Author

Snehal Singh

シートフェイスマスク市場調査レポート 材料タイプ別(コットン、不織布、紙、バイオセルロース)、肌タイプ別(乾燥肌、脂性肌、混合肌、敏感肌)、機能別(保湿、アンチエイジング、明るさ、浄化)、流通チャネル別(オンライン小売、オフライン小売、美容サロン、薬局)、地域別(北米、ヨーロッパ、南米、アジア太平洋、中東およびアフリカ) - 2035年までの予測

MRFRの分析によると、シートフェイスマスク市場の規模は2024年に292.88億米ドルと推定されました。シートフェイスマスク業界は、2025年に319.16億米ドルから2035年には753.62億米ドルに成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は8.97を示します。

シートフェイスマスク市場は、変化する消費者の好みと革新的な製品の提供によって、ダイナミックな成長を遂げています。

| 2024 Market Size | 292.88 (米ドル十億) |

| 2035 Market Size | 753.62 (USD十億) |

| CAGR (2025 - 2035) | 8.97% |

ロレアル(フランス)、プロクター・アンド・ギャンブル(アメリカ)、エスティ・ローダー(アメリカ)、資生堂(日本)、ユニリーバ(イギリス)、アモーレパシフィック(韓国)、イニスフリー(韓国)、メディヒール(韓国)、ドクタージャルト+(韓国)

Our Impact

Enabled $4.3B Revenue Impact for Fortune 500 and Leading Multinationals

Partnering with 2000+ Global Organizations Each Year

30K+ Citations by Top-Tier Firms in the Industry

シートフェイスマスク市場は、消費者の好みと革新的な製品の提供が交差する中で、現在ダイナミックな進化を遂げています。個人が自己ケアとウェルネスをますます重視するようになる中で、シートマスクの需要が急増しており、これはパーソナライズされたスキンケアソリューションへの広範な傾向を反映しています。この市場は、さまざまな肌タイプや悩みに対応する多様な処方が特徴であり、美容製品におけるカスタマイズへの傾向が高まっていることを示唆しています。さらに、Eコマースプラットフォームの台頭により、消費者は自宅の快適さから幅広い選択肢を探求し、購入することができるようになりました。パーソナライズの強調に加えて、持続可能性はシートフェイスマスク市場における重要なテーマとして浮上しています。ブランドは、環境への影響に対する消費者の意識に応える形で、エコフレンドリーな素材や慣行を採用しています。このシフトは、グローバルな持続可能性目標に沿うだけでなく、倫理的消費を重視する層にも共鳴しています。市場が進化し続ける中で、革新が今後のトレンドを形成する上で重要な役割を果たすことが予想され、技術や処方の進歩が効果やユーザー体験の向上につながる可能性があります。全体として、シートフェイスマスク市場は、消費者の需要、持続可能性の取り組み、そして継続的な革新によって成長を続ける準備が整っているようです。

パーソナライズされたスキンケアソリューションへの傾向は、シートフェイスマスク市場で勢いを増しています。消費者は、特定の肌のニーズに合わせた製品をますます求めており、ブランドは水分補給、アンチエイジング、明るさなど、さまざまな悩みに対応する多様な処方を開発しています。

持続可能性は、シートフェイスマスク市場の多くのブランドにとって焦点となっています。企業は、効果的であるだけでなく、環境に配慮した製品を求める消費者の好みを反映し、エコフレンドリーな素材や慣行を採用しています。

Eコマースプラットフォームの拡大は、シートフェイスマスク市場に大きな影響を与えています。この傾向により、消費者はさまざまな製品に簡単にアクセスできるようになり、利便性が向上し、ブランドはより広いオーディエンスにリーチできるようになります。

シートフェイスマスク市場を推進する上で、革新的な処方と独自の成分の導入は重要です。ブランドは、健康志向の消費者にアピールする自然およびオーガニック成分を特徴とするマスクの開発にますます注力しています。アンチエイジングやブライトニングなど、特定の肌の問題をターゲットにした専門的なマスクの導入は、製品の差別化を高めます。市場分析によると、自然派スキンケア製品の需要が高まっており、消費者は品質に対してプレミアムを支払う意欲があります。この傾向は、ブランドが消費者の期待に応えるために革新を続ける限り、シートフェイスマスク市場が進化し続ける可能性があることを示しています。

