Active Geofencing Market Summary

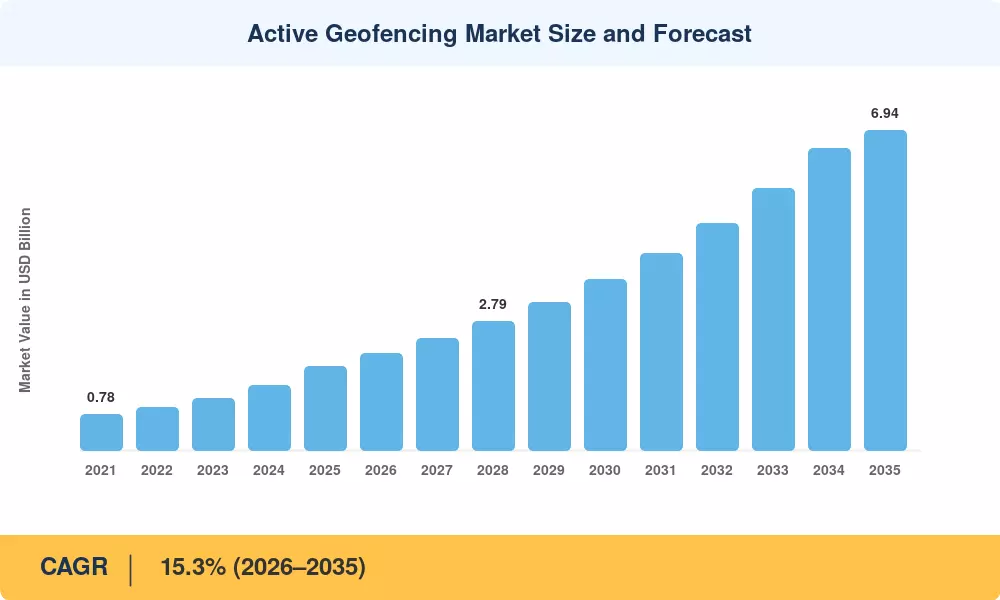

The active geofencing market is projected to reach USD 1.82 billion in 2025, growing from an estimated USD 2.10 billion in 2026 to USD 6.94 billion by 2035 at a CAGR of 15.3% during 2026–2035. This expansion is being driven by the rapid proliferation of location-aware mobile applications, tighter enterprise requirements around workforce and asset visibility, and a regulatory push — particularly in the EU and North America — toward privacy-compliant, consent-based proximity marketing frameworks. Active geofencing, which triggers real-time alerts and actions when a device enters or exits a defined virtual boundary, has moved from a niche logistics feature to a mainstream capability embedded across retail, transportation, healthcare, and smart city platforms.

The underlying technology stack is shifting meaningfully. Legacy passive geofencing solutions — which relied on periodic location polling and batch-processed boundary checks — are giving way to always-on, GPS and Wi-Fi geofence-based alerts powered by edge computing and low-power Bluetooth beacons. Investment in real-time geofencing triggers for mobile apps surged past USD 420 million globally in 2024, according to enterprise mobility spending trackers, as brands like Starbucks, Walmart, and McDonald's scaled proximity-triggered campaigns. The integration of AI-driven contextual awareness is further accelerating adoption, enabling smarter boundary logic that adapts to user behavior patterns rather than relying on static circular or polygonal fences[3].

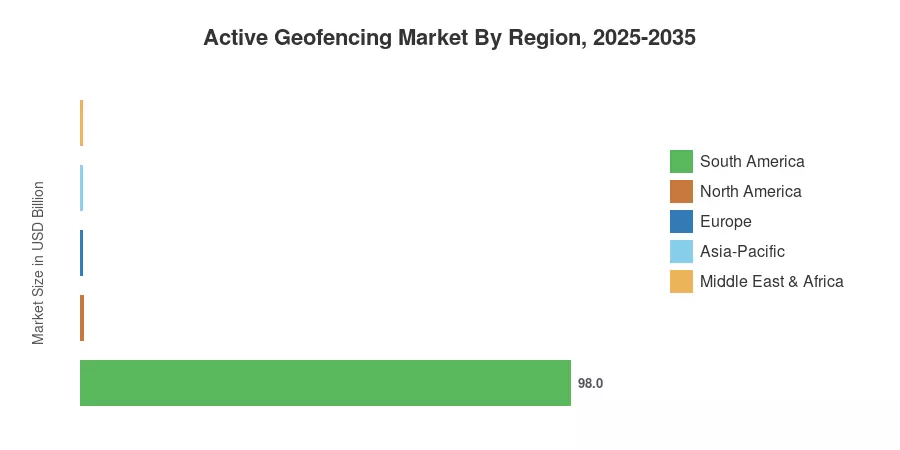

North America commands roughly 38% of the global active geofencing market, anchored by mature retail tech ecosystems and extensive fleet management deployments across the U.S. and Canada. Asia-Pacific is the fastest-growing region at an 18.1% CAGR, propelled by smartphone density in India, China, and Southeast Asia and by aggressive smart city investments. Europe holds the second-largest share at approximately 27%, where GDPR-compliant geofencing frameworks have paradoxically accelerated adoption by creating clearer rules of engagement for marketers and logistics providers The next decade will see active geofencing evolve from a standalone feature into an embedded layer of broader spatial intelligence platforms.

Key Report Takeaways

• By Technology

- GPS-based active geofencing holds a 42% market share in 2025, driven by fleet management and outdoor asset tracking use cases where satellite accuracy outperforms alternatives

- Wi-Fi and BLE-based geofencing is growing at a 17.8% CAGR, the fastest among technology segments, fueled by indoor positioning demand in retail and healthcare facilities

- Hybrid geofencing solutions (combining GPS, Wi-Fi, and cellular triangulation) are valued at approximately USD 390 million in 2025, reflecting enterprise preference for multi-signal reliability

• By Sector

- Retail and proximity marketing applications account for roughly 29% of total market revenue, as active geofencing for retail proximity marketing becomes a standard component of omnichannel strategies

- Geofencing for fleet and asset tracking is growing at a 16.2% CAGR, supported by last-mile logistics expansion and regulatory mandates for vehicle telematics in the EU and U.S.

- Workforce management — including smart geofencing for workforce attendance — represents approximately USD 285 million in 2025 market value

• By Geography

- North America leads with a 38% revenue share, underpinned by high enterprise software spending and early adoption across QSR and retail verticals

- Asia-Pacific is forecast to grow at an 18.1% CAGR through 2035, with India and China driving volumes

- Europe contributes roughly 27% of global revenue, with GDPR compliance frameworks shaping solution design across the region

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated approach combining bottom-up revenue estimation from over 120 active geofencing solution providers, top-down validation against enterprise mobility and location analytics spending benchmarks, and cross-referencing with publicly disclosed deal values and pilot program budgets from fleet operators, retailers, and smart city authorities.