Luxury Watch Market Summary

The Luxury Watch Market was valued at USD 85.07 Billion in 2025 and is projected to reach USD 90.29 Billion in 2026 before climbing to USD 152.38 Billion by 2035, registering a CAGR of 5.68% during the forecast period (2026–2035). Rising disposable incomes across Asia-Pacific economies and renewed appetite for Swiss mechanical luxury watches among younger demographics are anchoring this growth trajectory. Government-backed trade facilitation programs in key export corridors — particularly Switzerland's bilateral agreements with China and India — have reduced tariff friction on high horology and complications timepieces by roughly 4–6% since 2022 [1].

A quiet revolution in materials science is reshaping the Luxury Watch Market from the inside out. Brands are replacing conventional stainless steel cases with forged carbon composites, ceramic alloys, and recycled titanium — Panerai's Ecotitanium initiative alone has diverted an estimated 30 metric tons of aerospace-grade titanium into watch production since 2023 [2]. Tourbillon and chronograph watches now integrate silicon escapements and graphene hairsprings, extending power reserves beyond 120 hours and eliminating the need for periodic servicing that once deterred first-time collectors. Investment in watchmaking R&D across the top ten Maisons exceeded USD 1.8 Billion cumulatively between 2022 and 2025.

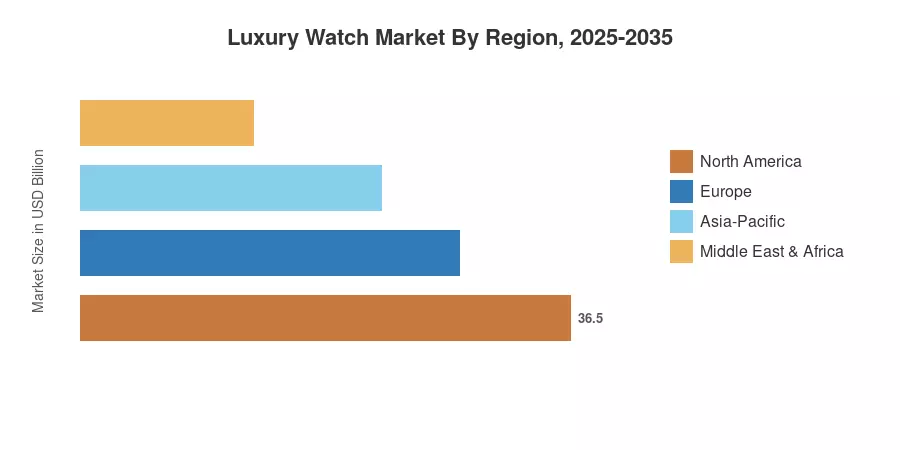

Asia-Pacific commands an estimated 38.5% share of the Luxury Watch Market, powered by surging demand in China, Japan, and South Korea. South America is the fastest-growing region, with a projected CAGR of 7.28% through 2035, fueled by expanding luxury retail infrastructure in Brazil and Argentina. Europe holds the second-largest share at roughly 27%, anchored by Switzerland's manufacturing base and robust domestic consumption in Germany, France, and Italy The next decade will see luxury watch investment value become a mainstream asset-class conversation as authenticated resale platforms scale globally.

Key Report Takeaways

• By Product Type

- Quartz/mechanical watches captured approximately 59% of the Luxury Watch Market in 2025, driven by enduring collector demand for Swiss mechanical luxury watches with hand-finished movements

- Digital watches are forecast to post a CAGR of 5.97% through 2035, supported by hybrid smartwatch designs that blend high horology and complications with connected functionality

• By End User

- Men accounted for USD 46.54 Billion in Luxury Watch Market revenue during 2025, reflecting strong demand for tourbillon and chronograph watches across traditional buyer segments

- Women's luxury watch lines are projected to expand at a 6.22% CAGR to 2035, as brands like Cartier, Chopard, and Audemars Piguet invest in gem-set and complication-driven women's collections

- Unisex timepieces are gaining traction, with an estimated 4.8% CAGR, reflecting shifting gender norms in luxury watch auction and resale channels

• By Region

- Asia-Pacific led the Luxury Watch Market with a 38.5% share in 2025

- South America is projected to register the highest CAGR at 7.28% through 2035, driven by rising middle-class affluence and luxury watch investment value awareness

- North America contributed approximately USD 17.86 Billion in 2025 revenue

Market Size and Forecast (2021–2035)

MRFR’s market sizing methodology triangulates top-down revenue projections from the luxury conglomerates (LVMH, Richemont, Swatch Group) with bottom-up demand modeling across 42 geographic markets. Historical data is collected from the Swiss Watch Industry Federation export figures, national customs databases and proprietary retail audit panels [4].