シートフェイスマスク市場の成長において、流通チャネルの拡大は重要な役割を果たしています。Eコマースプラットフォームの台頭により、消費者はさまざまなブランドのシートマスクにアクセスしやすくなりました。さらに、従来の小売店でもこれらの製品がますます取り扱われており、入手可能性が向上しています。最近の統計によると、美容製品のオンライン販売が急増しており、消費者の購買行動の変化を示しています。この傾向は、ブランドが多様な流通戦略を活用してより広いオーディエンスにリーチすることで、シートフェイスマスク市場が引き続き成長する可能性があることを示唆しています。

消費者の間でスキンケアルーチンに対する意識が高まっていることは、シートフェイスマスク市場の主要な推進要因であるようです。個人が自分の肌の健康に対してより意識的になるにつれて、効果的なスキンケアソリューションの需要が高まります。報告によると、スキンケア市場は2026年までに約2000億米ドルの評価に達する見込みであり、シートマスクはその便利さと効果から人気の選択肢となっています。この傾向は、消費者が水分補給、栄養補給、さまざまな肌の悩みに対するターゲット治療を提供する製品を求める中で、シートフェイスマスク市場が大幅な成長を遂げる可能性が高いことを示唆しています。

シートフェイスマスク市場に対する自己ケアとウェルネスへの関心の高まりは、重要な推進要因です。個人がメンタルとフィジカルの健康を優先する中、スキンケアルーチンは自己ケアの一形態としてますます見なされています。ウェルネス文化の高まりは、リラクゼーションとリジュビネーションを促進する製品への需要の急増をもたらしました。市場データによると、自己ケア市場は大幅に成長する見込みであり、シートマスクは迅速かつ効果的な癒しのソリューションを求める消費者にとって好まれる選択肢となっています。このトレンドは、シートフェイスマスク市場がより広範なウェルネス運動と一致しているため、繁栄する可能性が高いことを示しています。

ソーシャルメディアが美容トレンドに与える影響は、シートフェイスマスク市場に大きな影響を与えています。InstagramやTikTokなどのプラットフォームは、消費者の好みを形成する上で重要な役割を果たしており、インフルエンサーがしばしばスキンケアルーチンの一部としてシートマスクを紹介しています。この可視性は、認知度を高めるだけでなく、フォロワーの間での試用を促進します。データによると、ソーシャルメディア上の美容関連コンテンツは数百万回の視聴を集めており、オンラインエンゲージメントと製品販売の間に強い相関関係があることを示唆しています。その結果、シートフェイスマスク市場は、このトレンドから恩恵を受ける可能性が高く、ブランドはソーシャルメディアマーケティングを活用してより広いオーディエンスにリーチしています。

シートフェイスマスク市場では、コットンが自然で通気性のある素材への消費者の好みと広範な人気により、さまざまな素材タイプの中で現在最大の市場シェアを占めています。非織布は、支配的ではないものの、スキンケア用途におけるその多様性と効果により、急速にシェアを拡大しています。紙やバイオセルロースなどの他の素材は、特定の消費者ニーズに応えるニッチな選択肢を提供していますが、コットンや非織布の規模や一般性には及びません。この市場における素材タイプの成長トレンドは、エコフレンドリーで持続可能な選択肢への消費者の傾向が変化していることを示しています。特に非織布は、このトレンドから恩恵を受けており、製造業者はその特性を向上させ、より魅力的にするための革新を進めています。さまざまな素材の利点に関する認識が進化するにつれて、バイオセルロースマスクの需要も高まっており、その効果と肌への適合性が優れていると見なされています。このダイナミックな状況は、市場の基本を変化させ、素材提供者間の競争を促進しています。

コットン(主流)対バイオセルロース(新興)

コットンは、その自然な特性、快適さ、通気性から、シートフェイスマスク市場で主導的な素材として位置づけられています。消費者は、コットンの低アレルギー性と肌に与える贅沢な感触を好みます。それに対して、バイオセルロースは、独自の質感と高い保湿能力で注目を集めている新しい素材です。バイオセルロースマスクは、天然のココナッツウォーターから作られており、生分解性があり、環境に配慮した消費者に人気があります。そのため、バイオセルロースは肌への利点が強調され、革新的で効果的なフェイシャルトリートメントを求めるスキンケア愛好者の間での採用が増加しています。これらの素材の独特な特性と消費者の認識が、市場の競争環境を形成しています。

