-

FACTOR ANALYSIS

-

\r\n\r\n\r\nValue chain Analysis

-

\r\n\r\n\r\nPorter's

-

Five Forces Analysis

-

\r\n\r\n\r\nBargaining Power of Suppliers

-

\r\n\r\n\r\nBargaining

-

Power of Buyers

-

\r\n\r\n\r\nThreat of New Entrants

-

\r\n\r\n\r\nThreat

-

of Substitutes

-

\r\n\r\n\r\nIntensity of Rivalry

-

\r\n\r\n\r\n\r\n\r\nCOVID-19

-

Impact Analysis

-

\r\n\r\n\r\nMarket Impact Analysis

-

\r\n\r\n\r\nRegional

-

Impact

-

\r\n\r\n\r\nOpportunity and Threat Analysis

-

\r\n\r\n\r\n\r\n\r\n\r\n\r\n\r\n\r\nHIV

-

Diagnostics Market, BY Test Type (USD Billion)

-

\r\n\r\n\r\nAntibody

-

Tests

-

\r\n\r\n\r\nAntigen Tests

-

\r\n\r\n\r\nNucleic

-

Acid Tests

-

\r\n\r\n\r\n\r\n\r\nHIV Diagnostics

-

Market, BY End User (USD Billion)

-

\r\n\r\n\r\nHospitals

-

\r\n\r\n\r\nDiagnostic

-

Laboratories

-

\r\n\r\n\r\nHome Care Settings

-

\r\n\r\n\r\n\r\n\r\nHIV

-

Diagnostics Market, BY Product Type (USD Billion)

-

\r\n\r\n\r\nTests

-

Kits

-

\r\n\r\n\r\nInstruments

-

\r\n\r\n\r\nSoftware

-

\r\n\r\n\r\n\r\n\r\nHIV

-

Diagnostics Market, BY Technology (USD Billion)

-

\r\n\r\n\r\nElisa

-

\r\n\r\n\r\nRapid

-

Testing

-

\r\n\r\n\r\nPolymerase Chain Reaction

-

\r\n\r\n\r\n\r\n\r\nHIV

-

Diagnostics Market, BY Regional (USD Billion)

