Ablation Devices Market Summary

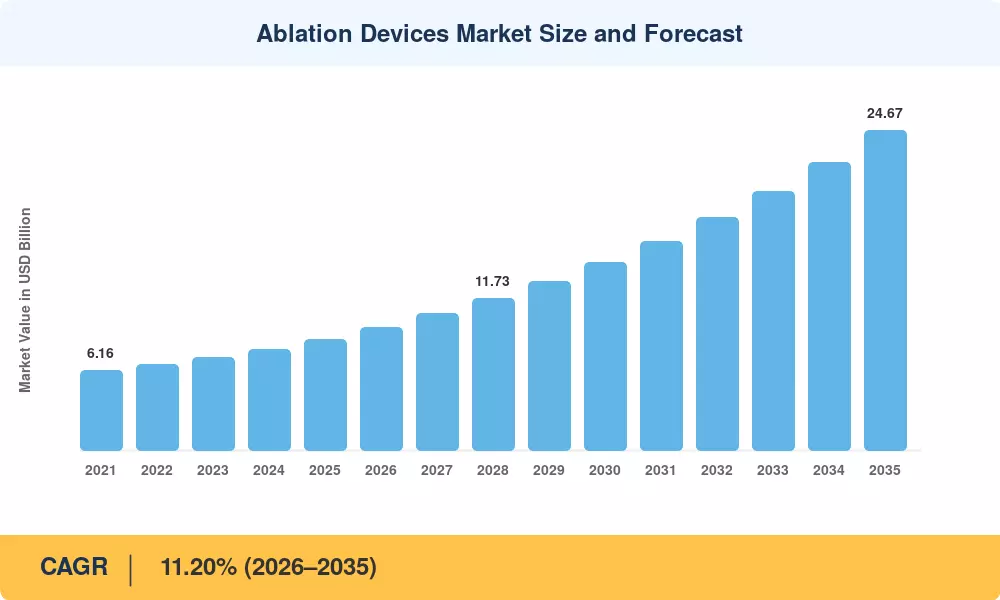

The Ablation Devices Market reached a valuation of USD 8.53 billion in 2025 and is projected to grow from USD 9.49 billion in 2026 to USD 24.67 billion by 2035, registering a CAGR of 11.20% during the forecast period (2026–2035). This growth trajectory is anchored in accelerating adoption of minimally invasive surgical procedures across oncology, cardiology, and pain management. Governments in over 40 countries have expanded reimbursement frameworks for image-guided ablation procedures since 2022, and the U.S. Centers for Medicare & Medicaid Services (CMS) added three new ablation-related billing codes in 2024, directly fueling procedural volumes [1].

A fundamental technology revolution is the foundation of the Ablation Devices Market. Traditional open-surgical techniques are being replaced by catheter-based and percutaneous energy delivery systems that lead to shorter hospital stays and faster patient recovery. In 2024, global medtech R&D expenditure in ablation-related initiatives surpassed USD 2.1 billion, with pulsed-field and hybrid-energy systems capturing the highest proportion of venture and corporate funding [2]. The FDA and EMA are examples of regulatory agencies that have established accelerated review paths for next-generation ablation platforms, reducing clearance delays by roughly 30–40% from five years ago [3].

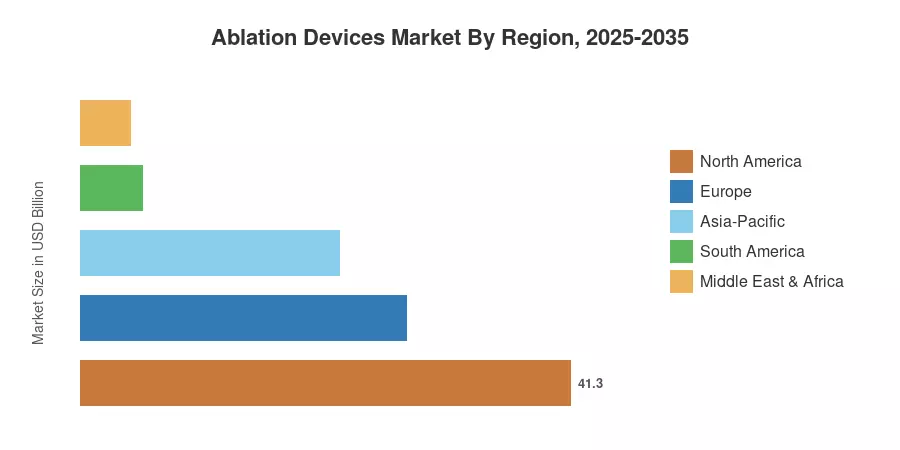

North America leads the Ablation Devices Market share, accounting for around 41.3% of the revenue in 2025. This growth is attributed to the increasing number of procedures, high prices of devices, and sophisticated payer systems. The Asia-Pacific region is the fastest-expanding region with a predicted CAGR of 13.05% through 2035 due to hospital infrastructure build-outs in China, India, and Southeast Asia. Europe has the second-highest share with approximately 27.5% of the global revenue, due to a high uptake of cardiac ablation in Germany, France, and the UK [4]. The Ablation Devices Market is expected to register continued double-digit growth until the end of the forecast window as emerging markets increase access and energy delivery technologies converge.

Key Report Takeaways

• By Device Technology

- Radiofrequency platforms accounted for 46.3% of the Ablation Devices Market in 2025, reflecting their entrenched role across both oncology and cardiac indications.

- Pulsed-field ablation is on track to become the fastest-expanding technology segment through 2035, driven by growing clinical evidence of tissue selectivity and shorter procedure times.

- Cryoablation and ultrasound-based systems continue to capture procedural share in renal denervation and tumor treatment, diversifying the technology mix of the Ablation Devices Market.

• By Application

- Oncology applications represented the largest revenue segment of the Ablation Devices Market in 2025, supported by rising hepatocellular carcinoma and lung metastasis caseloads globally.

- Cardiovascular procedures are projected to record a CAGR of 12.90% from 2026 to 2035, fueled by the global atrial fibrillation epidemic and expanding electrophysiology lab capacity.

• By Geography

- North America retained revenue leadership in the Ablation Devices Market in 2025, with the United States alone driving more than 75% of regional demand.

- Asia-Pacific is forecast to grow at 13.05% CAGR, the highest among all regions, as China and India ramp up hospital modernization programs.

- Europe held approximately 27.5% of the Ablation Devices Market in 2025, with Germany and France as the primary growth engines.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) utilizes a triangulated approach, incorporating bottom-up procedural volume modeling, top-down revenue reconciliation based on business disclosures, and confirmed secondary data from regulatory filings. All values are in USD billion at constant exchange rates. The size of the Ablation Devices Market below is based on the base year 2025, with historical estimations for the period 2021-2024 and forecast period up to 2035.