adjusted demand models calibrated to macroeconomic indicators, including GDP per capita growth, urbanization rates, and consumer confidence indices.