Advanced Metering Infrastructure (AMI) Market Summary

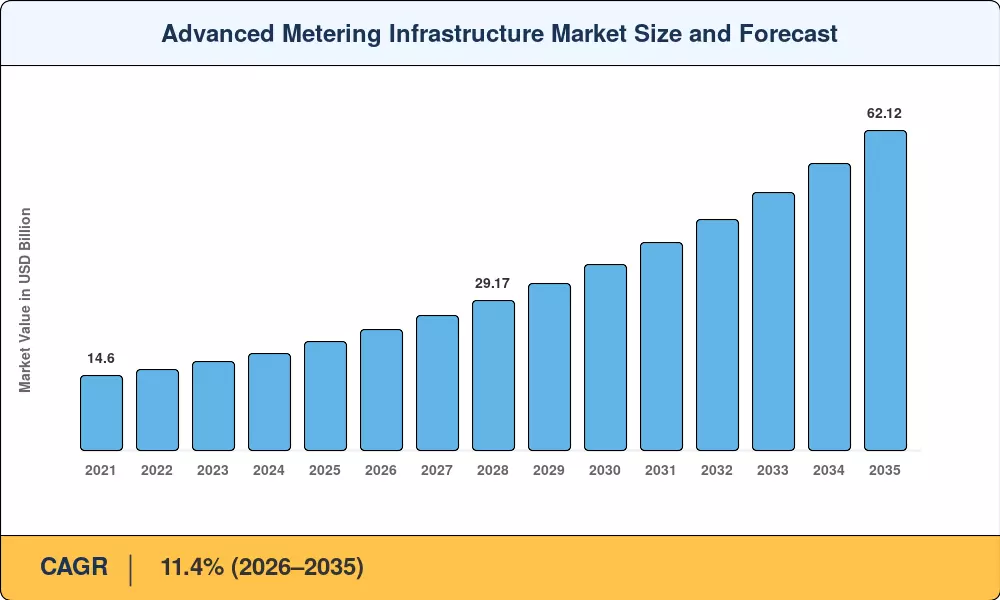

The Advanced Metering Infrastructure Market reached an estimated USD 21.10 billion in 2025 and is projected to expand from USD 23.50 billion in 2026 to USD 62.12 billion by 2035, registering a CAGR of 11.4% during the forecast period. Two catalysts stand out: the European Union's revised Energy Performance of Buildings Directive, which now requires member states to complete residential smart-meter coverage by 2030, and India's Revamped Distribution Sector Scheme (RDSS), which earmarks roughly USD 38 billion for distribution upgrade, including metering digitization [1][2]. These policy commitments guarantee multi-year procurement pipelines that underpin steady double-digit growth.

The technology shift at the core of the Advanced Metering Infrastructure Market is the replacement of electromechanical and automated meter reading (AMR) systems with two-way communicating smart meters and head-end software stacks. Utilities are moving from monthly estimated billing to fifteen-minute interval data collection, enabling dynamic pricing, outage detection within seconds, and remote connect/disconnect operations. The U.S. Department of Energy's Grid Modernization Initiative has channeled over USD 10 billion into grid-edge intelligence since 2022, a large share of which flows directly into AMI networks [3]. This funding cycle is still accelerating.

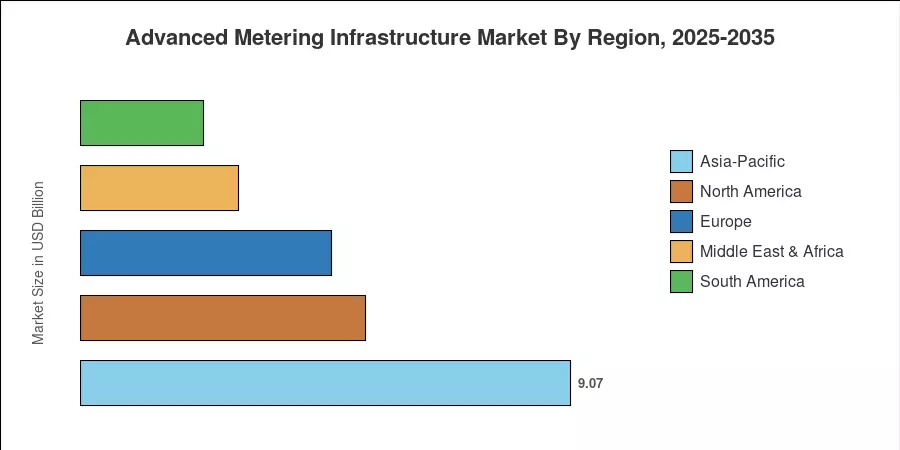

Asia-Pacific dominates the Advanced Metering Infrastructure Market with approximately 43.0% of global revenue in 2025, driven by China's State Grid rollout and India's mass procurement tenders. The Middle East & Africa region is poised to grow at the fastest clip, registering a projected CAGR of 13.9% through 2035 as Gulf states digitize utilities ahead of economic diversification targets. Europe holds the second-largest share at roughly 22%, anchored by mandated smart meter rollout programs across the EU-27. The decade ahead will reshape how the world measures, manages, and monetizes energy and water consumption.

Key Report Takeaways

• By Application

- Electricity metering accounted for an estimated 66.2% of the Advanced Metering Infrastructure Market revenue in 2025, backed by mandated national deployment schedules that assure utilities of regulated cost recovery.

- Water metering is the fastest-expanding application segment, projected to register a 14.0% CAGR through 2035, as drought-stressed regions invest in leak-detection-enabled smart meters.

- Gas metering is forecast to reach approximately USD 3.48 billion by 2035, driven by safety-regulation upgrades across European and North American distribution networks.

• By Service Model

- Professional services captured roughly 48.0% of segment revenue in 2025, reflecting utilities' ongoing reliance on system integrators for network design, deployment, and commissioning.

- Managed services are expanding at a projected 14.2% CAGR to 2035 as utilities shift toward outcome-based contracts that transfer cybersecurity and integration risk to vendors.

• By Region

- Asia-Pacific commanded 43.0% of the Advanced Metering Infrastructure Market in 2025, led by large-scale government tenders in China and India.

- The Middle East & Africa is the fastest-growing region, with a projected CAGR of 13.9%, as Gulf states modernize aging utility networks.

- North America contributed roughly USD 5.28 billion in 2025, propelled by federal grid-modernization incentives and utility rate-case approvals for AMI capital expenditure.

Market Size and Forecast (2021–2035)

Market Research Future's estimates integrate primary interviews with utility procurement officers and meter OEMs, validated against public regulatory filings, customs trade data, and vendor-reported shipments. Historical figures (2021–2024) reflect actual market activity; the base year (2025) blends trailing actuals with confirmed procurement schedules; and the forecast period (2026–2035) applies a calibrated compound growth model informed by policy timelines, technology adoption S-curves, and regional macroeconomic projections.

.webp?v=1782120131)