シートフェイスマスク市場は主に肌タイプによってセグメント化されており、乾燥肌が水分補給や栄養製品の高い需要により最大の市場シェアを占めています。脂性肌も近く追随していますが、過剰な油分コントロールやニキビ解決策をターゲットにした魅力的な処方が急速に人気を集めています。近年、スキンケアにおける自然およびオーガニック成分への注目が高まったことで、脂性肌向けのソリューションのバリエーションが増加し、最も成長しているセグメントとなっています。革新的な成分の使用や特定の肌の悩みに合わせたマーケティング戦略がこの成長を促進しており、消費者は自分のスキンケアニーズに対してより目が肥えてきています。

乾燥肌:(優勢)対 脂性肌(新興)

乾燥肌セグメントは、市場での支配力が特徴であり、深い保湿と栄養を求める消費者に常にアピールしています。乾燥肌をターゲットにした製品は、ヒアルロン酸、グリセリン、植物抽出物などの保湿成分を特徴としており、効果的な水分補給を求めるユーザーに支持されています。一方、脂性肌セグメントは、オイル生産をバランスさせ、吹き出物を防ぐ軽量シートマスクに焦点を当てており、人気の選択肢として浮上しています。余分な油分を吸収し、テカリを防ぐように設計された処方により、このセグメントはスキンケアに熱心な若い消費者の注目を集めています。特定の肌タイプの重要性に対する認識が高まる中、脂性肌セグメントは市場の大きな発展が期待されています。

シートフェイスマスク市場の機能セグメントは、多様な製品が特徴であり、現在は保湿マスクが最大の市場シェアを占めています。これらのマスクは、肌に瞬時に水分と栄養を提供する能力から、消費者に人気があります。アンチエイジング、ブライトニング、浄化マスクなどの他のセグメントも重要な役割を果たしていますが、消費者の好みやブランド忠誠心にはさまざまなレベルがあります。成長トレンドに関しては、アンチエイジングシートマスクが最も成長しているセグメントとして浮上しており、スキンケアへの関心の高まりや若々しい肌への欲求がその要因です。高齢化社会、可処分所得の増加、スキンケアルーチンへの意識の高まりなどの要因が、このカテゴリーの需要を後押ししており、長期的な肌の利益を提供する製品への消費者の優先順位の変化を示しています。

水分補給(支配的)対浄化(新興)

保湿シートマスクは市場で強く位置づけられており、消費者の水分補給と肌の栄養に対する需要を反映しています。これらのマスクは、最大限の保湿のためにヒアルロン酸やアロエベラなどの成分が含まれていることが多く、即効性のあるスキンケアソリューションを求める幅広い層を惹きつけています。一方、浄化マスクはまだ新興カテゴリーですが、特に脂性肌やニキビができやすい肌を持つ消費者の間で注目を集めています。これらは、肌を深くクレンジングし、デトックスすることに焦点を当てており、しばしば炭やクレイが含まれています。ソーシャルメディア広告やインフルエンサーとの提携の増加は、浄化マスクの可視性を高め、ターゲットを絞ったスキンケア効果を求める若い消費者にとってトレンディな代替品として位置づけるのに役立っています。

シートフェイスマスク市場において、販売チャネルの分布はオンライン小売が大きなシェアを占めていることを示しています。このチャネルはeコマースプラットフォームを活用し、消費者が幅広い製品に簡単にアクセスできるようにしています。一方、物理店舗を含むオフライン小売は、消費者が直接製品を試したり選んだりするための対面でのショッピング体験を求める中で急成長しています。流通チャネルの成長トレンドは、いくつかの要因によって影響を受けています。eコマースのブームは、オンライン小売の重要な地位を強化し、オンラインショッピングに対する消費者の信頼が高まっています。一方、特に美容院や薬局におけるオフライン小売は、消費者が購入前に美容の専門家と相談できることや、個人的な対話を重視する中で注目を集めています。このトレンドの組み合わせが、シートフェイスマスク市場の流通環境におけるダイナミックな相互作用を促進しています。

オンライン小売(主流)対美容院(新興)

オンライン小売はシートフェイスマスク市場において支配的な流通チャネルとして機能しており、利便性とアクセスの良さが特徴です。自宅の快適さからショッピングを楽しむことができる幅広い選択肢を重視する多様な顧客層に対応しています。このセクターは、ターゲットを絞ったマーケティング戦略やソーシャルメディアプラットフォームでのインフルエンサーとのコラボレーションから恩恵を受けており、ブランドの可視性と消費者のエンゲージメントを高めています。一方で、美容サロンはこの市場における新たなセグメントを代表しており、パーソナライズされたサービスを通じて顧客体験を向上させています。これらの施設は、プロフェッショナルなトリートメントの一環としてシートマスクを楽しむ機会を消費者に提供しています。この個人的なアプローチと美容師からの熟練した推奨が、美容サロンをシートフェイスマスクの有力な流通チャネルとしての人気を高める要因となっています。