-

\r\n\r\n\r\nNorth

-

America

-

\r\n\r\n\r\nUS

-

\r\n\r\n\r\nCanada

-

\r\n\r\n\r\n\r\n\r\nEurope

-

\r\n\r\n\r\nGermany

-

\r\n\r\n\r\nUK

-

\r\n\r\n\r\nFrance

-

\r\n\r\n\r\nRussia

-

\r\n\r\n\r\nItaly

-

\r\n\r\n\r\nSpain

-

\r\n\r\n\r\nRest

-

of Europe

-

\r\n\r\n\r\n\r\n\r\nAPAC

-

\r\n\r\n\r\nChina

-

\r\n\r\n\r\nIndia

-

\r\n\r\n\r\nJapan

-

\r\n\r\n\r\nSouth

-

Korea

-

\r\n\r\n\r\nMalaysia

-

\r\n\r\n\r\nThailand

-

\r\n\r\n\r\nIndonesia

-

\r\n\r\n\r\nRest

-

of APAC

-

\r\n\r\n\r\n\r\n\r\nSouth America

-

\r\n\r\n\r\nBrazil

-

\r\n\r\n\r\nMexico

-

\r\n\r\n\r\nArgentina

-

\r\n\r\n\r\nRest

-

of South America

-

\r\n\r\n\r\n\r\n\r\nMEA

-

\r\n\r\n\r\nGCC

-

Countries

-

\r\n\r\n\r\nSouth Africa

-

\r\n\r\n\r\nRest

-

of MEA

-

\r\n\r\n\r\n\r\n\r\n\r\n\r\n\r\n\r\nCompetitive

-

Landscape

-

\r\n\r\n\r\nOverview

-

\r\n\r\n\r\nCompetitive

-

Analysis

-

\r\n\r\n\r\nMarket share Analysis

-

\r\n\r\n\r\nMajor

-

Growth Strategy in the HIV Diagnostics Market

-

\r\n\r\n\r\nCompetitive

-

Benchmarking

-

\r\n\r\n\r\nLeading Players in Terms of Number of Developments

-

in the HIV Diagnostics Market

-

\r\n\r\n\r\nKey developments and growth

-

strategies

-

\r\n\r\n\r\nNew Product Launch/Service Deployment

-

\r\n\r\n\r\nMerger

-

& Acquisitions

-

\r\n\r\n\r\nJoint Ventures

-

\r\n\r\n\r\n\r\n\r\nMajor

-

Players Financial Matrix

-

\r\n\r\n\r\nSales and Operating Income

-

\r\n\r\n\r\nMajor

-

Players R&D Expenditure. 2023

-

\r\n\r\n\r\n\r\n\r\n\r\n\r\nCompany

-

Profiles

-

\r\n\r\n\r\nAbbott Laboratories

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nThermo Fisher Scientific

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nBecton Dickinson and Company

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nHologic Inc

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nMeridian Bioscience

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nGrifols

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nGenMark Diagnostics

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nDanaher Corporation

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nRoche Holding AG

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nQuidel Corporation

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nBioRad Laboratories

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nPerkinElmer

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nCepheid

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nOrtho Clinical Diagnostics

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\nSiemens Healthineers

-

\r\n\r\n\r\nFinancial

-

Overview

-

\r\n\r\n\r\nProducts Offered

-

\r\n\r\n\r\nKey

-

Developments

-

\r\n\r\n\r\nSWOT Analysis

-

\r\n\r\n\r\nKey

-

Strategies

-

\r\n\r\n\r\n\r\n\r\n\r\n\r\nAppendix

-

\r\n\r\n\r\nReferences

-

\r\n\r\n\r\nRelated

-

Reports

-

\r\n\r\n\r\n\r\n\r\nLIST Of tables

-

\r\n\r\n\r\nLIST

-

OF ASSUMPTIONS

-

\r\n\r\n\r\nNorth America HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nNorth

-

America HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nNorth America HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nNorth

-

America HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nNorth America HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nUS

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nUS HIV Diagnostics Market SIZE ESTIMATES &

-

FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nUS HIV

-

Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nUS HIV Diagnostics Market SIZE ESTIMATES &

-

FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nUS

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nCanada HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nCanada

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nCanada HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nCanada

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nCanada HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nEurope

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nEurope HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nEurope

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nEurope HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nEurope

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nGermany HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nGermany

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nGermany HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nGermany

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nGermany HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nUK

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nUK HIV Diagnostics Market SIZE ESTIMATES &

-

FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nUK HIV

-

Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nUK HIV Diagnostics Market SIZE ESTIMATES &

-

FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nUK

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nFrance HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nFrance

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nFrance HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nFrance

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nFrance HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRussia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nRussia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRussia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRussia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRussia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nItaly HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nItaly

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nItaly HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nItaly

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nItaly HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSpain

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nSpain HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSpain

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSpain HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSpain

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nRest of Europe HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of Europe HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of Europe HIV Diagnostics Market

-

SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of Europe HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of Europe HIV Diagnostics Market

-

SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nAPAC

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nAPAC HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nAPAC

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nAPAC HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nAPAC

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nChina HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nChina

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nChina HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nChina

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nChina HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nIndia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nIndia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nIndia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nIndia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nIndia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nJapan HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nJapan

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nJapan HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nJapan

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nJapan HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

Korea HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth Korea HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

Korea HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth Korea HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

Korea HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nMalaysia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMalaysia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMalaysia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMalaysia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMalaysia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nThailand

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nThailand HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nThailand

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nThailand HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nThailand

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nIndonesia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nIndonesia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nIndonesia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nIndonesia

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nIndonesia HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of APAC HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of APAC HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of APAC HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of APAC HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of APAC HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth America HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

America HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth America HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

America HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth America HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nBrazil

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nBrazil HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nBrazil

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nBrazil HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nBrazil

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMexico HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMexico

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMexico HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMexico

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMexico HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nArgentina

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nArgentina HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nArgentina

