-

. EXECUTIVE SUMMARY

-

. Market Overview

-

. Key Findings

-

. Market Segmentation

-

. Competitive Landscape

-

. Challenges and Opportunities

-

. Future Outlook

-

. MARKET INTRODUCTION

-

. Definition

-

. Scope of the study

-

. Research Objective

-

. Assumption

-

. Limitations

-

. RESEARCH METHODOLOGY

-

. Overview

-

. Data Mining

-

. Secondary Research

-

. Primary Research

-

. Primary Interviews and Information Gathering Process

-

. Breakdown of Primary Respondents

-

. Forecasting Model

-

. Market Size Estimation

-

. Bottom-Up Approach

-

. Top-Down Approach

-

. Data Triangulation

-

. Validation

-

. MARKET DYNAMICS

-

. Overview

-

. Drivers

-

. Restraints

-

. Opportunities

-

. MARKET FACTOR ANALYSIS

-

. Value chain Analysis

-

. Porter's Five Forces Analysis

-

. Bargaining Power of Suppliers

-

. Bargaining Power of Buyers

-

. Threat of New Entrants

-

. Threat of Substitutes

-

. Intensity of Rivalry

-

. COVID-19 Impact Analysis

-

. Market Impact Analysis

-

. Regional Impact

-

. Opportunity and Threat Analysis

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY (USD BILLION)

-

. Computed Radiography

-

. Direct Digital Radiography

-

. Digital Fluoroscopy

-

. Mobile Digital Radiography

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION (USD BILLION)

-

. Orthopedics

-

. Cardiology

-

. Dentistry

-

. Oncology

-

. Pediatrics

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE (USD BILLION)

-

. Hospitals

-

. Diagnostic Imaging Centers

-

. Research Institutions

-

. Outpatient Clinics

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE (USD BILLION)

-

. X-ray Devices

-

. CT Scanners

-

. MRI Devices

-

. Ultrasound Devices

-

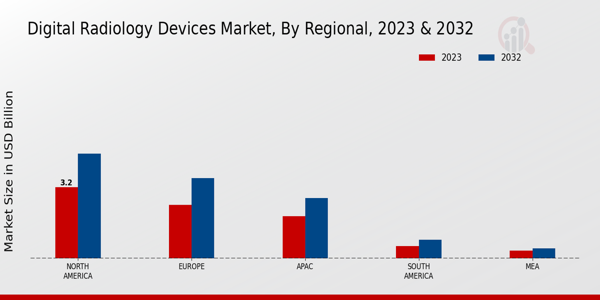

. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL (USD BILLION)

-

. North America

-

. US

-

. Canada

-

. Europe

-

. Germany

-

. UK

-

. France

-

. Russia

-

. Italy

-

. Spain

-

. Rest of Europe

-

. APAC

-

. China

-

. India

-

. Japan

-

. South Korea

-

. Malaysia

-

. Thailand

-

. Indonesia

-

. Rest of APAC

-

. South America

-

. Brazil

-

. Mexico

-

. Argentina

-

. Rest of South America

-

. MEA

-

. GCC Countries

-

. South Africa

-

. Rest of MEA

-

. COMPETITIVE LANDSCAPE

-

. Overview

-

. Competitive Analysis

-

. Market share Analysis

-

. Major Growth Strategy in the Digital Radiology Devices Market

-

. Competitive Benchmarking

-

. Leading Players in Terms of Number of Developments in the Digital Radiology Devices Market

-

. Key developments and growth strategies

-

. New Product Launch/Service Deployment

-

. Merger & Acquisitions

-

. Joint Ventures

-

. Major Players Financial Matrix

-

. Sales and Operating Income

-

. Major Players R&D Expenditure. 2023

-

. COMPANY PROFILES

-

. Siemens Healthineers

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Canon Medical Systems

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. GE Healthcare

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Elekta

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Fujifilm Holdings

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Philips Healthcare

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Hitachi Medical Corporation

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Mindray

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Samsung Medison

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. AgfaGevaert Group

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Hologic

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Nikon

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Carestream Health

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Konica Minolta

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. Varian Medical Systems

-

. Financial Overview

-

. Products Offered

-

. Key Developments

-

. SWOT Analysis

-

. Key Strategies

-

. APPENDIX

-

. References

-

. Related Reports LIST OF TABLES TABLE

-

. LIST OF ASSUMPTIONS TABLE

-

. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. US DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. US DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. US DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. US DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. US DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY APPLICATION, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY END USE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2032 (USD BILLIONS) TABLE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2032 (USD BILLIONS) TABLE

