自動車HVAC市場 概要

MRFRの分析によると、自動車用HVAC市場の規模は2024年に315.5億米ドルと推定されました。自動車用HVAC業界は、2025年に32.6から2035年には45.19に成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は3.32を示します。

主要な市場動向とハイライト

自動車HVAC市場は、高度な技術と持続可能なソリューションへの変革的なシフトを経験しています。

- スマート技術の統合はHVACシステムを再構築し、ユーザーエクスペリエンスと効率を向上させています。

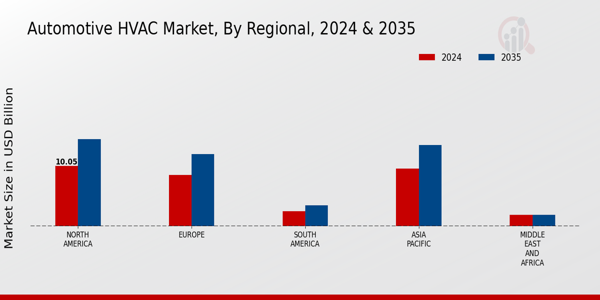

市場規模と予測

| 2024 Market Size | 315.5億ドル |

| 2035 Market Size | 45.19 (USD十億) |

| CAGR (2025 - 2035) | 3.32% |

主要なプレーヤー

デンソー株式会社(JP)、ヴァレオSA(FR)、ハノンシステムズ(KR)、マーレ株式会社(DE)、サンデンホールディングス株式会社(JP)、カルソニックカンセイ株式会社(JP)、デルファイテクノロジーズ(GB)、コンチネンタルAG(DE)、ジェンザーム社(US)