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nArgentina HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nArgentina

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nRest of South America HIV Diagnostics Market

-

SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of South America HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER,

-

\r\n\r\n\r\nRest of South America HIV Diagnostics

-

Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of South America HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY,

-

\r\n\r\n\r\nRest of South America HIV Diagnostics

-

Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMEA

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMEA HIV Diagnostics Market SIZE ESTIMATES &

-

FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMEA HIV

-

Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nMEA HIV Diagnostics Market SIZE ESTIMATES &

-

FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nMEA

-

HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD

-

Billions)

-

\r\n\r\n\r\nGCC Countries HIV Diagnostics Market SIZE ESTIMATES

-

& FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nGCC

-

Countries HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nGCC Countries HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nGCC

-

Countries HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nGCC Countries HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

Africa HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth Africa HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY END USER, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

Africa HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nSouth Africa HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nSouth

-

Africa HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY REGIONAL, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of MEA HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY TEST TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of MEA HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY END USER, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of MEA HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY PRODUCT TYPE, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nRest

-

of MEA HIV Diagnostics Market SIZE ESTIMATES & FORECAST, BY TECHNOLOGY, 2019-2035

-

(USD Billions)

-

\r\n\r\n\r\nRest of MEA HIV Diagnostics Market SIZE

-

ESTIMATES & FORECAST, BY REGIONAL, 2019-2035 (USD Billions)

-

\r\n\r\n\r\nPRODUCT

-

LAUNCH/PRODUCT DEVELOPMENT/APPROVAL

-

\r\n\r\n\r\nACQUISITION/PARTNERSHIP

-

\r\n\r\n\r\nLIST

-

Of figures

-

\r\n\r\n\r\nMARKET SYNOPSIS

-

\r\n\r\n\r\nNORTH

-

AMERICA HIV DIAGNOSTICS MARKET ANALYSIS

-

\r\n\r\n\r\nUS HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nUS HIV DIAGNOSTICS MARKET

-

ANALYSIS BY END USER

-

\r\n\r\n\r\nUS HIV DIAGNOSTICS MARKET ANALYSIS

-

BY PRODUCT TYPE

-

\r\n\r\n\r\nUS HIV DIAGNOSTICS MARKET ANALYSIS BY

-

TECHNOLOGY

-

\r\n\r\n\r\nUS HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nCANADA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nCANADA HIV

-

DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nCANADA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nCANADA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nCANADA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nEUROPE HIV DIAGNOSTICS MARKET

-

ANALYSIS

-

\r\n\r\n\r\nGERMANY HIV DIAGNOSTICS MARKET ANALYSIS BY TEST

-

TYPE

-

\r\n\r\n\r\nGERMANY HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nGERMANY

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nGERMANY

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nGERMANY

-

HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nUK HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nUK HIV DIAGNOSTICS MARKET

-

ANALYSIS BY END USER

-

\r\n\r\n\r\nUK HIV DIAGNOSTICS MARKET ANALYSIS

-

BY PRODUCT TYPE

-

\r\n\r\n\r\nUK HIV DIAGNOSTICS MARKET ANALYSIS BY

-

TECHNOLOGY

-

\r\n\r\n\r\nUK HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nFRANCE

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nFRANCE HIV

-

DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nFRANCE HIV DIAGNOSTICS

-

MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nFRANCE HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nFRANCE HIV DIAGNOSTICS

-

MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nRUSSIA HIV DIAGNOSTICS MARKET

-

ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nRUSSIA HIV DIAGNOSTICS MARKET ANALYSIS

-

BY END USER

-

\r\n\r\n\r\nRUSSIA HIV DIAGNOSTICS MARKET ANALYSIS BY

-

PRODUCT TYPE

-

\r\n\r\n\r\nRUSSIA HIV DIAGNOSTICS MARKET ANALYSIS BY

-

TECHNOLOGY

-

\r\n\r\n\r\nRUSSIA HIV DIAGNOSTICS MARKET ANALYSIS BY

-

REGIONAL

-

\r\n\r\n\r\nITALY HIV DIAGNOSTICS MARKET ANALYSIS BY TEST

-

TYPE

-

\r\n\r\n\r\nITALY HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nITALY

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nITALY

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nITALY HIV

-

DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nSPAIN HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nSPAIN HIV DIAGNOSTICS MARKET