シートマスク市場に関する詳細な洞察を得る 無料サンプルを請求する

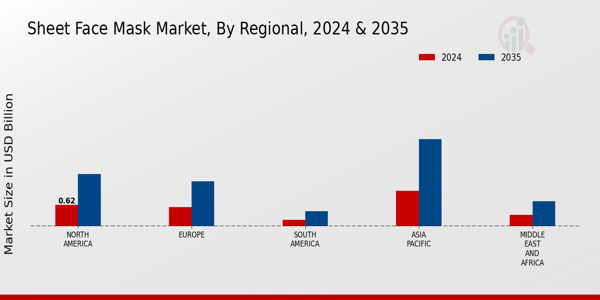

シートフェイスマスク市場は、さまざまな地域にわたる多様な景観を示しています。2024年には北米市場が5.83億米ドルと評価され、2035年までに14.08億米ドルに達する見込みであり、消費者の意識の高まりとスキンケア製品への需要の増加により、全体市場において重要なプレーヤーとなっています。

同様に、ヨーロッパは2024年に5.1億米ドルの市場を保持し、2035年までに11.92億米ドルに成長する見込みであり、消費者の間でのウェルネスとナチュラルビューティーのトレンドの高まりに支えられています。アジア太平洋地域は、2024年に10.93億米ドルと評価され、2035年には25.28億米ドルに達する予測であり、美容トレンドの急速な拡大と若年層の需要の高まりを反映しています。

一方、南米は2024年に1.46億米ドルと評価され、2035年までに3.97億米ドルに成長する見込みであり、スキンケア製品への関心の徐々の高まりを示しています。最後に、中東およびアフリカ地域は2024年に3.57億米ドルと評価され、2035年までに9.75億米ドルに達する見込みであり、美容基準の向上と化粧品の革新の恩恵を受けています。全体のシートフェイスマスク市場の収益は、可処分所得の増加、肌の健康に対する意識の高まり、オンライン小売チャネルの増加などの要因に影響され、これらの地域での有望な成長の可能性を示しています。

出典:一次調査、二次調査、マーケットリサーチフューチャーデータベース、およびアナリストレビュー

シートフェイスマスク市場は、便利さと効果を提供するスキンケア製品に対する消費者の需要の高まりによって、現在、ダイナミックな競争環境が特徴です。L'Oreal(フランス)、Procter & Gamble(米国)、Estée Lauder(米国)などの主要企業は、革新と地域拡大を通じて戦略的にポジショニングを図っています。L'Oreal(フランス)は、持続可能な成分を用いた製品ポートフォリオの強化に注力しており、これはエコフレンドリーな製品を好む消費者の嗜好の高まりと一致しています。一方、Procter & Gamble(米国)は、デジタルトランスフォーメーションを活用して顧客エンゲージメントを向上させ、サプライチェーンを効率化し、運営効率を改善しています。これらの戦略は、主要プレーヤーの影響が大きいが、新興ブランドがニッチを切り開く余地を残す、適度に断片化された市場構造に寄与しています。

ビジネス戦略に関して、企業はリードタイムを短縮し、市場の需要に対する応答性を高めるために製造のローカリゼーションを進めています。このアプローチは、サプライチェーンを最適化するだけでなく、グローバルな物流に関連するリスクを軽減します。シートフェイスマスク市場の競争構造は適度に断片化されており、いくつかの主要プレーヤーが支配する一方で、ニッチマーケティングや革新的な製品提供によって多くの小規模ブランドが登場し続けています。

2025年8月、Estée Lauder(米国)は、AI駆動のスキンケアソリューションを開発するために、主要なテクノロジー企業とのパートナーシップを発表しました。これは、パーソナライズされたスキンケアレジメンを革命的に変えることが期待されています。この戦略的な動きは、革新へのコミットメントを強調し、ますます個別化された消費者体験を重視する市場において有利なポジションを確立します。AI技術の統合は、製品の効果と顧客満足度を向上させ、売上成長を促進する可能性があります。

