Wearable Medical Device Market Summary

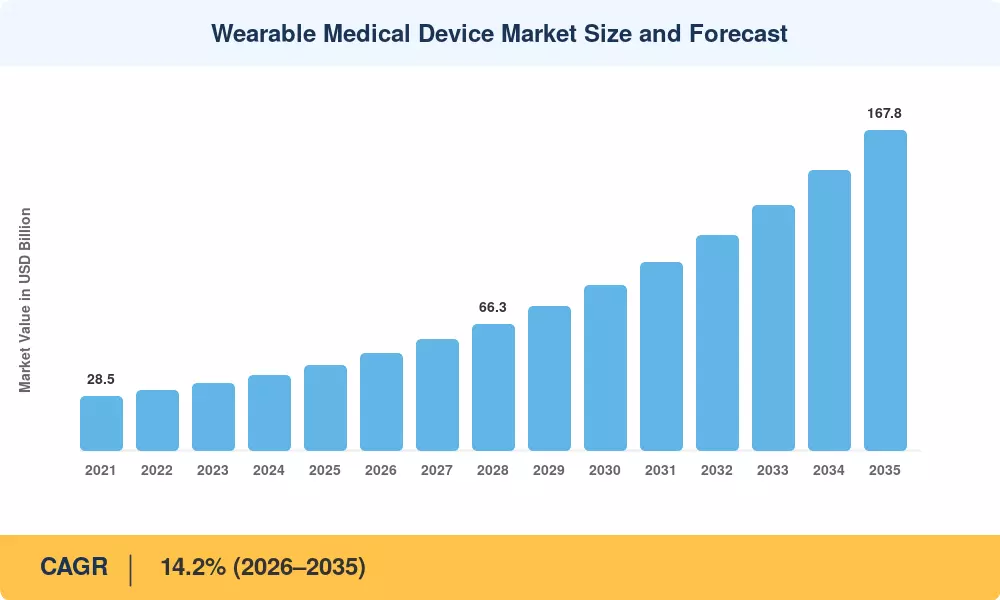

The Wearable Medical Device Market reached an estimated USD 44.5 billion in 2025 and is projected to climb from USD 50.8 billion in 2026 to USD 167.8 billion by 2035, registering a CAGR of 14.2% across the forecast window. Two catalysts are accelerating this trajectory: the U.S. Centers for Medicare & Medicaid Services expanded remote-monitoring reimbursement codes in 2024, unlocking an incremental USD 3.8 billion in annual billable services, while the European Commission's Digital Health Strategy earmarked EUR 1.3 billion for connected-diagnostics infrastructure through 2028 [1][2].

A technology shift is reshaping clinical workflows. Legacy spot-check devices — pulse oximeters used once per hospital shift, periodic blood-pressure cuffs — are giving way to continuous, multi-parameter wearables that stream data to cloud dashboards in real time. Apple's FDA-cleared ECG module, Abbott's FreeStyle Libre continuous glucose monitor, and Dexcom's G7 platform illustrate how consumer-grade form factors now deliver clinical-grade accuracy, a convergence that drew over USD 6.2 billion in venture and strategic investment during 2023–2024 alone [3][4].

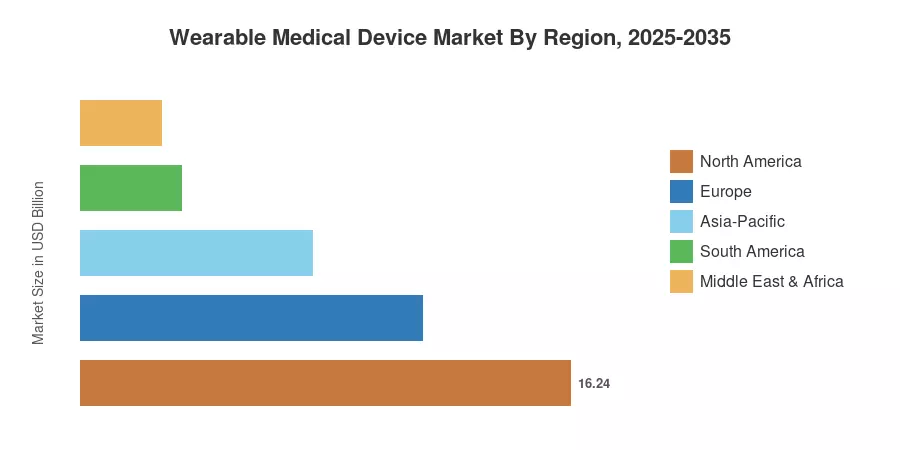

North America held a 36.5% share of the Wearable Medical Device Market in 2025, underpinned by advanced payer ecosystems and dense hospital IT networks. Asia-Pacific ranks as the fastest-growing region with a projected 17.3% CAGR through 2035, powered by government digitization campaigns in India, China, and Japan. Europe captured the second-largest share at 25.5%, anchored by MDR-compliant product launches and aging-population demand. As reimbursement pathways mature and sensor costs decline, the Wearable Medical Device Market is poised for sustained double-digit expansion across every major geography.

Key Report Takeaways

• By Device Type

- Diagnostic and monitoring devices commanded 67.5% of the Wearable Medical Device Market in 2025, driven by continuous glucose monitors and multi-lead ECG patches.

- Therapeutic devices are expected to grow at a 17.0% CAGR through 2035, reflecting rising adoption of insulin-delivery wearables and neurostimulation patches.

• By Application & End User

- Home healthcare retained 55.4% of the Wearable Medical Device Market share in 2025, fueled by payer incentives for post-discharge monitoring.

• By End User

- Consumer end users accounted for 58.9% of revenue in 2025, although hospital procurement is accelerating under updated reimbursement frameworks.

• By Region

- North America led the Wearable Medical Device Market with a 36.5% revenue share in 2025.

- Asia-Pacific is forecast to register a 17.3% CAGR through 2035, the highest among all regions.

- Europe contributed 25.5% of global revenue, with Germany and the UK anchoring adoption.

Wearable Medical Device Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up revenue aggregation from 120+ device manufacturers, top-down validation against payer-claims databases, and demand-side calibration through 450+ primary interviews with procurement officers, clinicians, and channel partners.