-

ANALYSIS BY END USER

-

\r\n\r\n\r\nSPAIN HIV DIAGNOSTICS MARKET ANALYSIS

-

BY PRODUCT TYPE

-

\r\n\r\n\r\nSPAIN HIV DIAGNOSTICS MARKET ANALYSIS

-

BY TECHNOLOGY

-

\r\n\r\n\r\nSPAIN HIV DIAGNOSTICS MARKET ANALYSIS BY

-

REGIONAL

-

\r\n\r\n\r\nREST OF EUROPE HIV DIAGNOSTICS MARKET ANALYSIS

-

BY TEST TYPE

-

\r\n\r\n\r\nREST OF EUROPE HIV DIAGNOSTICS MARKET ANALYSIS

-

BY END USER

-

\r\n\r\n\r\nREST OF EUROPE HIV DIAGNOSTICS MARKET ANALYSIS

-

BY PRODUCT TYPE

-

\r\n\r\n\r\nREST OF EUROPE HIV DIAGNOSTICS MARKET

-

ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nREST OF EUROPE HIV DIAGNOSTICS

-

MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nAPAC HIV DIAGNOSTICS MARKET

-

ANALYSIS

-

\r\n\r\n\r\nCHINA HIV DIAGNOSTICS MARKET ANALYSIS BY TEST

-

TYPE

-

\r\n\r\n\r\nCHINA HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nCHINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nCHINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nCHINA HIV

-

DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nINDIA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nINDIA HIV DIAGNOSTICS MARKET

-

ANALYSIS BY END USER

-

\r\n\r\n\r\nINDIA HIV DIAGNOSTICS MARKET ANALYSIS

-

BY PRODUCT TYPE

-

\r\n\r\n\r\nINDIA HIV DIAGNOSTICS MARKET ANALYSIS

-

BY TECHNOLOGY

-

\r\n\r\n\r\nINDIA HIV DIAGNOSTICS MARKET ANALYSIS BY

-

REGIONAL

-

\r\n\r\n\r\nJAPAN HIV DIAGNOSTICS MARKET ANALYSIS BY TEST

-

TYPE

-

\r\n\r\n\r\nJAPAN HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nJAPAN

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nJAPAN

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nJAPAN HIV

-

DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nSOUTH KOREA HIV

-

DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nSOUTH KOREA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nSOUTH KOREA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nSOUTH

-

KOREA HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nSOUTH

-

KOREA HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nMALAYSIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nMALAYSIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nMALAYSIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nMALAYSIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nMALAYSIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nTHAILAND

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nTHAILAND

-

HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nTHAILAND

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nTHAILAND

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nTHAILAND

-

HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nINDONESIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nINDONESIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nINDONESIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nINDONESIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nINDONESIA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nREST OF APAC

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nREST OF

-

APAC HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nREST

-

OF APAC HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nREST

-

OF APAC HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nREST

-

OF APAC HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nSOUTH

-

AMERICA HIV DIAGNOSTICS MARKET ANALYSIS

-

\r\n\r\n\r\nBRAZIL HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nBRAZIL HIV DIAGNOSTICS MARKET

-

ANALYSIS BY END USER

-

\r\n\r\n\r\nBRAZIL HIV DIAGNOSTICS MARKET ANALYSIS

-

BY PRODUCT TYPE

-

\r\n\r\n\r\nBRAZIL HIV DIAGNOSTICS MARKET ANALYSIS

-

BY TECHNOLOGY

-

\r\n\r\n\r\nBRAZIL HIV DIAGNOSTICS MARKET ANALYSIS

-

BY REGIONAL

-

\r\n\r\n\r\nMEXICO HIV DIAGNOSTICS MARKET ANALYSIS BY

-

TEST TYPE

-

\r\n\r\n\r\nMEXICO HIV DIAGNOSTICS MARKET ANALYSIS BY END

-

USER

-

\r\n\r\n\r\nMEXICO HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT

-

TYPE

-

\r\n\r\n\r\nMEXICO HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nMEXICO

-

HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nARGENTINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nARGENTINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nARGENTINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nARGENTINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nARGENTINA

