Luxury Goods Market Summary

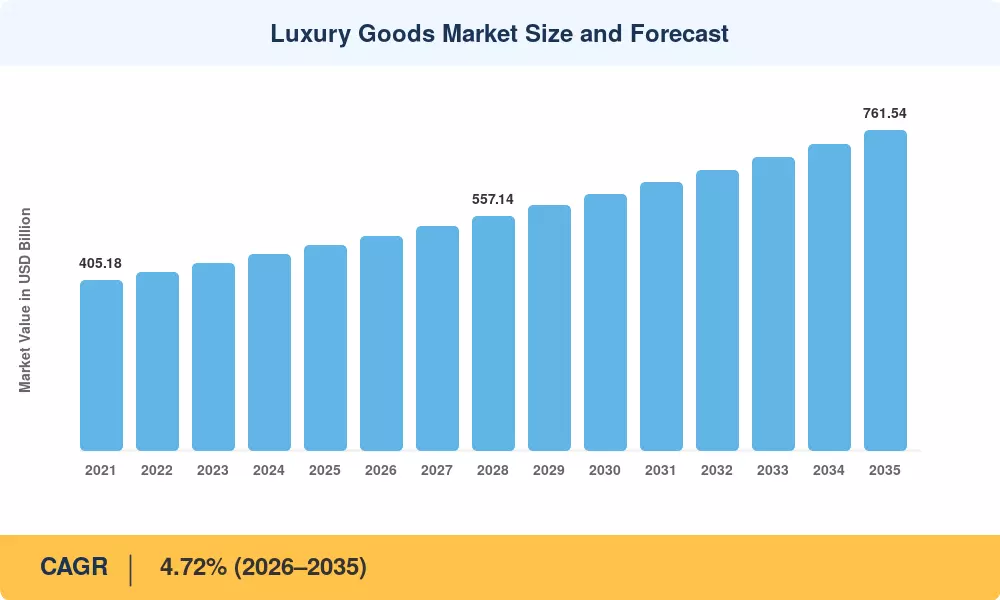

The global Luxury Goods Market was valued at USD 487.30 billion in 2025 and is projected to reach USD 510.04 billion in 2026, climbing to USD 761.54 billion by 2035 at a CAGR of 4.72% during 2026–2035. Rising affluent consumer spending across developed and emerging economies, combined with the enduring appeal of exclusive luxury brand heritage, continues to anchor this expansion. A wave of high-net-worth household formation in Asia and the Middle East has injected fresh capital into ultra-premium branded products, while European maisons are reinvesting record profits into flagship retail experiences.

Digital transformation is reshaping how consumers discover and purchase luxury leather goods and jewelry. Legacy wholesale distribution is giving way to brand-owned e-commerce ecosystems, virtual try-on technologies, and AI-curated clienteling platforms. LVMH alone allocated over EUR 1.2 billion toward digital infrastructure between 2023 and 2025, signaling the sector's commitment to omnichannel integration. Social commerce channels — particularly in China and Southeast Asia — now influence more than 40% of first-time luxury purchases among consumers under 35.

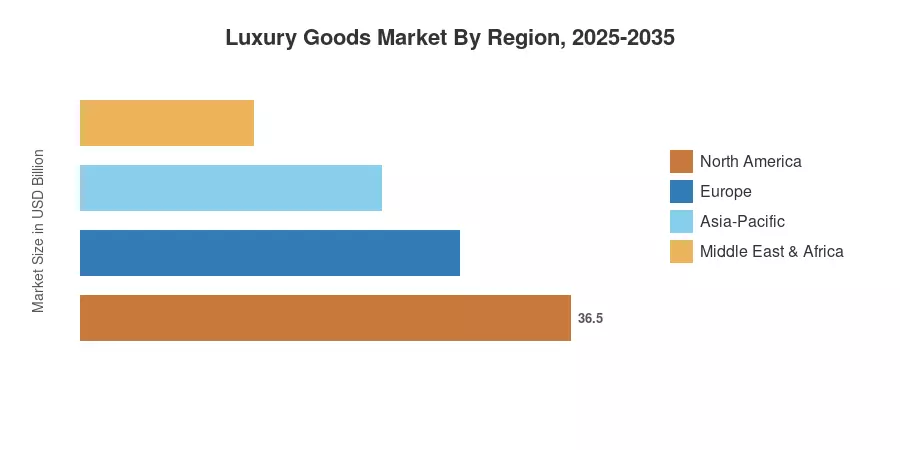

Europe commands the largest share of the Luxury Goods Market at roughly 48.4% of 2025 revenue, anchored by France, Italy, and the tourism-driven Swiss watch corridor. Asia-Pacific is the fastest-growing region with a projected CAGR of 5.89%, propelled by a surging affluent middle class in China, India, and South Korea. North America remains the second-largest region, accounting for approximately USD 112.10 billion in 2025 sales, driven by resilient demand for high-end fashion and accessories among Gen-Z and millennial cohorts The next decade will likely see the balance of luxury spending tilt further eastward as aspirational consumption accelerates across emerging Asia [5].

Key Report Takeaways

• By Product Type

- Clothing and apparel captured a 34.17% share of the Luxury Goods Market in 2025, reflecting enduring demand for seasonal collections and couture

- Watches are forecast to register the fastest CAGR of 4.78% through 2035, driven by investment-grade timepiece acquisition

- Footwear generated approximately USD 72.60 billion in 2025, buoyed by sneaker culture crossovers into luxury leather goods and jewelry categories

• By End User

- Women accounted for 52.18% of Luxury Goods Market purchases in 2025, sustaining their role as the primary buyer demographic

- Male consumers are projected to grow at a 5.12% CAGR, supported by expanding menswear and grooming segments featuring ultra-premium branded products

• By Distribution Channel

- Single-brand stores held 35.40% of 2025 revenue across the Luxury Goods Market, reinforcing the importance of exclusive luxury brand heritage in retail environments

- Online stores are anticipated to achieve the highest CAGR of 5.48% to 2035 as affluent consumer spending migrates to digital platforms

• By Region

- Europe contributed 48.40% of global Luxury Goods Market sales in 2025

- Asia-Pacific is positioned to accelerate at a 5.89% CAGR through 2035, led by China and India

Luxury Goods Market Size and Forecast (2021–2035)

Market Research Future employs a hybrid bottom-up and top-down sizing methodology, triangulating brand-level revenue disclosures, trade association data, customs-level import/export flows, and consumer panel surveys. Historical figures (2021–2024) reflect audited performance, while the 2025 base year integrates preliminary filings and channel-check data. Forecast values (2026–2035) are derived from MRFR's proprietary CAGR model, validated against macroeconomic indicators including GDP per capita growth, luxury price inflation indices, and tourism arrival projections[6].