2025年9月、Unilever(英国)は、新しい生分解性シートマスクのラインを発表し、持続可能性へのコミットメントを反映しました。この取り組みは、環境問題に対処するだけでなく、エコ意識の高い製品を好む消費者トレンドにも合致しています。持続可能性を優先することで、Unilever(英国)はブランドロイヤルティを強化し、特に環境に配慮した消費者の間でより広い顧客基盤を引き付ける可能性があります。

2025年10月、Shiseido(日本)は、シートマスクの利点に焦点を当てた新しいマーケティングキャンペーンを発表し、若年層にリーチするためにソーシャルメディアインフルエンサーを活用しました。このデジタルマーケティングとインフルエンサーとのパートナーシップに対する戦略的な焦点は、競争の激しい市場においてブランドの可視性と消費者エンゲージメントを高める可能性があります。

2025年10月現在、シートフェイスマスク市場は、デジタル化、持続可能性、AIなどの先進技術の統合を強調するトレンドを目撃しています。主要プレーヤー間の戦略的提携が競争環境を形成し、革新を促進し、製品提供を強化しています。今後、競争の差別化は、従来の価格競争から革新、技術の進歩、サプライチェーンの信頼性に焦点を当てたものへと進化する可能性が高く、企業は現代の消費者の洗練された要求に応えようとしています。

シートフェイスマスク市場は、ここ数ヶ月で大きな変化を遂げており、大手企業が顧客のニーズの変化に対応するために計画を変更しています。ユニリーバは、特定の肌の問題を解決するために設計された新しいシートマスクのフォーミュラをスキンケアラインに追加しました。一方、ザ・フェイスショップは、ブランドの認知度を高めるためにグローバルなマーケティング活動を強化しています。資生堂は、環境に配慮した素材をパッケージに使用することに重点を置いたプロジェクトに投資しています。

プロクター・アンド・ギャンブルとトニーモリーは、健康志向の顧客にアピールするために、ターゲットを絞ったトリートメントや新しい提供方法を通じて新しいアイデアを生み出し続けています。2025年の中頃までに、トップシートマスクブランド間で公にされた大規模な合併や買収はありません。しかし、スキンケアルーチンに対する関心が高まっているため、市場は成長しています。これは、美容インフルエンサーやソーシャルメディアのトレンドに大きく影響されています。たとえば、ニュートロジーナやエスティ・ローダーは、スキンケア製品の売上が安定して成長しています。

これは、シートマスクのような専門的なトリートメントの人気が高まっていることにも起因しています。パンデミック後の時代は、2020年と2021年に自宅でのスキンケアの高まりから始まった勢いを維持しており、より大きな顧客基盤を生み出しています。市場は、eコマースが成長し続け、より多くの人々がパーソナライズされたスキンケアを求める中で、変化する顧客のニーズに応えるように変わっています。

シートフェイスマスク市場は、2024年から2035年までの間に8.97%のCAGRで成長すると予測されており、これは消費者の意識の高まりとスキンケア革新への需要の増加によって推進されています。

新しい機会は以下にあります:

