Germany Luxury Goods Market Summary

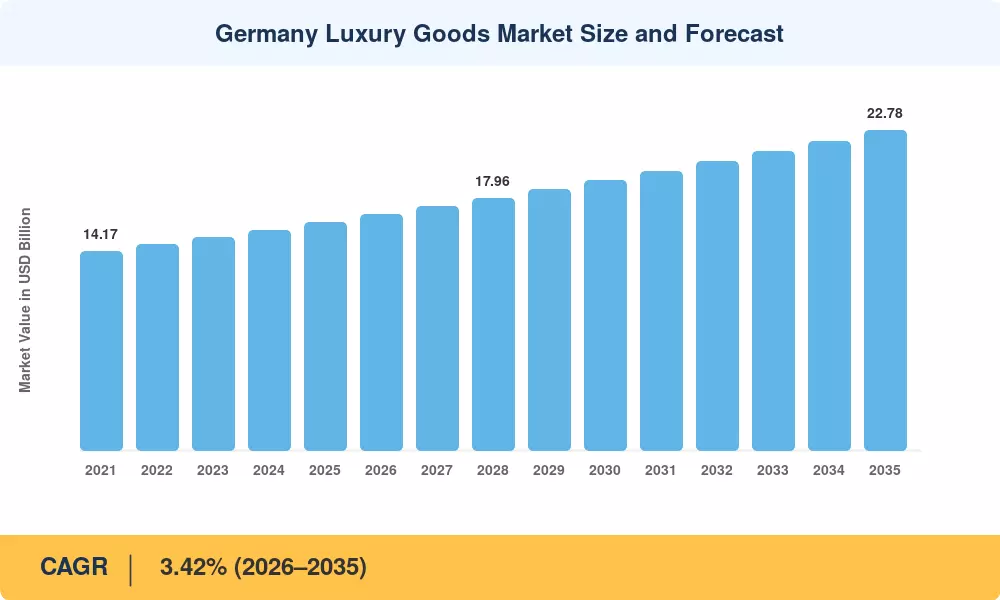

The Germany Luxury Goods Market stood at USD 16.22 billion in 2025 and is projected to reach USD 16.83 billion in 2026 before climbing to USD 22.78 billion by 2035, expanding at a 3.42% CAGR over the 2026–2035 forecast window. Germany's resilient consumer economy, bolstered by strong disposable income levels and a cultural appreciation for craftsmanship, continues to anchor demand. The Federal Ministry for Economic Affairs reported that consumer confidence in premium segments recovered to pre-pandemic levels by late 2024, with luxury retail sales in Munich, Berlin, and Düsseldorf rising 4.1% year-over-year [2]. This trajectory positions the Germany Luxury Goods Market as a bellwether for broader European premium consumption.

A transformation is underway in how luxury fashion accessories Germany retailers engage buyers. Legacy brick-and-mortar mono-brand stores are ceding ground to omnichannel platforms that blend immersive in-store experiences with digital concierge services. Brands such as Hugo Boss and MCM have invested over EUR 200 million collectively in digital infrastructure since 2022, integrating AI-driven personalization engines and virtual try-on technology [3]. Sustainability certifications — particularly the EU Digital Product Passport regulation effective 2027 — are reshaping supply chains for every German premium luxury brand competing in leather goods and apparel.

Europe dominates the Germany Luxury Goods Market with a natural 100% share given the single-country scope, though the report benchmarks Germany against its continental peers. Within Germany, the southern states of Bavaria and Baden-Württemberg account for roughly 38% of luxury retail Germany trend spending, driven by higher per-capita wealth and tourism inflows. The German luxury auto market continues to reinforce brand prestige through cross-category halo effects, with Porsche and BMW lifestyle divisions expanding into fashion and accessories. Looking ahead, digital-first millennials and Gen Z consumers will redefine the competitive playbook through 2035

Key Report Takeaways

• By Product Type

- Clothing and apparel captured 44.6% of the Germany Luxury Goods Market in 2025, underscoring the dominance of luxury fashion accessories Germany demand among domestic and tourist shoppers

- The watches segment is forecast to advance at a 3.61% CAGR through 2035 as high-end watch jewelry Germany demand pivots toward limited-edition mechanical timepieces

- Footwear revenues in the Germany Luxury Goods Market exceeded USD 2.1 billion in 2025, driven by sneaker-luxury crossovers and artisan leather craftsmanship

• By End User

- Women represented 57.2% of the Germany Luxury Goods Market by value in 2025, reflecting entrenched spending on handbags, couture, and fine jewelry

- The men's segment is set to grow at a 4.01% CAGR to 2035 as German premium luxury brand houses expand tailored menswear and grooming lines

• By Distribution Channel

- Single brand stores held 40.1% of Germany Luxury Goods Market revenue in 2025, anchored by flagship locations on Berlin's Kurfürstendamm and Munich's Maximilianstraße

- Online stores are advancing at a 4.48% CAGR as digital luxury retail Germany trend adoption accelerates among younger demographics

Market Size and Forecast (2021–2035)

The market size trajectory below is derived from MRFR's proprietary demand modeling, incorporating macroeconomic indicators (GDP per capita, Gini coefficient, tourism receipts), brand-level sell-through data, and consumer survey panels across Germany's top 15 metropolitan areas.

.webp?v=1783326299)