-

. PRODUCT LAUNCH/PRODUCT DEVELOPMENT/APPROVAL TABLE

-

. ACQUISITION/PARTNERSHIP LIST OF FIGURES FIGURE

-

. MARKET SYNOPSIS FIGURE

-

. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE

-

. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE

-

. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE

-

. KEY BUYING CRITERIA OF DIGITAL RADIOLOGY DEVICES MARKET FIGURE

-

. RESEARCH PROCESS OF MRFR FIGURE

-

. DRO ANALYSIS OF DIGITAL RADIOLOGY DEVICES MARKET FIGURE

-

. DRIVERS IMPACT ANALYSIS: DIGITAL RADIOLOGY DEVICES MARKET FIGURE

-

. RESTRAINTS IMPACT ANALYSIS: DIGITAL RADIOLOGY DEVICES MARKET FIGURE

-

. SUPPLY / VALUE CHAIN: DIGITAL RADIOLOGY DEVICES MARKET FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY, 2024 (% SHARE) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY, 2019 TO 2032 (USD Billions) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION, 2024 (% SHARE) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION, 2019 TO 2032 (USD Billions) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE, 2024 (% SHARE) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE, 2019 TO 2032 (USD Billions) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE, 2024 (% SHARE) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE, 2019 TO 2032 (USD Billions) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL, 2024 (% SHARE) FIGURE

-

. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL, 2019 TO 2032 (USD Billions) FIGURE

-

. BENCHMARKING OF MAJOR COMPETITORS

-

List of Tables and Figures

-

Table FIGURE 1. MARKET SYNOPSIS FIGURE 2. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 3. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 4. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 5. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 6. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 7. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 8. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 9. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 10. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 11. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 12. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 13. EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 14. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 15. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 16. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 17. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 18. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 19. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 20. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 21. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 22. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 23. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 24. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 25. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 26. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 27. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 28. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 29. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 30. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 31. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 32. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 33. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 34. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 35. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 36. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 37. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 38. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 39. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 40. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 41. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 42. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 43. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 44. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 45. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 46. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 47. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 48. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 49. APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 50. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 51. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 52. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 53. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 54. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 55. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 56. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 57. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 58. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 59. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 60. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 61. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 62. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 63. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 64. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 65. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 66. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 67. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 68. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 69. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 70. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 71. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 72. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 73. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 74. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 75. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 76. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 77. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 78. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 79. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 80. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 81. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 82. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 83. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 84. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 85. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 86. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 87. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 88. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 89. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 90. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 91. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 92. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 93. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 94. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 95. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 96. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 97. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 98. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 99. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 100. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 101. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 102. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 103. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 104. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 105. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 106. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 107. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 108. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 109. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 110. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 111. MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 112. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 113. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 114. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 115. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 116. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 117. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 118. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 119. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 120. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 121. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 122. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 123. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 124. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 125. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 126. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 127. KEY BUYING CRITERIA OF DIGITAL RADIOLOGY DEVICES MARKET FIGURE 128. RESEARCH PROCESS OF MRFR FIGURE 129. DRO ANALYSIS OF DIGITAL RADIOLOGY DEVICES MARKET FIGURE 130. DRIVERS IMPACT ANALYSIS: DIGITAL RADIOLOGY DEVICES MARKET FIGURE 131. RESTRAINTS IMPACT ANALYSIS: DIGITAL RADIOLOGY DEVICES MARKET FIGURE 132. SUPPLY / VALUE CHAIN: DIGITAL RADIOLOGY DEVICES MARKET FIGURE 133. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY, 2024 (% SHARE) FIGURE 134. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY, 2019 TO 2032 (USD Billions) FIGURE 135. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION, 2024 (% SHARE) FIGURE 136. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION, 2019 TO 2032 (USD Billions) FIGURE 137. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE, 2024 (% SHARE) FIGURE 138. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE, 2019 TO 2032 (USD Billions) FIGURE 139. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE, 2024 (% SHARE) FIGURE 140. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE, 2019 TO 2032 (USD Billions) FIGURE 141. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL, 2024 (% SHARE) FIGURE 142. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL, 2019 TO 2032 (USD Billions) FIGURE 143. BENCHMARKING OF MAJOR COMPETITORS