2035年までに、市場はグローバルなスキンケア業界のリーダーとしての地位を確立することが期待されています。

| 市場規模 2024 | 292.88億米ドル |

| 市場規模 2025 | 319.16億米ドル |

| 市場規模 2035 | 753.62億米ドル |

| 年平均成長率 (CAGR) | 8.97% (2024 - 2035) |

| レポートの範囲 | 収益予測、競争環境、成長要因、トレンド |

| 基準年 | 2024 |

| 市場予測期間 | 2025 - 2035 |

| 過去データ | 2019 - 2024 |

| 市場予測単位 | 億米ドル |

| 主要企業のプロファイル | 市場分析進行中 |

| カバーされるセグメント | 市場セグメンテーション分析進行中 |

| 主要市場機会 | シートフェイスマスク市場における天然成分と持続可能なパッケージングの需要の高まり。 |

| 主要市場ダイナミクス | 天然成分に対する消費者の需要の高まりが、シートフェイスマスク市場における革新と競争を促進しています。 |

| カバーされる国 | 北米、ヨーロッパ、APAC、南米、中東・アフリカ |

The secondary research process involved comprehensive analysis of cosmetics regulatory frameworks, peer-reviewed dermatology journals, cosmetic science publications, and authoritative beauty industry organizations. Key sources included the US Food and Drug Administration (FDA) Center for Food Safety and Applied Nutrition (CFSAN), European Commission Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs (Cosmetics Regulation EC 1223/2009), National Medical Products Administration (NMPA) of China, Ministry of Food and Drug Safety (MFDS) of South Korea, Ministry of Health, Labour and Welfare (MHLW) of Japan, ASEAN Cosmetics Directive regulatory databases, Personal Care Products Council (PCPC), Cosmetics Europe, Korea Cosmetic Association (KCA), Japan Cosmetics Industry Association (JCIA), International Federation of Societies of Cosmetic Chemists (IFSCC), Society of Cosmetic Scientists, Journal of Cosmetic Dermatology, International Journal of Cosmetic Science, Journal of Investigative Dermatology, ITC Trade Map, UN Comtrade database, Eurostat Consumer Goods Statistics, and national cosmetics industry reports from key markets. These sources were used to collect global trade statistics, regulatory compliance data, ingredient safety assessments, consumer sentiment indices, and market landscape analysis for cotton/non-woven substrates, hydrogel masks, biocellulose masks, and functional categories including hydrating, anti-aging, brightening, and acne-control formulations.

During the initial research process, both supply-side and demand-side stakeholders were interviewed to gather both qualitative and quantitative information. Supply-side sources were CEOs, Chief Marketing Officers, Heads of Product Innovation, regulatory compliance officers, and supply chain directors from sheet face mask manufacturers, private label/OEM/ODM producers, raw material suppliers (non-woven fabric mills, biocellulose fermenters, active ingredient formulators), and packaging solution providers. Board-certified dermatologists, licensed aestheticians, beauty retail category managers (for specialty beauty, drugstore, and mass merchant channels), e-commerce platform merchandising directors, spa and wellness center procurement leads, and professional salon owners were all sources on the demand side. Primary research affirmed market segmentation based on substrate materials and functional claims, confirmed the timescales for new product pipelines, and gathered information on how consumers buy things, how to distribute products across several channels, how prices change, and how clean beauty certification works.

Primary Respondent Breakdown:

• By Designation: C-level Primaries (30%), Director Level (35%), Others (35%)

• By Region: North America (28%), Europe (25%), Asia-Pacific (35%), Rest of World (12%)

Global market valuation was derived through revenue mapping and unit volume analysis across mass, masstige, and premium segments. The methodology included:

• Identification of 40+ key manufacturers and private label suppliers across North America, Europe, Asia-Pacific, and Latin America

• Product mapping across cotton/non-woven, hydrogel, biocellulose, and bio-cellulose/second-skin substrate categories, as well as functional segments (hydration, whitening/brightening, anti-aging, soothing/sensitive skin)

• Analysis of reported and modeled annual revenues specific to sheet mask portfolios, including OEM/ODM indirect sales

• Coverage of manufacturers representing 75-80% of global market share in 2024

• Extrapolation using bottom-up (unit shipment volume × average selling price by country/channel) and top-down (manufacturer revenue cross-referenced with retail audit data) approaches to derive segment-specific valuations, adjusted for intra-regional trade flows and duty-free channel dynamics

このレポートの無料サンプルを受け取るには、以下のフォームにご記入ください

“This is really good guys. Excellent work on a tight deadline. I will continue to use you going forward and recommend you to others. Nice job”

“Thanks. It’s been a pleasure working with you, please use me as reference with any other Intel employees.”

“Thanks for sending the report it gives us a good global view of the Betaïne market.”

“Thank you, this will be very helpful for OQS.”

“We found the report very insightful! we found your research firm very helpful. I'm sending this email to secure our future business.”

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

“I have been reading the first document or the study, ,the Global HVAC and FP market report 2021 till 2026. Must say, good info! I have not gone in depth at all parts, but got a good indication of the data inside!”

“We got the report in time, we really thank you for your support in this process. I also thank to all of your team as they did a great job.”

“The Automotive 48V ECU Components Procurement Intelligence Study” was a complex project, but the Market Research Future (MRFR) team handled it with quality, agility, and customer-centricity. They delivered all requested data on time and within the agreed scope. The team, including Shubhendra Anand and Rahul Gotadki, was always readily available to clarify questions and swiftly implement necessary adjustments, driving the project to a successful conclusion within a very demanding timeframe.

I would also like to specifically commend Akshay Agarwal for his responsiveness and support at every stage—from our initial inquiry on May 6th through to final delivery on June 18th. His dedication made the entire process seamless.”