-

HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nREST OF SOUTH

-

AMERICA HIV DIAGNOSTICS MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nREST

-

OF SOUTH AMERICA HIV DIAGNOSTICS MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nREST

-

OF SOUTH AMERICA HIV DIAGNOSTICS MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nREST

-

OF SOUTH AMERICA HIV DIAGNOSTICS MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nREST

-

OF SOUTH AMERICA HIV DIAGNOSTICS MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nMEA

-

HIV DIAGNOSTICS MARKET ANALYSIS

-

\r\n\r\n\r\nGCC COUNTRIES HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nGCC COUNTRIES HIV DIAGNOSTICS

-

MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nGCC COUNTRIES HIV DIAGNOSTICS

-

MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nGCC COUNTRIES HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nGCC COUNTRIES HIV DIAGNOSTICS

-

MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nSOUTH AFRICA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nSOUTH AFRICA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nSOUTH AFRICA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nSOUTH AFRICA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nSOUTH AFRICA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nREST OF MEA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TEST TYPE

-

\r\n\r\n\r\nREST OF MEA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY END USER

-

\r\n\r\n\r\nREST OF MEA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY PRODUCT TYPE

-

\r\n\r\n\r\nREST OF MEA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY TECHNOLOGY

-

\r\n\r\n\r\nREST OF MEA HIV DIAGNOSTICS

-

MARKET ANALYSIS BY REGIONAL

-

\r\n\r\n\r\nKEY BUYING CRITERIA OF HIV

-

DIAGNOSTICS MARKET

-

\r\n\r\n\r\nRESEARCH PROCESS OF MRFR

-

\r\n\r\n\r\nDRO

-

ANALYSIS OF HIV DIAGNOSTICS MARKET

-

\r\n\r\n\r\nDRIVERS IMPACT ANALYSIS:

-

HIV DIAGNOSTICS MARKET

-

\r\n\r\n\r\nRESTRAINTS IMPACT ANALYSIS: HIV

-

DIAGNOSTICS MARKET

-

\r\n\r\n\r\nSUPPLY / VALUE CHAIN: HIV DIAGNOSTICS

-

MARKET

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET, BY TEST TYPE, 2025 (%

-

SHARE)

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET, BY TEST TYPE, 2019 TO

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET, BY END USER,

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET, BY END USER, 2019

-

TO 2035 (USD Billions)

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET, BY PRODUCT

-

TYPE, 2025 (% SHARE)

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET, BY PRODUCT

-

TYPE, 2019 TO 2035 (USD Billions)

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET,

-

BY TECHNOLOGY, 2025 (% SHARE)

-

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET,

-

BY TECHNOLOGY, 2019 TO 2035 (USD Billions)

-

\r\n\r\n\r\nHIV DIAGNOSTICS

-

MARKET, BY REGIONAL, 2025 (% SHARE)

-

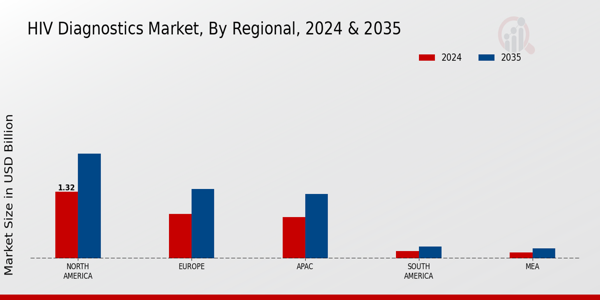

\r\n\r\n\r\nHIV DIAGNOSTICS MARKET,

-

BY REGIONAL, 2019 TO 2035 (USD Billions)

-

\r\n\r\n\r\nBENCHMARKING

-

OF MAJOR COMPETITORS

-

\r\n\r\n\r\n

Leave a Comment