-

Table FIGURE 1. MARKET SYNOPSIS FIGURE 2. NORTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 3. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 4. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 5. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 6. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 7. US DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 8. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 9. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 10. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 11. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 12. CANADA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 13. EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 14. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 15. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 16. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 17. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 18. GERMANY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 19. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 20. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 21. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 22. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 23. UK DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 24. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 25. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 26. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 27. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 28. FRANCE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 29. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 30. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 31. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 32. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 33. RUSSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 34. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 35. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 36. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 37. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 38. ITALY DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 39. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 40. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 41. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 42. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 43. SPAIN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 44. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 45. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 46. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 47. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 48. REST OF EUROPE DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 49. APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 50. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 51. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 52. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 53. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 54. CHINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 55. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 56. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 57. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 58. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 59. INDIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 60. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 61. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 62. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 63. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 64. JAPAN DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 65. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 66. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 67. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 68. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 69. SOUTH KOREA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 70. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 71. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 72. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 73. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 74. MALAYSIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 75. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 76. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 77. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 78. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 79. THAILAND DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 80. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 81. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 82. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 83. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 84. INDONESIA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 85. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 86. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 87. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 88. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 89. REST OF APAC DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 90. SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 91. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 92. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 93. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 94. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 95. BRAZIL DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 96. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 97. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 98. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 99. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 100. MEXICO DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 101. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 102. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 103. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 104. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 105. ARGENTINA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 106. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 107. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 108. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 109. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 110. REST OF SOUTH AMERICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 111. MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS FIGURE 112. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 113. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 114. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 115. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 116. GCC COUNTRIES DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 117. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 118. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 119. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 120. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 121. SOUTH AFRICA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 122. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY TECHNOLOGY FIGURE 123. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY APPLICATION FIGURE 124. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY END USE FIGURE 125. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY PRODUCT TYPE FIGURE 126. REST OF MEA DIGITAL RADIOLOGY DEVICES MARKET ANALYSIS BY REGIONAL FIGURE 127. KEY BUYING CRITERIA OF DIGITAL RADIOLOGY DEVICES MARKET FIGURE 128. RESEARCH PROCESS OF MRFR FIGURE 129. DRO ANALYSIS OF DIGITAL RADIOLOGY DEVICES MARKET FIGURE 130. DRIVERS IMPACT ANALYSIS: DIGITAL RADIOLOGY DEVICES MARKET FIGURE 131. RESTRAINTS IMPACT ANALYSIS: DIGITAL RADIOLOGY DEVICES MARKET FIGURE 132. SUPPLY / VALUE CHAIN: DIGITAL RADIOLOGY DEVICES MARKET FIGURE 133. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY, 2024 (% SHARE) FIGURE 134. DIGITAL RADIOLOGY DEVICES MARKET, BY TECHNOLOGY, 2019 TO 2032 (USD Billions) FIGURE 135. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION, 2024 (% SHARE) FIGURE 136. DIGITAL RADIOLOGY DEVICES MARKET, BY APPLICATION, 2019 TO 2032 (USD Billions) FIGURE 137. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE, 2024 (% SHARE) FIGURE 138. DIGITAL RADIOLOGY DEVICES MARKET, BY END USE, 2019 TO 2032 (USD Billions) FIGURE 139. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE, 2024 (% SHARE) FIGURE 140. DIGITAL RADIOLOGY DEVICES MARKET, BY PRODUCT TYPE, 2019 TO 2032 (USD Billions) FIGURE 141. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL, 2024 (% SHARE) FIGURE 142. DIGITAL RADIOLOGY DEVICES MARKET, BY REGIONAL, 2019 TO 2032 (USD Billions) FIGURE 143. BENCHMARKING OF MAJOR COMPETITORS

Leave a Comment